Originally Posted, 4 October 2024 – What’s Hot: A roaring rebound for industrial metals

Key Takeaways

- China’s monetary stimulus is igniting demand for industrial metals.

- Copper and nickel are seeing strong gains due to supply concerns and construction demand.

- Silver shows upside potential, fuelled by its hybrid industrial and precious metal role.

- Related Products WisdomTree Industrial Metals, WisdomTree Copper, WisdomTree Energy Transition Metals

Industrial metals have seen a significant price uptick in recent days, driven by favourable macroeconomic conditions. The sector began its recovery when risk assets rallied following the US Federal Reserve’s 50 basis point interest rate cut last month. However, it was the monetary stimulus from the People’s Bank of China (PBOC) that truly ignited momentum in the industrial metals market.

In a recent blog post, we break down the key components of this stimulus package and explain why it is poised to benefit industrial metals. Since the package’s announcement, along with the Chinese government’s promise of additional fiscal stimulus, markets have responded positively, particularly towards Chinese equities. Industrial metals have also surged, riding this wave of optimism.

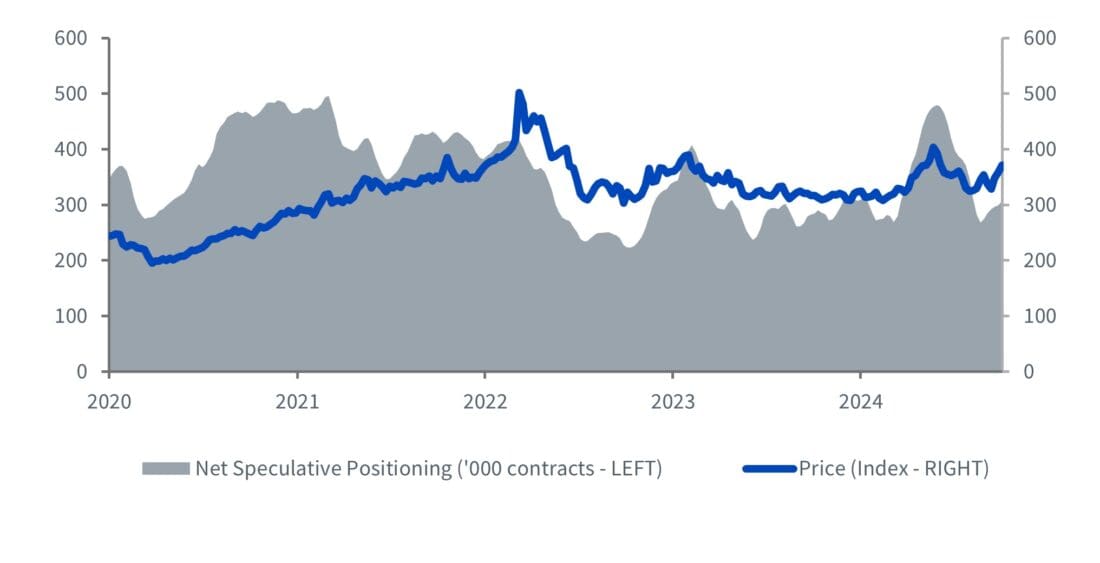

Sentiment in industrial metals has revived but could go much further

Source: WisdomTree, Commodity Futures Trading Commission (CFTC), Bloomberg. Weekly data as of 01 October 2024. Price reflects the Bloomberg Industrial Metals Subindex Net Total Return, which includes five metals – copper, aluminium, zinc, nickel, and lead. Net speculative positioning covers the same commodities. Historical performance is not an indication of future performance and any investments may go down in value.

Since May, when investor sentiment toward industrial metals briefly spiked (as shown in the chart above), net speculative positioning in the sector has been steadily declining. This decline has been driven largely by the perception that metals are well-supplied in the near term, particularly considering a cooling global economy and slowing demand from China. Rising inventory levels on futures exchanges have further reinforced this view. However, recent monetary stimulus from China and the prospect of additional fiscal measures are now fuelling hopes that base metal demand could increase meaningfully, even in the short term.

Industrial metals were up notably in September

| Copper | 8.5% |

| Nickel | 4.4% |

| Aluminium | 7.6% |

| Silver | 8.5% |

| Zinc | 7.3% |

| Tin | 3.0% |

| Lead | 1.7% |

| Platinum | 5.5% |

| Cobalt | 0.6% |

| Lithium | -8.6% |

Source: Bloomberg, data shows returns for September using the price of generic first futures contracts. Historical performance is not an indication of future performance and any investments may go down in value.

Copper has seen the most pronounced impact from China’s recent stimulus. Among the measures introduced by the People’s Bank of China (PBOC) are relaxed rules for homebuyers and lower mortgage rates, aimed at reviving the country’s struggling property market. Markets interpret this as a signal of a potential rebound in demand for construction materials like copper. However, China’s Caixin Manufacturing Purchasing Managers’ Index (PMI) fell into contractionary territory with a reading of 49.3 in September1. All eyes are now on how quickly activity picks up and whether we see an expansionary print in October.

Nickel prices have risen despite the International Nickel Study Group’s (INSG) forecast of a 170,000-ton surplus this year, largely due to lower demand projections, especially from the electric mobility sector. Nonetheless, market optimism fuelled by China’s stimulus measures and rising stainless steel prices has lifted nickel prices. With stainless steel production accounting for about two-thirds of nickel demand, markets are increasingly betting on an uptick in Chinese manufacturing activity. Another factor for nickel is the potential risk of supply disruptions, as Russia, one of the top five nickel producers, is considering limiting metal exports to the West.

Silver, a hybrid precious and industrial metal, is also worth mentioning. It has benefitted from the strong rally in gold this year. However, the gold-to-silver ratio is currently around 84, still significantly higher than the 20-year average of 692, suggesting further potential upside for silver, particularly if the industrial sector maintains positive momentum.

To conclude, we believe industrial metals remain reactive to evolving cyclical macroeconomic conditions. If China introduces fiscal stimulus in the coming weeks, this could be another catalyst to further fuel the rally in the sector. Investor sentiment too, as measured by net speculative positioning, still has considerable room to move upward.

1 Trading Economics, October 2024.

2 Bloomberg, data as of 03 October 2024.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account