Artificial intelligence enthusiasm has sent stocks to fresh all-time highs despite fading optimism for a plethora of Fed cuts in the near future. Tesla is leading today amidst tech-driven market gains, while certain rate-sensitive, cyclically oriented areas are descending. Illustrating the bifurcated action are the S&P 500 and Nasdaq 100 benchmarks in the green and countering the losses of the small-cap Russell 2000 and Dow Jones Industrial gauges. Meanwhile, this morning’s weaker-than-expected UMich consumer sentiment print included the second-consecutive monthly climb in long-term inflation expectations. The increase in five-year price level projections together with yesterday’s CPI reflecting broad cost pressures is extending the bear-steepening ascending movement across the Treasury curve that began before the bell, led by yields of the longer tenors. But the shorter maturities are feeling the impact of declining odds for a 50-basis point reduction from the US central bank next week, with the chances now down to the single digits. News supporting incrementally heavier domestic borrowing charges is driving an advancement for the greenback while commodity complex ex copper is catching strong bids.

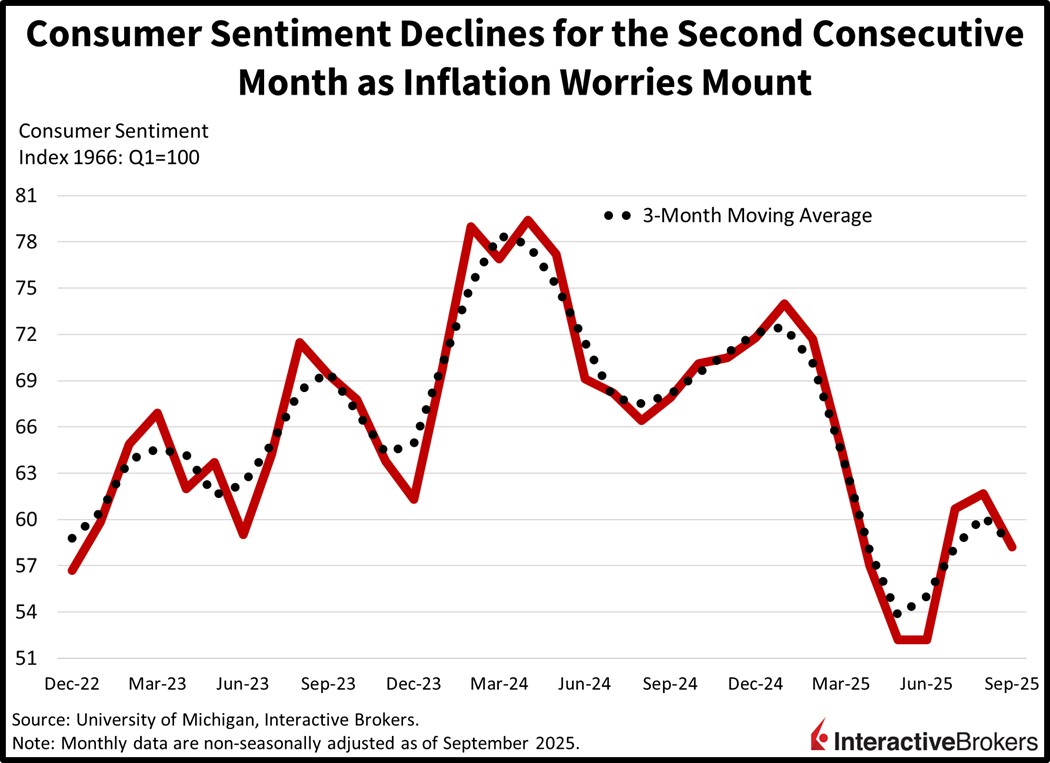

Consumer Moods Sour as Inflation Bites

Consumer sentiment declined this month, according to the University of Michigan (UMich), as the lower- and middle-income cohorts reported worse views on the economy and were particularly pessimistic about the road ahead. The headline figure of 55.4 missed the median estimate of 58 and descended from the 58.2 number from August. Both the indices for current economic conditions and the future dropped from 61.7 and 55.9 to 61.2 and 51.8. One-year inflation expectations remained unchanged at 4.8%, but the five-year projection rose for the second consecutive month to 3.9%, compared to the prior reading of 3.5%. Respondents reflected downbeat buying momentum in all components excluding durables. Households were additionally worried about business opportunities, labor market health and tariffs.

