Two weeks ago, when I wrote that China’s Belt and Road Initiative (BRI) had become a Trojan Horse, I meant it figuratively. But Beijing’s latest move to tighten control over rare earth elements (REEs) makes that metaphor feel almost literal.

The 17 REEs—with obscure names like neodymium, dysprosium, samarium and terbium—act as the sinews of the modern world. They can be found in the motor of your electric vehicle (EV), the guidance systems of an F-35 fighter jet, the lenses of your iPhone and even the hospital MRI that scans your heart. Without them, the 21st-century economy simply wouldn’t run.

For decades, China has played the long game. Beginning in the 1990s, it poured capital into mining and refining rare earths while Western nations, distracted by environmental concerns and short-term cost pressures, turned the other way.

The result? China now controls roughly 70% of global mining, 92% of refining and an astonishing 98% of magnet production, according to Goldman Sachs.

Three state-run companies dominate the field. China Northern Rare Earth Group, headquartered in Baotou, Inner Mongolia, is responsible for around 70% of China’s annual production. Its peer, China Rare Earth Group, was formed in 2021 by merging several state-owned conglomerates to consolidate heavy-rare-earth output and enhance Beijing’s pricing power. Together with Xiamen Tungsten Co., which accounts for 1% of the country’s mining output, these firms make China the OPEC of strategic metals.

Economic Statecraft

Beijing has a history of restricting exports of REEs, but this month, it rolled out the most sweeping ban in its history. Starting December 1, any company seeking to export goods containing more than 0.1% of their value from Chinese-sourced rare earths must apply for a government license.

Even more consequential, any product using Chinese rare-earth technology—whether mining methods, refining equipment or magnet fabrication—will now fall under the same restrictions.

The new rules also effectively block any supply chain linked to foreign defense contractors. In other words, Beijing can now veto the flow of materials that go into America’s most advanced weapons systems.

Consider the F-35, which requires over 900 pounds of rare earths. That means America’s flagship aircraft relies, in part, on materials that Washington’s chief rival now controls.

By tightening its grip, China can squeeze strategic industries without firing a single shot. It’s the same playbook it used in 2010, when it halted rare earth exports to Japan after a maritime dispute.

MP Materials: America’s Rare Earth Miner

Goldman Sachs recently warned that a 10% disruption in REE supply could wipe out $150 billion in global output, sending shockwaves through everything from semiconductors to EVs. Samarium, terbium and lutetium were singled out as particularly vulnerable.

