In Wealth, War and Wisdom (2008), Barton Biggs showed how financial markets often react with greater insight into the shifting fortunes of war than the general population. During World War II for example, German stocks peaked in 1941, well before the military disaster at Stalingrad. The US market rallied following the Battle of Midway in June 1942 even though conventional wisdom at the time downplayed its significance.

As of Friday, the Strait of Hormuz is supposedly opening back up, and crude oil sold off accordingly. The Administration will be hoping for a return to normalcy. Gasoline prices remain a looming political issue with midterms in November. But the stock market evidently sees much to like.

If Barton Biggs was alive today, he might say equity investors in their collective wisdom have concluded that the energy crisis is over.

That looks premature to us.

Past performance is not indicative of future results.

The US economy is more resilient to energy price shocks than in the past. This is because our energy intensity has been declining for decades as the service sector has increased its share of GDP. Life is also more energy efficient, from automobiles to refrigerators and light bulbs.

Since the shale revolution led to US energy independence, higher oil doesn’t simply represent a wealth transfer from consumers to OPEC. Oil producing regions of the US, notably Texas and the southwest, receive an economic boost that offsets the drag imposed by higher energy costs elsewhere.

The rise in crude is stimulating increased US exports, currently 5.2 Million Barrels per Day (MMB/D) as of the most recent weekly data (April 10) and +1.1 MMB/D on the prior week.

Both Iran and the US have shown that they can stop maritime traffic through the Strait of Hormuz. Iran’s pledge to reopen it falls short of permitting freedom of navigation. Ships will still need to check in with the Revolutionary Guard and travel close to Iran’s shore, allowing visual identification. The free flow of maritime traffic still isn’t back. Ships will only start moving again once it’s deemed safe. Iran’s asymmetric ability to impact the world economy is more potent than a nuclear bomb and far cheaper to implement. The US can’t keep a naval force in the region indefinitely. Iran will continue to create trouble.

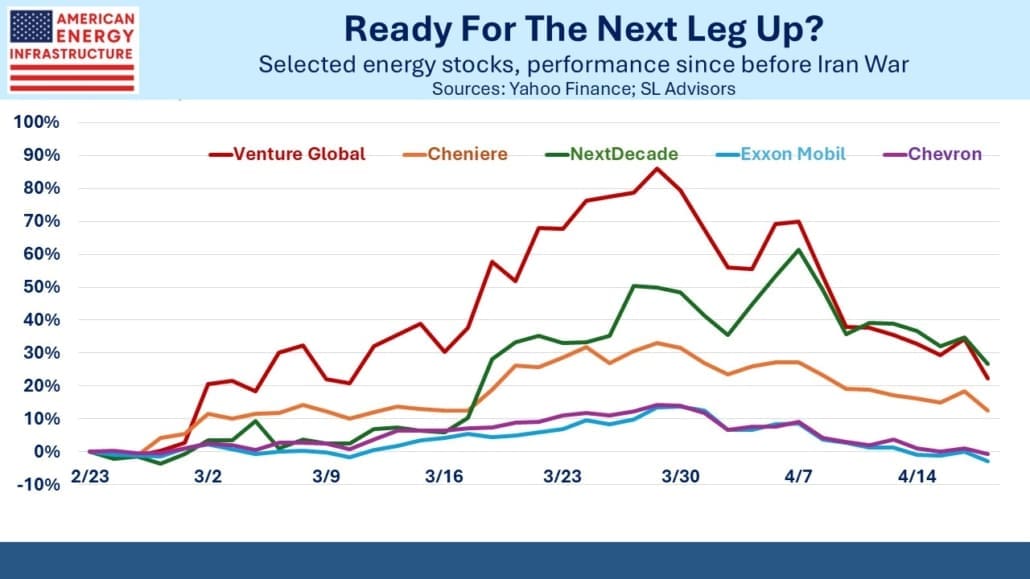

Therefore, it’s odd that energy stocks have weakened. ExxonMobil and Chevron are below their pre-war levels. The LNG exporters have also ceded gains but investors are starting to acknowledge the improvement in their long term outlook. Qatar is still not exporting any LNG and nobody knows when they will.

