Stocks are cautiously recovering from yesterday’s modest losses even as investor sentiment appears circumspect ahead of the last Fed decision of the year tomorrow. But stronger-than-expected economic data are lifting yields across the curve in bear-flattening fashion, led by the monetary policy sensitive shorter tenors in response to ADP-employment, NFIB-small business optimism and JOLTS reporting improvements in hiring, consumer spending and labor demand. Also raising rates today is evidence of several central banks considering the end of their easing cycles, with Australia and the EU potentially joining Japan in the sense that their next move is likely north, not south. The developments are sobering to fixed-income watchers that have approximately two FOMC cuts penciled in during 2026.

Russell 2000 Hits Record

The Russell 2000 is leading among domestic equity benchmarks and has hit a record because it stands to benefit disproportionately from looser financial conditions. Elsewhere, cyclical commodities are mostly retreating minus lumber, while gold, silver catch bids. The greenback and volatility protection instruments are near their respective flatlines, however.

Payroll Decline Reverses

Private sector payrolls expanded by a weekly average of 4,750 jobs during the 28 days ending on Nov. 22, a significant improvement from the 13,500 positions lost in the four weeks ended on Nov. 8, according to ADP. This new indicator is published every Tuesday on weeks that don’t include the more comprehensive monthly report, which is delivered near the beginning of each month, prior to the government’s print.

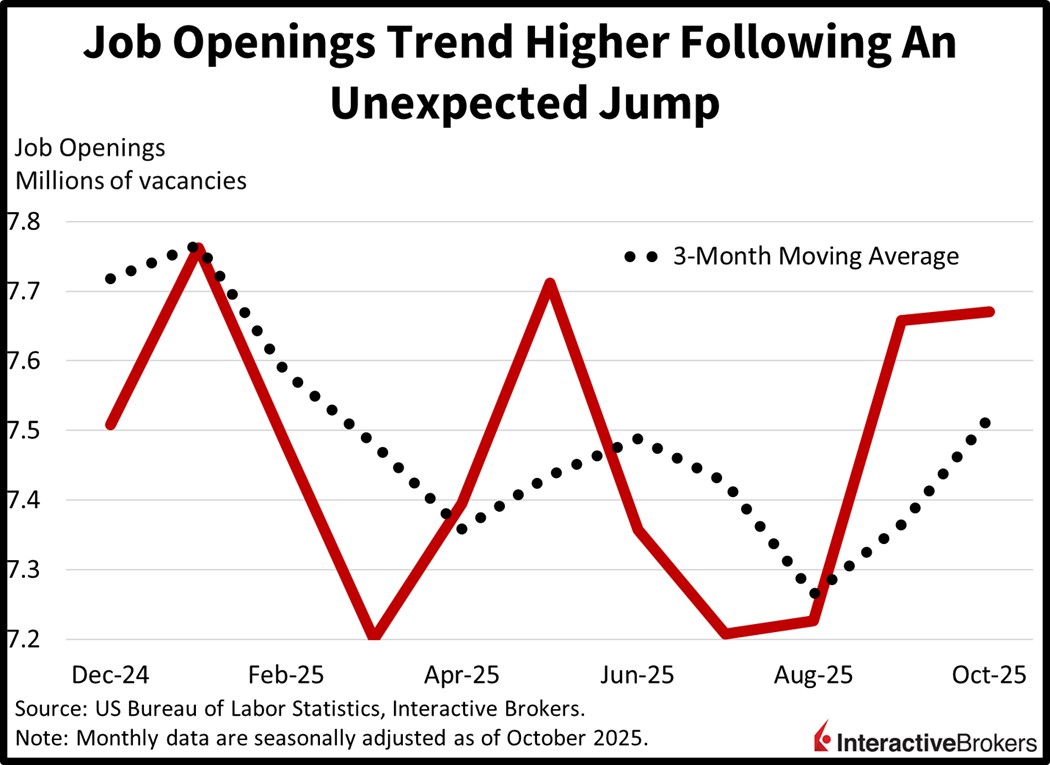

Strengthening Demand for Workers

Demand for new employees heated up in September and October with vacancies for each month totaling 7.658 million in 7.670 million, respectively. This morning’s Job Openings and Labor Turnover Survey (JOLTS) report included both periods due to the government shutdown blocking the release of public sector statistics. The numbers exceeded the 7.2 million consensus estimate by a wide margin as well as August’s 7.227 million. Retail, health care, transportation and manufacturing experienced the sharpest increases, while professional/business services, finance, accommodation/food services and information weathered the steepest declines.

Past performance does not guarantee future results.

