The “Face-to-Face Social Interactions and Local Informational Advantage” was originally published on Alpha Architect blog.

Mutual fund managers have long been thought to benefit from being close to the companies they follow. But what exactly creates that edge? Better public information, faster internal communication or something more human? This paper argues that the missing piece is face-to-face contact itself. When COVID lockdowns abruptly disrupted in-person meetings, fund managers’ advantage in local stocks weakened, suggesting that some investment edge still depends on trust, nuance, and soft information that does not travel as well through screens.

Face-to-face social interactions and local informational advantage

- Robin Y. Lee

- Journal of Financial Economics, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Face-to-face contact appears to create a real local information edge

Using COVID-19 lockdowns as an exogenous shock, the paper shows that mutual fund managers’ performance in local stocks deteriorated relative to distant stocks when in-person meetings were curtailed. The effect is not just about weaker local economies. It shows up in worse investment timing on the same stocks.

The economic effect is meaningful

After lockdowns, monthly benchmark-adjusted and DGTW-adjusted returns on local portfolios were about 0.2 to 0.4 percentage points lower than on distant portfolios, relative to the pre-lockdown period. For an average pre-lockdown local portfolio of $277 million, the paper estimates that a 0.4 percentage point monthly drop implies an annualized loss of roughly $13.3 million per fund.

The mechanism looks like soft information, not just hard data

The author compares local and distant investors trading the same stock and finds that local funds increased portfolio weight less aggressively after positive stock moves once face-to-face contact was disrupted. A one-percentage-point increase in a local position was associated with 1.3 to 1.5 percentage points lower abnormal return over the following three months, relative to distant positions, compared with the pre-lockdown period.

Trust-building is one reason in-person meetings matter

The paper argues that face-to-face meetings help build trust, which matters when information is soft, nuanced, and hard to verify. The adverse effect of losing that channel is stronger when trust distance between fund managers and corporate managers is higher. A one standard deviation increase in trust distance is associated with a 0.79 percentage point lower next-period abnormal return for local versus distant investments, per one-percentage-point increase in portfolio weight, after lockdowns.

Impression management matters too, especially on the buy side

The deterioration is concentrated in buy decisions rather than sell decisions, consistent with the idea that in-person meetings are particularly useful for transmitting favorable soft information. The effect is also stronger for firms whose CEOs have higher pay-for-performance sensitivity, suggesting that executives with stronger incentives to shape investor perceptions benefit more from the face-to-face channel.

Practical Applications for Investment Advisors

Be cautious about assuming all information travels equally well digitally

For local or relationship-driven investing, video calls and disclosures may not fully replace in-person access. If your process depends on management access, local networks, or private channel checks, treat face-to-face disruption as a real risk to information quality.

Pay more attention in less transparent names

The paper finds stronger effects in stocks with less transparent information environments, such as firms outside the S&P 500 and those with higher idiosyncratic uncertainty. That means local edge may matter more in harder-to-read businesses than in large, heavily covered names.

Separate informational edge from fundamental exposure

A useful takeaway for due diligence is to ask whether a manager’s edge comes from superior analysis of public data or from relationship-based access to soft information. Those are different skill sets, and the second one may be more vulnerable when travel, access, or social contact is disrupted.

Do not confuse lower active share with inactivity

The paper finds that managers reduced deviations from benchmark holdings after lockdowns, but they still traded actively. That suggests the problem was not a collapse in effort. It was a weaker signal environment. Advisors should distinguish between reduced conviction and reduced ability to extract information.

How to Explain This to Clients

“Being close to a company is not just about geography. It is often about access. This paper shows that when face-to-face meetings suddenly disappeared, professional investors lost some of their edge in nearby stocks. In other words, some information is still transmitted best in person, especially when trust, nuance, and judgment matter more than raw public data.”

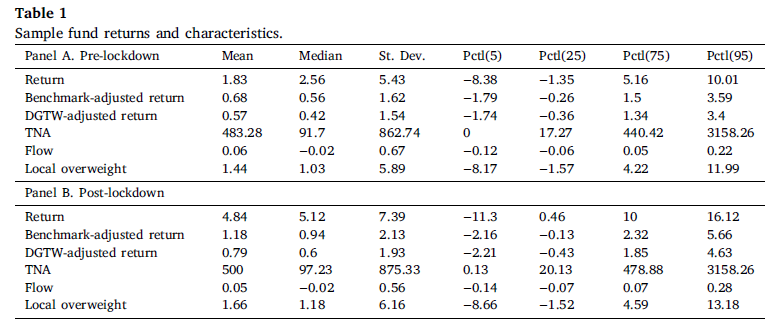

The Most Important Chart from the Paper

Table 1 summarizes the characteristics of sample funds reported separately for the pre-lockdown period (from January 2019 through the month before lockdown orders were implemented in the fund’s location) in Panel A, and for the post-lockdown period (from the implementation month through December 2020) in Panel B. Returns are calculated monthly and reported in percentage points. 𝑇𝑁𝐴 refers to the fund’s total net assets in millions. 𝐹𝑙𝑜𝑤 denotes monthly fund inflows in decimals.

𝐿𝑜𝑐𝑎𝑙 𝑜𝑣𝑒𝑟𝑤𝑒𝑖𝑔ℎ𝑡 is a measure from Coval and Moskowitz (2001) in percentage points.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This paper examines the causal role of face-to-face (F2F) interactions in generating local informational

advantages for mutual fund managers. Using COVID-19 lockdowns as an exogenous shock, I show that fund managers’ performance on local stocks declined relative to distant stocks when in-person meetings were curtailed, driven by impaired investment timing rather than changes in firm fundamentals. I investigate two distinct benefits of F2F interactions arising from interpersonal cues: trust-building, which enhances the transmission of soft information, and impression management, which facilitates the transmission of favorable information. The results cannot be fully explained by changes in internal information flows or the use of public information, and are more pronounced for stocks in less transparent information environments and in regions with stronger social traits.

Disclosure: Alpha Architect

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Mutual Funds

Not all funds are available to retail investors. Mutual Funds are investments that pool the funds of investors to purchase a range of securities to meet specified objectives, such as growth, income or both. Investors are reminded to consider the various objectives, fees, and other risks associated with investing in Mutual Funds. Please read the prospectus accordingly. This communication is not to be construed as a recommendation, solicitation or promotion of any specific fund, or family of funds. Interactive Brokers may receive compensation from fund companies in connection with purchases and holdings of mutual fund shares. Such compensation is paid out of the funds' assets. However, IBKR does not solicit you to invest in specific funds and does not recommend specific funds or any other products to you. For additional information please visit the Mutual Funds section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account