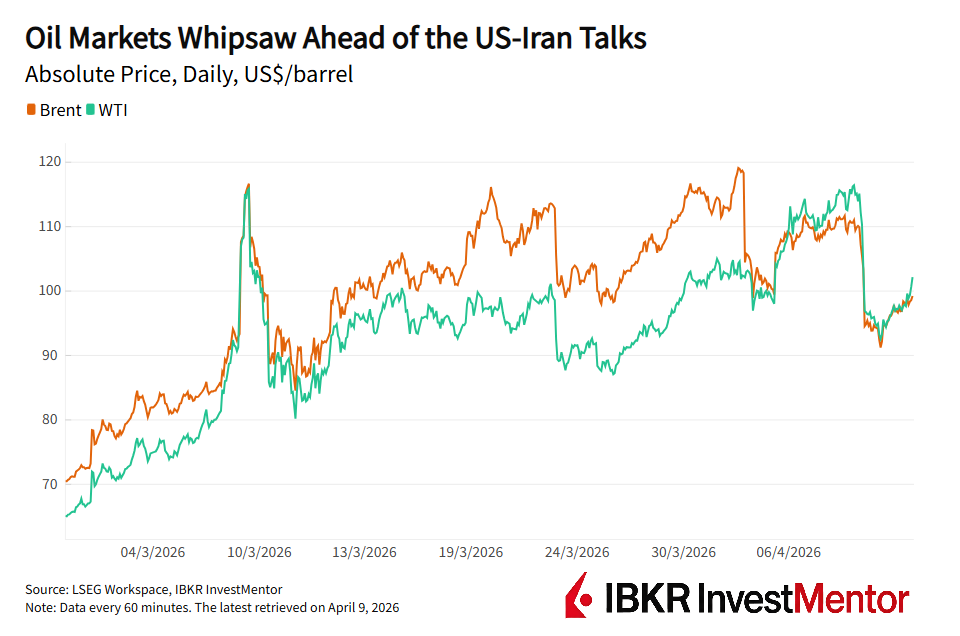

The Strait of Hormuz is among the most economically important places on the map. This six-week war has demonstrated that with brutal clarity, sending oil and gas prices soaring and raising fears of a worldwide return to the high inflation environment, perhaps even stagflation.

The strait is just a narrow stretch of water between Iran and Oman, barely 30 miles wide at its tightest point and with shipping lanes only about 2 miles wide. But it carries around 20% of the world’s oil and liquefied natural gas, and other crucial ingredients of the global economy, such as helium and fertilizers.

For decades, the risk around Hormuz was straightforward. Either the traffic flowed, or a crisis threatened to shut the route. Wars, standoffs, and naval incidents sometimes disrupted the strait, but it soon returned to normal, with ships passing freely, regardless of where they were from or where they were headed.

But then came the Iran war of 2026. It’s the first one to effectively shut the strait for weeks. After the two-week ceasefire was announced earlier this week, the relief across the markets was palpable: Maybe the strait would finally reopen, and the world economy would return to normalcy?

But even if the talks go well, normalization may not mean a return to the old rules. Iran is floating a different idea: keep the strait open but charge for access. Reportedly, it has already done that to a few Chinese ships seeking passage. If the tolls take hold, it would raise transport costs permanently and challenge long-held international rules on global maritime trade.

Past performance is not indicative of future returns.

From Choke Point to Priced Passage

Iran has now demonstrated how easily Hormuz can be disrupted. Attacks, threats, and insurance pullbacks were enough to drain traffic fast and send oil prices surging. That was the classic Hormuz playbook that analysts had warned about for years.

The new proposal flips the script. Rather than blocking the route, Iran would allow ships through, selectively and for a fee. Iran’s parliamentary committee has already approved the plan for the tolls, with the fees set reportedly at 1$ per barrel of oil.

That doesn’t sound too much until you do the math. A standard Very Large Crude Carrier (VLCC) carries about 2 million barrels. At that rate, a single transit could cost $2 million, before accounting for insurance surcharges, security costs, and delays. Around 140 vessels per day pass through the strait at normal times. This could potentially be extremely profitable for Iran.

The danger here is normalization. If access becomes conditional rather than automatic, oil and gas markets suddenly have to deal with this new permanent layer of uncertainty. It would also set a dangerous precedent, which could be abused at other chokepoints around the world.

In the future, Iran would not necessarily need to close the strait to influence outcomes. It could slow certain shipments, favor others, or quietly adjust risk for specific destinations or cargoes. Access could depend on timing, ownership, or politics, while still claiming the strait is “open.”

Oman Has a Say Too

There is another country in this story that often gets skipped. Oman.

The Strait of Hormuz runs through the territorial waters of two states: Iran on the north shore, Oman on the south. That matters because under international maritime law, including the UN Convention on the Law of the Sea, Hormuz is treated as a strait used for global navigation.

In plain English, ships have the right to transit without asking permission or paying tolls, except for very narrow safety reasons. Even though the strait is not in international waters, no single country legally controls the passage.

Oman has made clear it does not accept tolls or permission‑based transit. Gulf states that rely on the strait to export oil share that view. So do shipping companies, who are wary of any system that turns access into a negotiation.

But law and practice are not the same thing. Iran has shown that drones, missiles, sea mines, and armed speedboats can give real power regardless of legal arguments. That gap between rules and reality is what the markets are now grappling with.

Iran is also pushing for a more formal recognition: acknowledging Tehran’s control over the strait is part of its peace plan demands.

The “Joint Venture” Curveball

Into this mix stepped US President Donald Trump with a surprising suggestion: a US‑Iran joint venture to manage traffic and charge tolls together.

For now, it is an idea without detail. Turning it into reality would require trust, shared enforcement, and rules agreed by governments that were trading air strikes just days ago. Oman would still have to be on board. So would Gulf exporters and the shipping industry.

Even if such a framework lowered short‑term risks, it would raise a bigger question. Would it further legitimize the idea that Hormuz is a priced gateway, not a public shipping artery?

If you want to learn more about how the global economy works, download IBKR InvestMentor app for free, interactive lessons, and daily news explainers.

Learn more about InvestMentor

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account