Originally Posted, 15 October 2024 – Can China’s Stimulus Boost Commodities Like in 2009?

In mid-October, China fleshed out the details of its plan to stimulate growth in the world’s second largest economy:

- 2.3 trillion yuan of support for local governments, equivalent to 1.8% of GDP.

- 1.0 trillion yuan of new borrowing authorization for local governments to consolidate property developers’ debts into local balance sheets, equivalent to 0.8% of GDP.

- 1.0 trillion yuan recapitalization of the nation’s largest banks, equivalent to 0.8% of GDP.

- Lifting of restrictions on buying investment properties across most Chinese cities, and easing of requirements for first-time purchasers.

These measures come on top of the People’s Bank of China’s (PBOC) recent reduction in interest rates. If China succeeds in boosting growth, it could have profound consequences for commodity markets including crude oil, aluminum, copper, corn, soybeans and wheat. Over the past 20 years, many of these commodities have followed the path of Chinese growth, often with a lag of about one year.

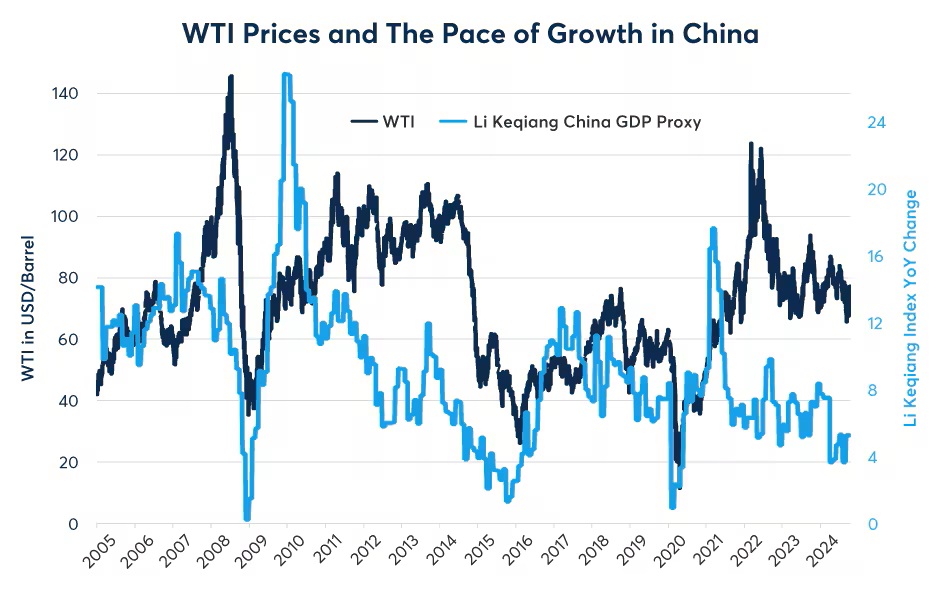

For example, using the Li Keqiang Index – which tracks bank loans, electricity consumption and rail freight volume — as a proxy for the Chinese economy, growth rates peaked in 2007, 2010, 2017 and 2021. WTI crude prices peaked just about one year later in each case (2008, 2011, 2018 and 2022) (Figure 1). The Li Keqiang Index has a strong correlation to the state of China’s industrial economy and to prices of many natural resources.

Figure 1: WTI tends to track growth in China but with a lag of 12 months

Source: Bloomberg Professional (USCRWTIC and CLKQINDX) – Past performance is not indicative of future results.