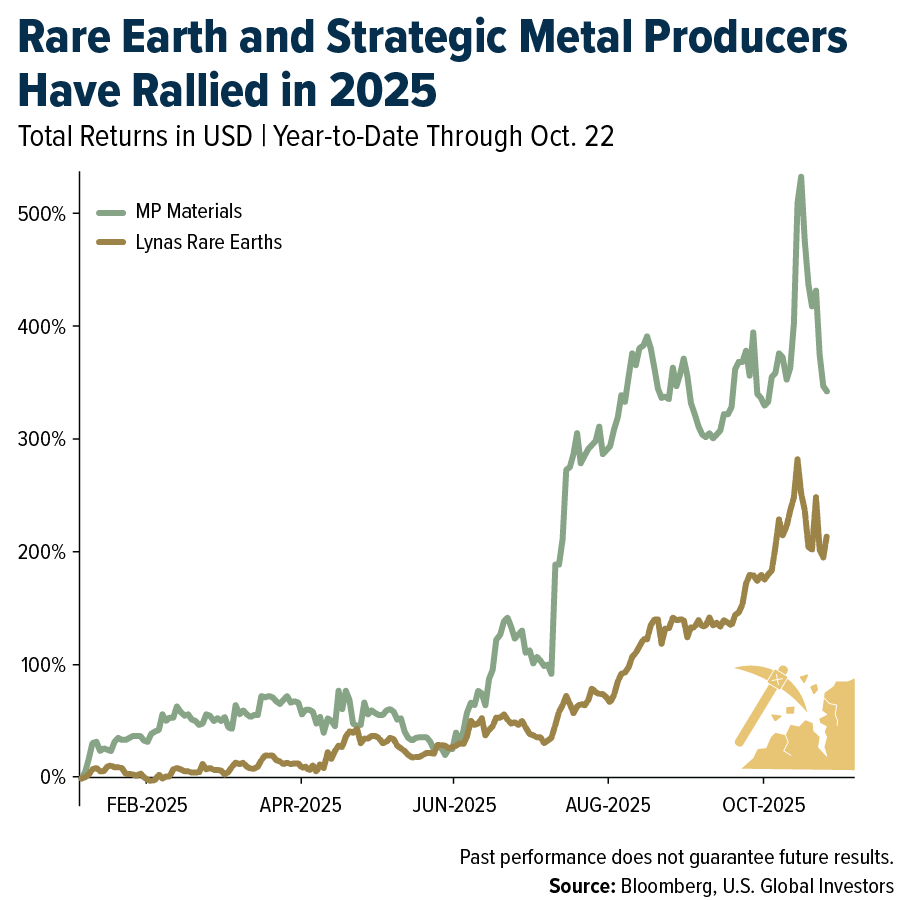

Investors have taken note. Since China’s announcement, rare earth stocks have rallied sharply in Sydney and New York, led by Lynas Rare Earths, Iluka Resources and MP Materials, the latter being America’s sole large-scale rare earth miner.

Past performance is not indicative of future results

Fortunately, Washington isn’t asleep at the wheel this time. In July, the Department of Defense (DoD)—recently renamed the Department of War—made a $400 million equity investment in MP Materials, establishing a price floor for neodymium-praseodymium (NdPr) magnets and guaranteeing offtake for defense supply chains. The DoD is now the company’s largest shareholder.

Government Policy Is a Precursor to Change

Just this month, President Trump and Australian Prime Minister Anthony Albanese signed the U.S.-Australia Critical Minerals Framework Agreement, pledging at least $1 billion in near-term financing to build processing capacity and reduce dependence on Chinese supply.

Australia is already a natural partner. Home to the Mount Weld mine, one of the world’s richest deposits, the country ranks fourth globally in rare earth production. Its producer, Lynas, achieved a milestone this May be becoming the first company outside China to produce commercial quantities of dysprosium oxide, a heavy rare earth essential for defense magnets.

What’s more, the Export-Import Bank of the U.S. is reviewing a $300 million financing package for Arafura Rare Earths’ Nolans project in Australia, while Canberra itself pledged another $100 million. The two nations plan to co-fund an $8.5 billion pipeline of critical minerals projects over the coming decade.

Lessons from Reagan

Skeptics may argue that the West can’t catch up with China, that processing capacity and environmental approvals take too long. I’d remind readers that we’ve seen this movie before.

In the early 1980s, the U.S. semiconductor industry faced intense competition from Japan, whose government-backed chipmakers were rapidly gaining market share. To counter what was viewed as unfair trade practices and dumping of underpriced semiconductors, President Ronald Reagan imposed 100% tariffs on selected Japanese chips in 1987.

In announcing the tariffs, Reagan stated that the “health and volatility of the U.S. semiconductor industry are essential to America’s future competitiveness.” He also expressed regret that the action was necessary and promised to remove the tariffs “as soon as we have firm and continuing evidence that the dumping has stopped.”

The policy, combined with the 1986 U.S.-Japan Semiconductor Agreement, helped stabilize the industry and protect domestic production. By the 1990s, Silicon Valley had regained global leadership.

I believe the same could happen with rare earths if the U.S. stays the course.

A 21st Century Gold Rush

History shows that supply disruptions can often breed attractive returns. With bipartisan support for reshoring and billions in new capital flowing into critical minerals projects, we may be witnessing the dawn on a new resource supercycle, driven by the elements that make technology itself possible.

As President Trump recently put it, this is the “gold rush of the 21st century.” The difference is that the new gold isn’t yellow but magnetic.

—

Originally Posted October 27, 2025 – The West Fights Back in the Rare Earth Wars

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the links above, you will be directed to a third-party website. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Disclosure: US Global Investors

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Alternative Investments

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account