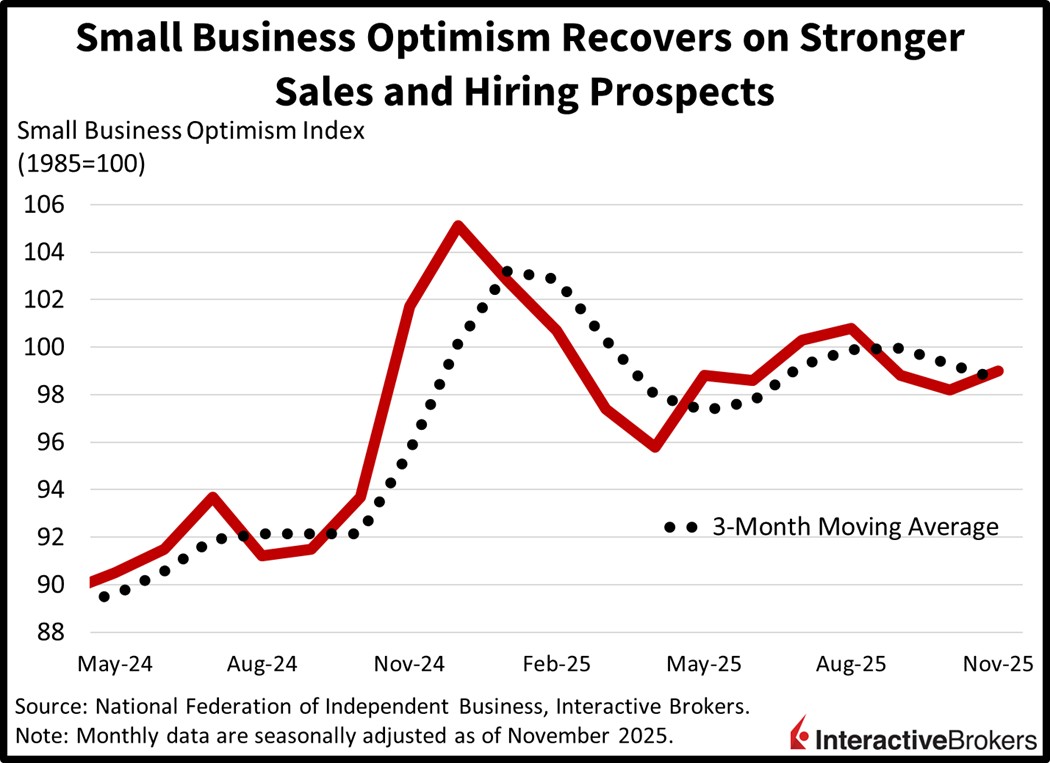

Small Business Sentiment Strengthened Last Month

Small business optimism improved in November for the first time since August as stronger revenue prospects and loftier hiring expectations lifted the National Federation of Independent Business’s (NFIB) print. Last month’s 99 result exceeded the 98.4 median estimate and October’s 98.3. Profit trends and plans to grow inventories also supported the higher number. On the other hand, capital expenditure intentions, pessimistic economic growth forecasts and tighter projected credit conditions hampered sentiment. The single most-important problem for 21% of enterprises was the quality of labor, while 15% and 14% mentioned inflation and taxes as their top issue.

Past performance does not guarantee future results.

Focusing on Dissent Among FOMC Members

The number one factor in tomorrow’s monetary policy decision will be how many cuts the committee envisions in 2026, as Wall Street is counting on additional easing to pave the path for further upside as we flip the calendar. But a critical consideration is that the central bank’s character is likely to turn dovish in May following the end of the Chair’s term. Because of the mid-year change, the future expectations of Jerome Powell may not matter as much to market participants, since he’s poised to remain at the helm for just three more meetings: January, March and April. Against that backdrop, however, investors will be focused on the degree of dissent depicted in the released materials. Our prediction platform projects that two to four voting members will formally disagree on tomorrow’s verdict, and a higher quantity would portend persistent objections in the new year, especially in light of President Trump favoring lower costs of capital.

International Roundup

Australia Central Bank Points to End of Easing

The Reserve Bank of Australia (RBA) decided yesterday to maintain its current 3.6% key interest rate and warned that it could hike if inflation persists. Central bank Governor Michele Bullock, during a press conference, told reporters she doesn’t foresee “interest rate cuts on the horizon for the foreseeable future.” She added that it’s unclear if conditions will cause the bank to tighten its policy soon or maintain an extended pause at the current 3.6% level. The last Consumer Price Index report, released in late November, showed inflation at 3.8% year over year (y/y). Government bond yields and the value of the Australian dollar both climbed after the rate decision.

While Residential Building Permits Decline

October approvals for residential construction sank 6.4% y/y and 1.8% month over month in Australia, matching economist consensus estimates and deteriorating further from September’s 1.20% y/y drop and 12% m/m jump.

And Business Sentiment and Conditions Weaken

Confidence among Australian businesses slipped 5 points to 1 in November while a survey found that conditions for entrepreneurs sank three points despite an uptick in hiring, according to the National Australia Bank. On a positive note, the survey showed that capacity utilization has climbed to 86%, the highest print in 18 months. Conversely, sales and profitability both weakened.

UK Black Friday Fails to Impress

Barclays just reported that UK credit card spending last month descended 1.1% y/y despite inflation in the country hitting 3.8%. The non-essential category fell 0.3%, the first drop in 15 months while the essential category contracted 2.9%. The British Retail Consortium and KPMG, meanwhile, reported that the total value of transactions in November ascended 1.4% y/y. In-store activity was weak, with non-food sales dropping 0.3% despite Black Friday sales. Online retailers bucked the trend with the value of transactions climbing 0.5%.

Japan Machine Orders Continue to Grow

Orders for machines tools in Japan jumped 14.2% y/y in November based on preliminary estimates from the Japan Machine Builders’ Association. The pace eased slightly from October’s 16.8% result.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account