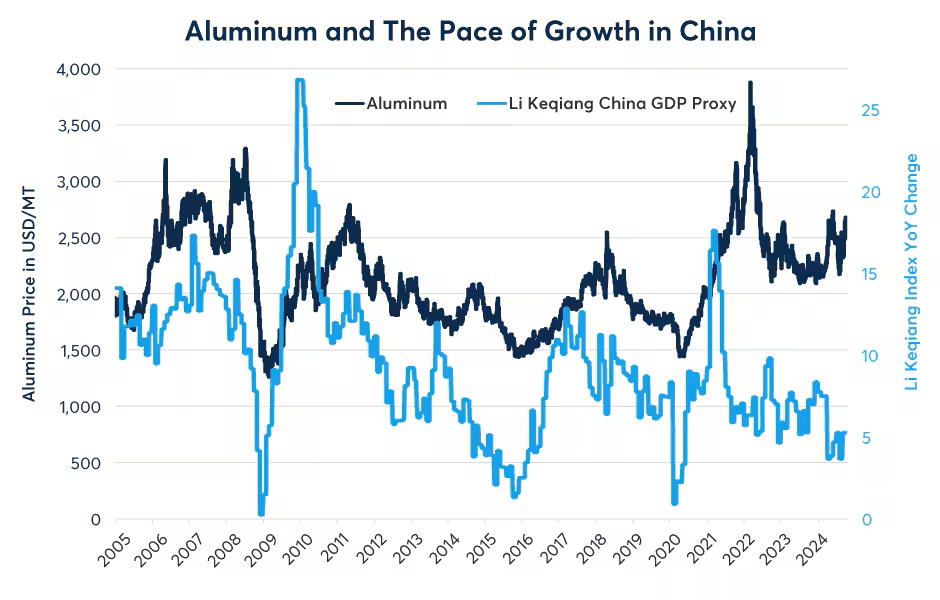

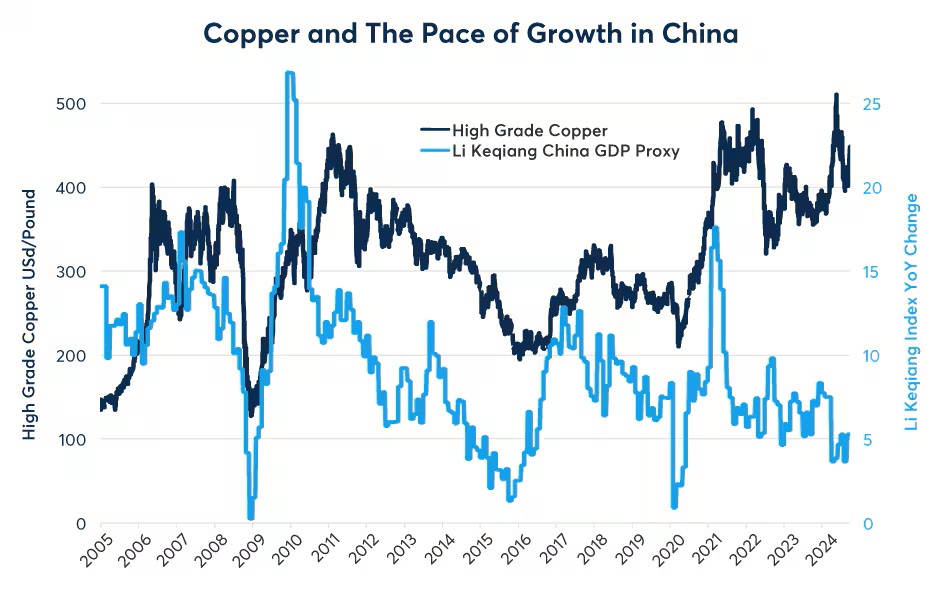

It’s a similar story for aluminum and for copper, although these two industrial metals sometimes respond to changes in the pace of Chinese growth more quickly than crude oil (Figures 2 and 3). Thus far in the 2020s, copper prices have diverged somewhat from the pace of growth in China owing to strong demand for the red metal stemming from the energy transition, and limited supply growth. By contrast, the price of aluminum appears to adhere closely to what’s been happening in China.

Figures 2 and 3: Aluminum, copper prices also tend to follow changes in the pace of China’s growth

Source: Bloomberg Professional (ALE1 and pre 2021 LA1 and CLKQINDX) – Past performance is not indicative of future results.

Source: Bloomberg Professional (HG1 and CLKQINDX) – Past performance is not indicative of future results.