Iran will always retain the option to close the Strait with not much more than a few dozen drones and missiles. This is the bull case for US energy exports. The shale revolution, which began over a decade ago, brought America first energy independence, then energy security and now even energy autonomy.

Although gasoline prices are up, the US economy might be the least negatively impacted in the world. Even the Gulf states that would normally benefit are suffering from lost revenues as they shut in production. They’re also facing many $BNs in costs to repair infrastructure damaged by Iranian missiles.

Crude oil futures are becoming increasingly less representative of the actual prices paid for physical delivery. The futures markets dominate. In March, the ICE futures exchange traded over 57 million contracts on Brent crude, equivalent to over 18 times global consumption.

Buying a futures contract doesn’t get you crude today. The physical shortage has led to prices paid by refineries, especially in Asia, reportedly $10-20 or more per barrel over the front month futures contract.

Given travel times from the Persian Gulf, the last shipments that were in transit before the Strait closed have been arriving at their destinations over the past week or so. Fertilizer, sulfur, helium and aluminum all come in various significant volumes through the same bottleneck, and their absence will similarly ripple across global supply chains.

Past performance is not indicative of future results.

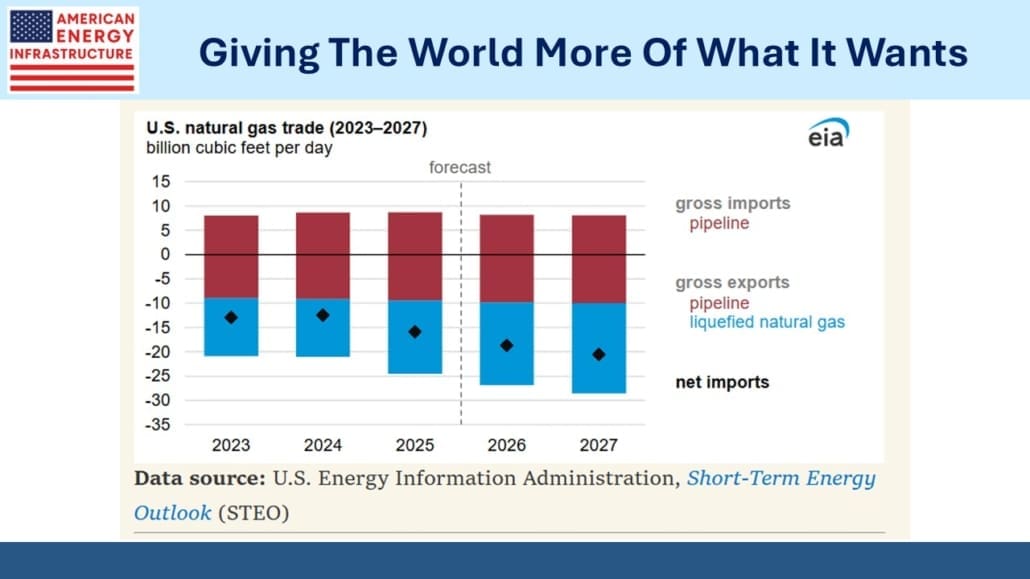

The big integrated oil companies must be worth more than before the Iran War broke out. The LNG names similarly look as if the pullback offers a good entry point. The Energy Information Administration is forecasting that LNG exports will exceed 20 Billion Cubic feet per Day (BCF/D) next year, up from 18.7 BCF/D this year.

Barton Biggs wrote a great book, but sometimes the market’s message can be misinterpreted.

The other day I found myself chatting with someone about AI. Naturally, I steered the conversation to the enormous power demands of data centers, one of the themes behind our exposure to natural gas and related infrastructure. My interlocutor was familiar with Cortical Labs, a start-up that’s using neurons to process information. I learned that they are harvested from stem cells and then genetically modified to eliminate any sensitivity to pain. Neurons require glucose and salt, not kilowatts — apparently 2 calories per neuron per day.

It’s one answer to the looming power crunch caused by data centers.

—

Originally Posted April 19, 2026 – Calmer But Not Resolved

Disclosure: SL Advisors

Please go to following link for important legal disclosures: https://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

{kind=link}

{kind=link}

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account