Past performance is not indicative of future results.

Inflation Angst Sparks Treasury U-Turn

The recent Treasury rally has reversed as fixed-income watchers reexamine yesterday’s CPI while receiving fresh data signaling consumer inflation angst. August’s update on price pressures wasn’t pretty, even though the highest level of initial unemployment claims in 47 months blunted its impact on financial markets. Costs rose in broad fashion across categories, including goods components that are tariff sensitive, namely cars and clothes. Meanwhile, the consumer discretionary-oriented sections, like hotels, airfares and restaurants, ascended due to servicer pricing power and sticky wage bills, which is consistent with a reaccelerating economy powered by rebounding shoppers. For stock bulls, however, this strong growth is great for corporate earnings and equity valuations, although it’s not conducive to cratering yields despite the love risk-on investors have for rate cuts.

International Roundup

UK Economy Stalled in July

The economy for the fiscally troubled UK produced no growth in July as factory activity contracted significantly, according to the Office for National Statistics (ONS). The result matched the economist consensus expectation but was down considerably from the 0.4% month-over-month (m/m) June print. While services and construction activity grew 0.1% and 0.2% respectively in July, industrial production sank 0.9%, much worse than the economist consensus expectation for a goose egg and down from 0.7% in June. All six services components increased with the 2.5% gain for warehousing leading the growth. The construction sector, furthermore, outpaced the economist consensus expectation for a 0.2% decline but it decelerated slightly from 0.3% in June. Conversely, a 5.6% decrease in motion picture, video and TV program and sound recording output caused activity in the information and communication subsector to sink 0.7%.

The news of a stagnating economy comes as Chancellor Rachel Reeves prepares to introduce the UK’s next budget on November 26. The UK faces a considerable funding shortfall unless it increases taxes or cuts spending. Either one is likely to be difficult as past measures to trim outlays for social programs were rejected by parliament. The Labor Party, furthermore, has pledged to not increase income tax, National Insurance premiums or the VAT for working people.

While Trade Deficit Widens Marginally

The UK’s goods trade deficit of $22.24 billion in July grew marginally from the $22.1 billion shortfall in June but it was much worse than the economist consensus estimate of $21.6 billion. Imports of goods from the US fell due to a drop in demand for aircraft, which pulled down results for the machinery and transport equipment category. Meanwhile, goods exports to the US grew, a result of higher demand for materials, chemicals, machinery and transport equipment. The ONS maintains that monthly trade volume can be volatile so the results should be interpreted with caution.

Canada Building Permits Falter

July issuance of building permits in Canada sank 0.1% m/m after sinking 9.5% in June. The recent result was far worse than the economist consensus expectation for growth of 3.7%. The value of permits in the residential sector increased by $268.3 million, helping to partially offset industrial and institutional declines of $252.9 million and $196 million. Among non-residential categories, the commercial component increased by $169.7 million.

And Capacity Utilization Drops

Canada’s industrial capacity utilization during the second quarter fell from 79.9% in the first three months of the year to 79.3% but was better than the economist consensus estimate of 78.8%. The mining, quarrying, and oil and gas extraction sector decreased by 1.0 percentage point to 75.9%, largely due to wildfires. Meanwhile, manufacturing sank 0.7 percentage points to 76.7%. Within this sector, the petroleum and coal category and the food manufacturing component dropped 5.2 and 2.6 percentage points.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account