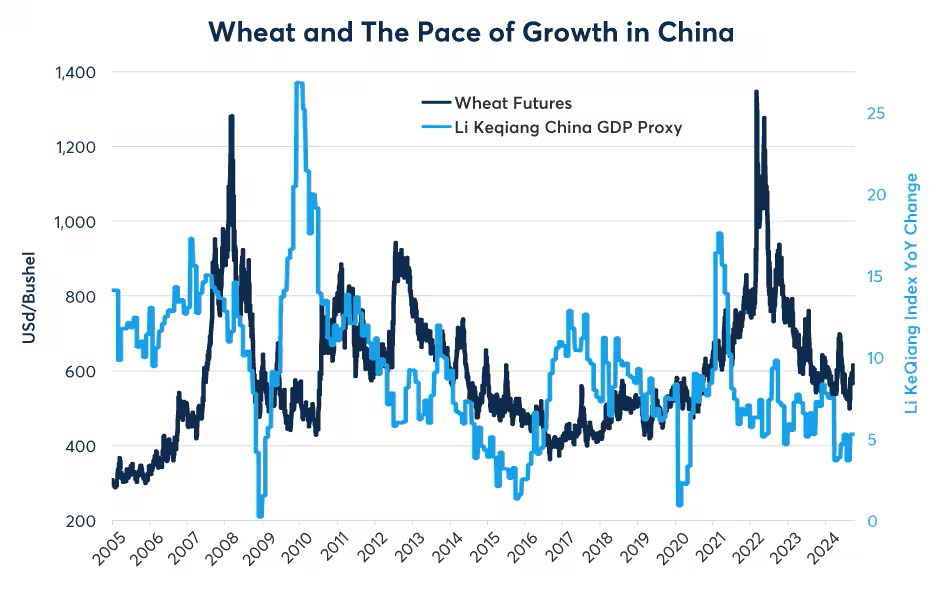

It’s a similar story for the agricultural markets. Corn and wheat, for example, also tend to follow what’s happening in China but with slightly longer lags of 12-18 months (Figures 4 and 5).

Figures 4 and 5: Corn and wheat prices have followed Chinese growth with a lag of slightly over 1 year

Source: Bloomberg Professional (C1 and CLKQINDX) – Past performance is not indicative of future results.

Source: Bloomberg Professional (W1 and CLKQINDX) – Past performance is not indicative of future results.

