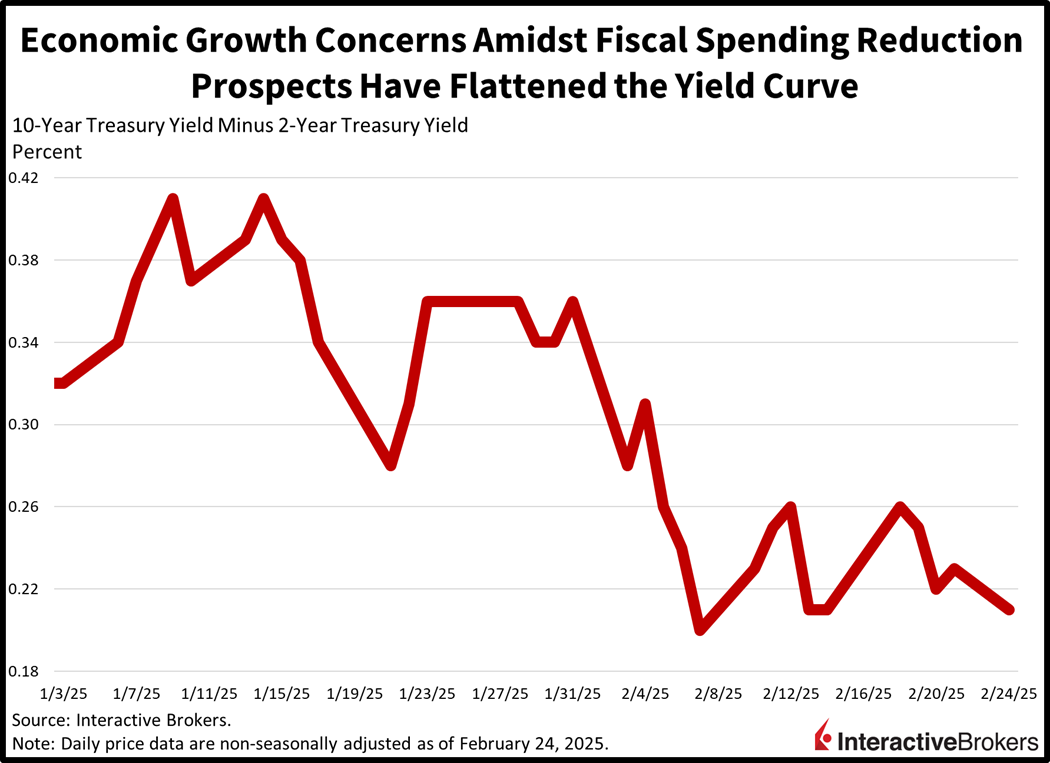

Stocks jumped right at the bell this morning, seeking to recover from last week’s losses. But the bullish momentum was short lived, as equities sank into the red roughly 20 minutes after the market open. Top of mind for market participants are incoming earnings from Home Depot, Lowe’s, Nvidia and Snowflake, which are expected to detail the capacity of the consumer, the momentum of residential investment and the strength of AI against the backdrop of Beijing’s DeepSeek challenging the cost assumptions of developing the technology. Moreover, a report from TD Cowen pointed to Microsoft cancelling data center leases, a possible sign that AI enthusiasm is beginning to fizzle. Meanwhile, investors are concerned about the potential negative effects of a smaller federal workforce on economic growth following a confusing weekend in which several department heads clashed with one another over a DOGE request for individual employees to submit five bullet points accounting for the work they did during the previous week. Emblematic of slowdown concerns is a yield curve spread that has compressed by roughly 20 bps in the past six weeks across the 2- and 10-year maturities, as rate watchers embrace bull flattener trades to brace for potential turbulence ahead.