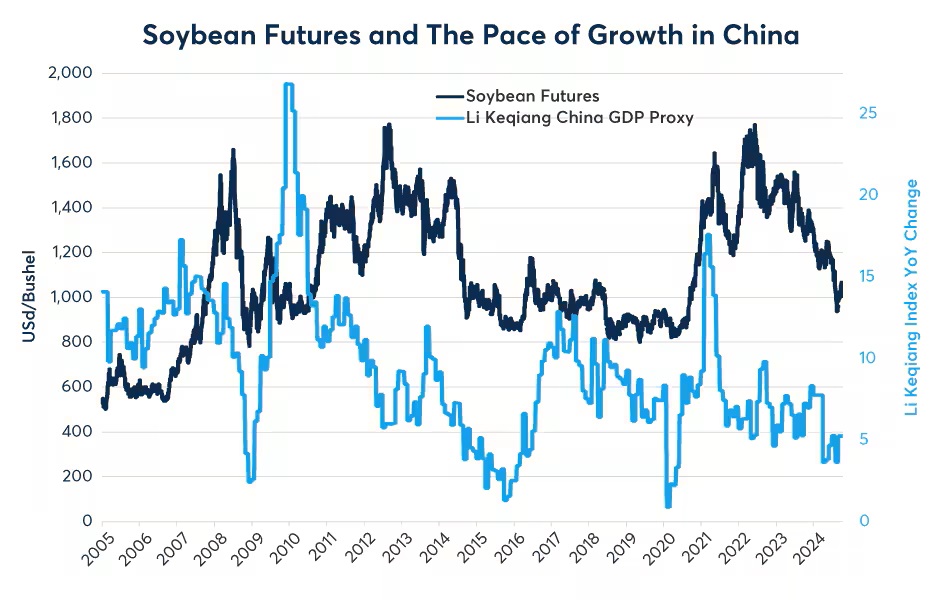

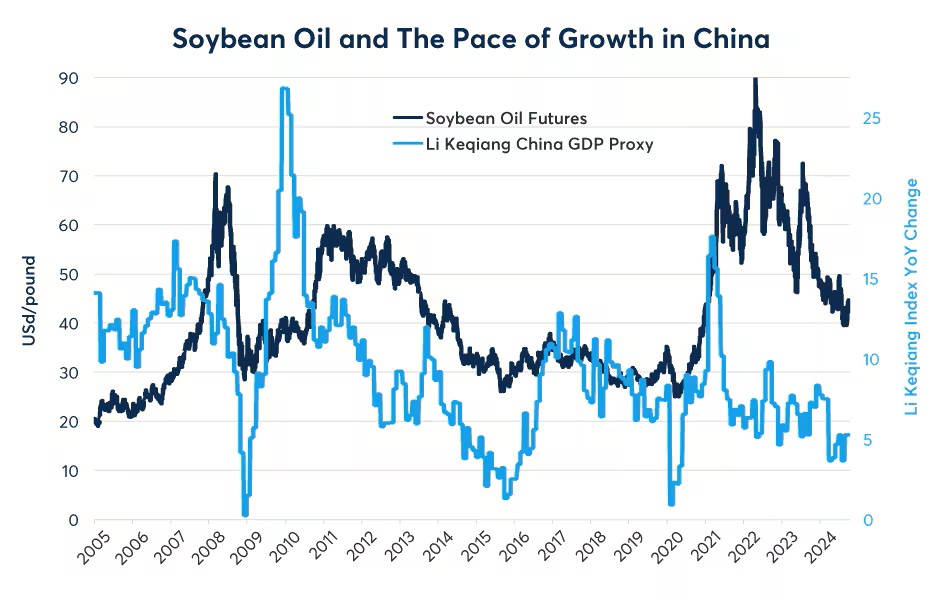

The same can be said of soybeans and soybean oil (Figures 6 and 7):

Figures 6 and 7: Soybean & soybean oil futures often follow the pace of growth in China

Source: Bloomberg Professional (S1 and CLKQINDX) – Past performance is not indicative of future results.

Source: Bloomberg Professional (BO1 and CLKQINDX) – Past performance is not indicative of future results.

Most famously, China’s 2009 stimulus generated a powerful bull market that peaked in late 2011 for oil and industrial metals, and in 2012 for the agricultural products. Oil prices rose from below $40 per barrel to above $110. Copper prices rose from $1.30 per lb to over $4.60. The prices of most agricultural goods roughly doubled.

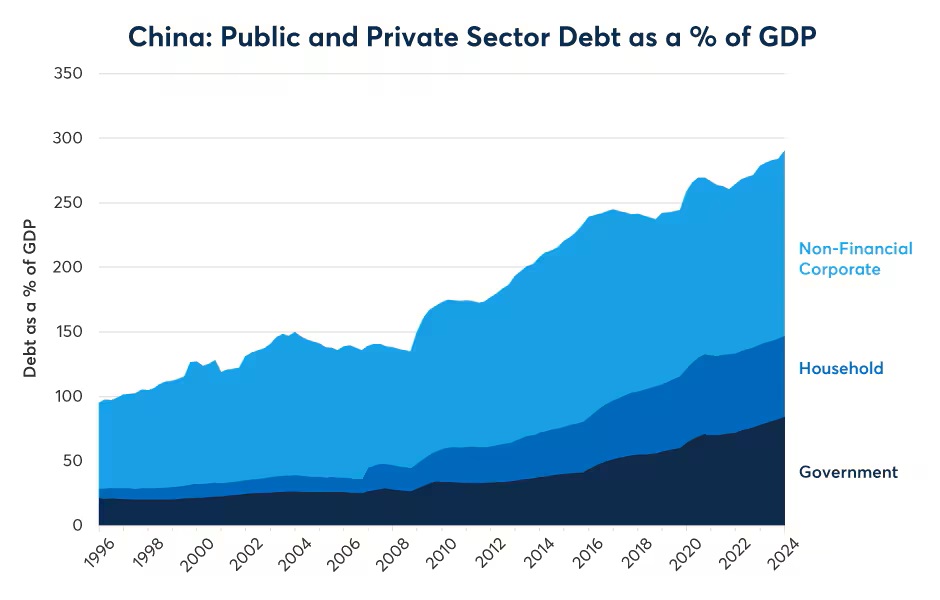

The 2009 stimulus differed in key aspects from the current one. First, it was much larger as a share of GDP. Between 2009 and 2010, non-financial corporate debt rose by 35% of GDP as the government encouraged a massive infrastructure building program (Figure 8). Thus far, the announced stimulus measures amount to about 3.6% of GDP, making it about one-tenth the size of the 2009-10 effort relative to the size of the economy.

Figure 8: China’s 2009 stimulus was large and occurred in a relatively low-debt environment

Source: Bank for International Settlements, Total Credit to the Non-Financial Sector Database (Q:CN:H:A:M:770:A, Q:CN:N:A:M:770:A, Q:CN:N:A:M:770:A) – Past performance is not indicative of future results.

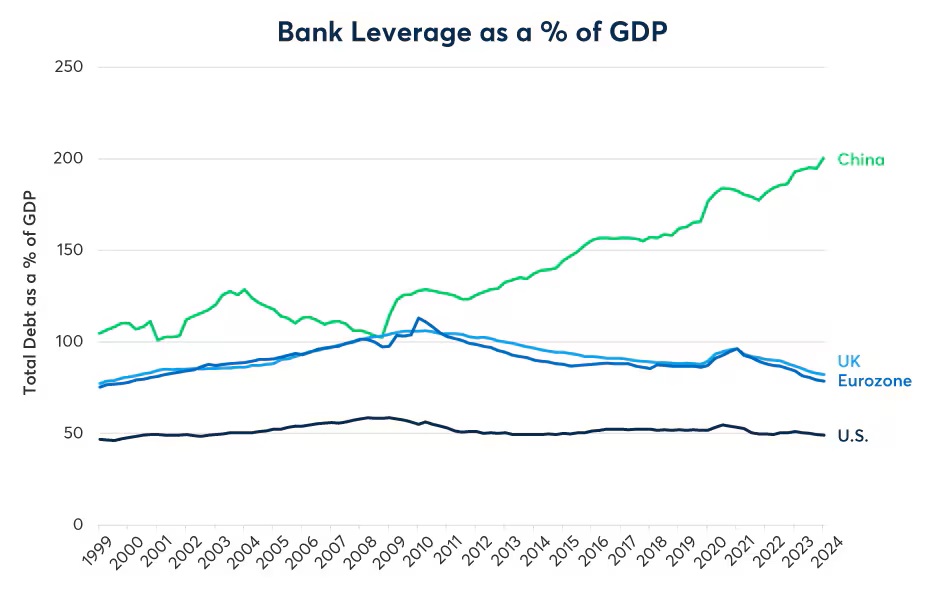

Second, the 2009-10 stimulus was meant to deal with the global financial crisis, which was exogenous to China. By contrast, the current stimulus is meant to deal with the endogenous problems of falling real estate prices, reduced consumer confidence and spending, weak finances on the part of local governments and property developers, and undercapitalized lenders. In fact, China’s lenders have total balance sheets that add up to nearly 200% of GDP (Figure 9), far higher than bank leverage ratios elsewhere.

Figure 9: China’s banks are exceptionally highly leveraged relative to the economy

Source: Bank for International Settlements, Total Credit to the Non-Financial Sector Database – Past performance is not indicative of future results.