Texas Manufacturing Slows

Today’s domestic economic calendar wasn’t very eventful, but the Dallas Federal Reserve branch reported a deterioration in Texas manufacturing activity. The Dallas Fed’s Manufacturing Index slipped to -8.3 in February from 14.1 in January. Declines in orders, production, employment, hourly workweeks and confidence drove the headline weakness. But despite the weak sentiment amidst a high degree of uncertainty regarding the outlook, capital expenditures still grew. Meanwhile, the inflationary aspects of the print were quite elevated, with charges paid, prices received and wage pressures remaining hot.

Investors Rush to Safety

Investors are selling stocks and buying Treasurys, equity volatility protection, gold bars and crude oil barrels with the proceeds. All major equity benchmarks are taking losses with the Nasdaq 100, Russell 2000, S&P 500 and Dow Jones Industrial indices lower by 1%, 0.9%, 0.5% and 0.1%. Sectoral breadth is split, however, with technology, utilities and consumer discretionary piloting the laggards; they’re down 1.3%, 0.6% and 0.6%. Countering the bearishness are healthcare, consumer staples and financials, which are gaining 1%, 0.6% and 0.3%. Treasurys are shifting in bull flattening motion once again, with the 2- and 10-year maturities changing hands at 4.19% and 4.39%, 1 and 4 basis points (bps) lighter on the session. The dollar is near its flatline though, as the greenback appreciates relative to the pound sterling, franc, yen, loonie and Aussie tender but depreciates against the euro and yuan. Commodities are mixed against this backdrop, with gains of 0.6%, 0.2% and 0.2% across crude oil, lumber and gold being partially offset by losses of 0.5% and 0.3% in silver and copper.

Can The Economy Accelerate with Smaller Deficits?

The yield curve has flattened considerably year to date, as market participants fear that a sizeable reduction in the federal workforce could negatively impact economic growth. The austerity measures could also weigh on the associated entities that perform contract work for the federal government, as well as the local economies where many public servants live and shop. Meanwhile, investors are worried that economic activity has become far too dependent on large deficits to progress, and that also has them reaching for the long-end of the curve, serving to produce bull flattener moves in the past few weeks. Finally, Treasury Secretary Bessent has committed to keeping auction sizes steady as well as the duration profile of the offerings while also supporting fiscal discipline. The stance has weighed on economic growth expectations and term premiums, sending long-term rates south faster than shorter-term ones.

Past performance is not indicative of future results

Germany’s Ruling Party Loses Control

German voters’ dissatisfaction with both the economy and immigration led to the center-right party, the Christian Democratic Union (CDU), retuning to power with an estimated 28.6% of votes while the hard-right Alternative for Germany (AfD) group trailed in second place with 20.8%. In a sign of voters’ discontent, exit polling points to the party of current Chancellor Olaf Scholoz, the Social Democratic Party of Germany (SPD), having captured only 16.4% of tallies, the weakest result since WWII. The results set up a potentially rocky political future while in a related matter, the country is bracing for a major shift with its US relationship.

The CDU and its leader, Friedrich Merz’s, are likely to face significant challenges with forming a government coalition as other political parties have said they won’t work with the AfD. Merz has also rejected forming a collation with the far-right party and is most likely to seek a partnership with the SPD, but the two organizations have substantial differences regarding government borrowing and welfare spending. In another development, Merz said President Donald Trump’s realignment of international policies requires that Europe “achieve independence” from the US.

Singapore Inflation Drops Below Expectations

Singapore’s inflation moderated last month, providing validation of the country’s central bank easing its monetary policy for the first time in almost five years last month. January’s headline and core Consumer Price Index (CPI) posted 1.2% and 0.8% y/y increases, much better than the median forecasts for 2.2% and 1.5%. Additionally, the rates eased from December’s 1.5% and 1.7%. On a m/m basis, the headline CPI fell 0.7% compared to the 0.3% gain in the preceding month. In January, the country’s central bank, the Monetary Authority of Singapore, eased its stance by modestly decreasing the slope of its policy band. The institution uses the nation’s exchange rate as the predominant factor in managing policy.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account