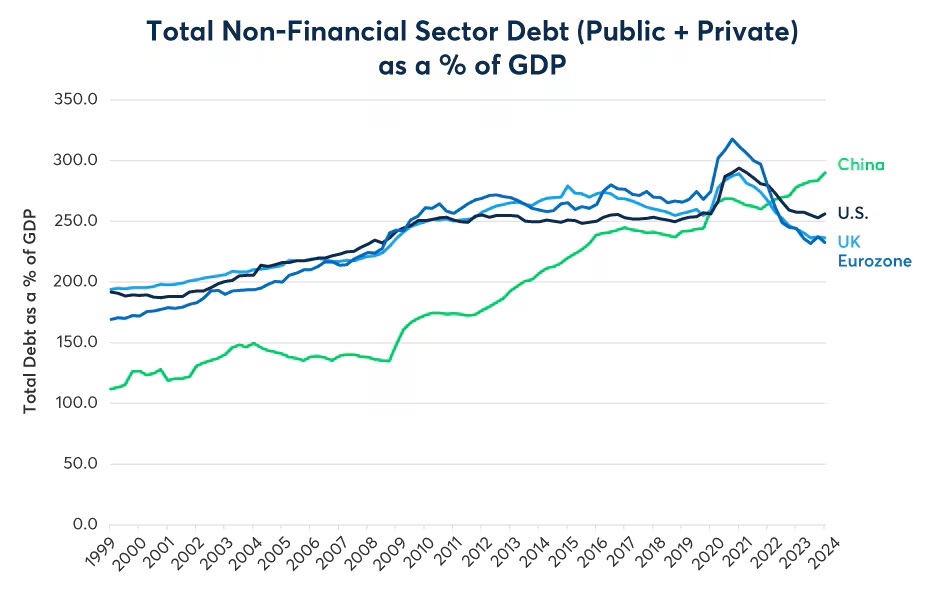

Third, higher debt ratios in the non-financial sector may also limit the effect of the stimulus measures. When the 2009-10 stimulus measures came into effect, the overall debt ratio was close to 140% of Chinese GDP – much lower than in Europe or the U.S. Today, China’s non-financial (or non-bank) leverage ratio is close to 300% of GDP, higher than in Europe or the U.S. (Figure 10). When debt ratios are low, additional borrowing can quickly add to the investment and spending components of GDP. By contrast, when debt ratios are high, additional borrowing often serves to refinance the existing stock of debt rather than add to the investment or spending components of GDP. Indeed, that seems very much the case with the existing stimulus proposals: allowing local governments to issue bonds to consolidate the debt of property developers onto their books and adding to the national public debt to boost the capital of the nation’s largest banks. This closely resembles what countries like the U.S., Ireland and Spain did in the 2008-2010 period. While such measures halted the economic downturn, they didn’t produce a particularly strong economic recovery.

Figure 10: China’s non-financial (non-bank) sector is highly leveraged

Source: Bank for International Settlements, Total Credit to the Non-Financial Sector Database – Past performance is not indicative of future results.

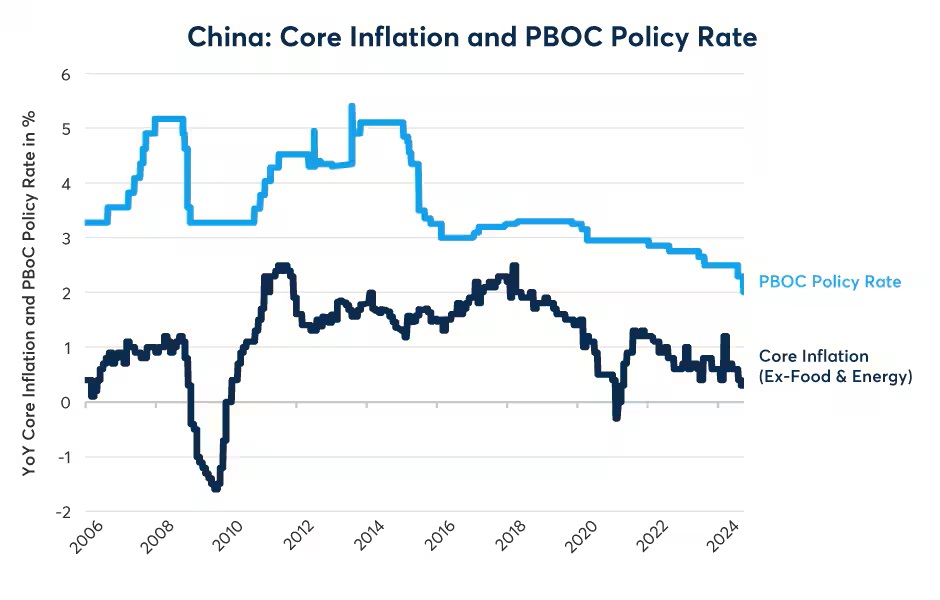

Finally, there is the issue of interest rates. While it is true that the PBOC has been cutting interest rates, it’s equally true that China’s core inflation rate has been falling. In fact, the gap between the PBOC’s policy rate and core inflation, which has been relatively stable over the past few years, is wider than it was at times in the past (Figure 11). This suggests that real rates in China have not in fact fallen and that monetary policy is China is not particularly easy for the moment. Giving a larger boost through monetary policy might require rates to move much closer to zero, but near-zero rates in China might also create pressures for capital flight and a weaker yuan which might make the PBOC reluctant to ease policy too much too soon. A sharply weaker yuan could fuel a protectionist backlash against China.

Figure 11: PBOC policy rates remain high relative to core inflation

Source: Bloomberg Professional (CHLLM1YR, PBOC7P, CNDR1Y, CNCPCRY) – Past performance is not indicative of future results.

A large part of the reason why commodity prices have been depressed despite conflicts in the Middle East and war between Russia and Ukraine is the weakness of Chinese demand growth. If China manages to halt or reverse the slowdown in its growth rate, the world could wind up with higher commodity prices. That said, the jury is still out on the degree to which China’s latest stimulus will boost growth.

Disclosure: CME Group

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account