Stocks are recovering from last week’s selloff as investors look ahead to retail and tech earnings in the next few days with AI juggernaut Nvidia taking center stage after the bell on Wednesday. Meanwhile, yields are catching a lift on rosier economic growth expectations as well as concerns about fiscal stimulus, which this morning drove the 30-year to its loftiest level since May. Also offering rates a bump was this morning’s stronger-than-projected homebuilder sentiment print, which has been consistently gaining ground since August and reached its highest level since April. And while construction folks are incredibly enthusiastic about sales into next year, the headline figure for this month remains in contraction territory, as buyer traffic is constrained with mortgages sporting a seven-handle. Still, participants in the space reported broad-based improvements in the sector, likely linked to expectations that the incoming administration will seek to bolster the real estate market.

Homebuilder Optimism Surges on Trump Win

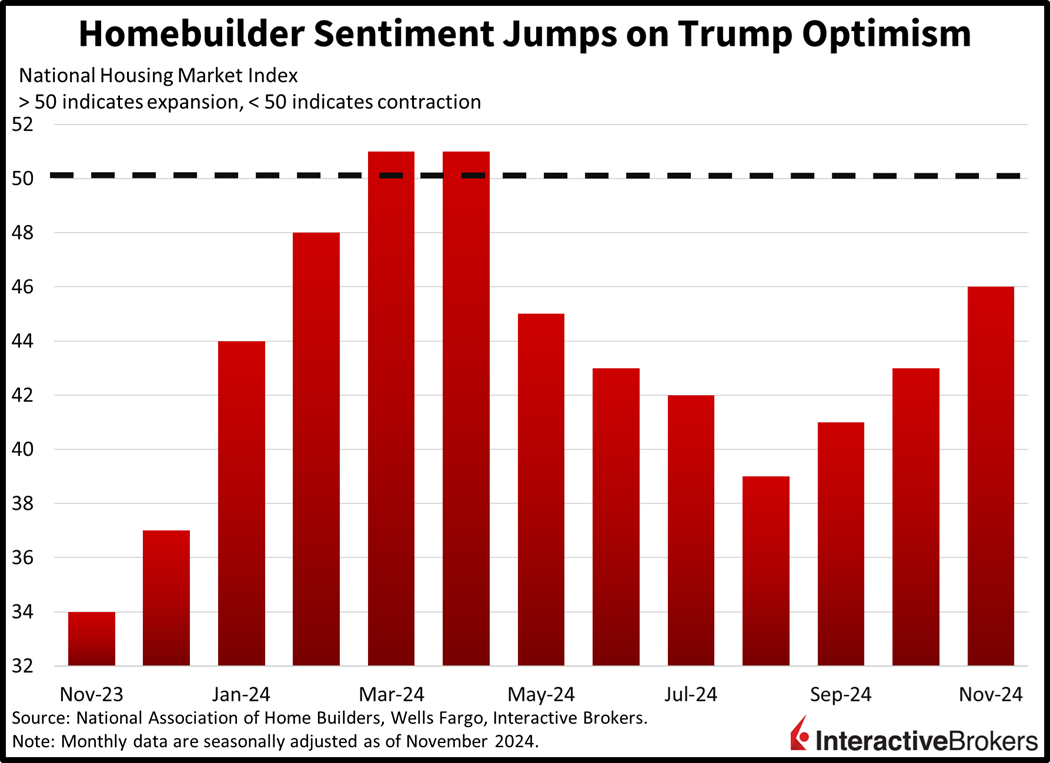

Sentiment among home construction companies has climbed to a seven-month high with the November NAHB/Wells Fargo Homebuilder Sentiment Index jumping from 43 to 46. Analysts anticipated a score of 44. This result was driven by optimism that the Trump Administration will ease regulations. Additionally, some builders believe that home shoppers who were reluctant to sign closing contracts due to uncertainty about the presidential race will resume their home searches now that the election is concluded. Conversely, with mortgage financing costs closely correlated with the bond market, rising yields on long-term debt during the past few weeks are concerning.

Past performance is not indicative of future results

Nevertheless, all three broad categories within the index improved, marking a three-month streak of the measurements moving somewhat in unison. Current sales conditions, which represents nearly 60% of the index’s makeup, rose from 47 to 49, while sales expectations in the next six months jumped seven points to 64. Finally, the NAHB gauge of traffic of prospective buyers advanced from 29 to 32.

In a related matter, the percentage of builders reducing prices was nearly steady, dropping from 32% to 31%. The size of the average price reduction declined one point to 5% and the use of sales incentives fell from 62% to 60%. Additionally, sentiment improved in two regions: the Northeast strengthened from 52 to 59 and the Midwest moved from 43 to 49. The South, however, declined from 43 to 42 while the West dropped from 44 to 39.

Trump Rally Resumes with Broad Equity Gains

Stocks are surging across the board as the Trump rally regains steam with all major benchmarks and sectors positive today. The Nasdaq 100, Russell 2000, S&P 500 and Dow Jones Industrial indices are 1%, 0.8%, 0.5% and 0.1% higher. The consumer discretionary, communication services and energy components are contributing the most with positive returns of 1.3%, 1% and 0.9%. Fixed-income is also responding to the animal spirits, with yields on the 2- and 10-year Treasury maturities changing hands at 4.33% and 4.47%, 2 and 3 basis points (bps) heavier on the session. The dollar is paring some of its recent progress, however, with the greenback’s gauge lower by 17 bps. The US currency is deprecating versus the euro, pound sterling, franc and Aussie and Canadian counterparts but is appreciating relative to the yen and yuan. Commodity majors are pointing north with crude oil, silver, gold, copper and lumber gaining 3.1%, 3.1%, 1.9%, 1.2% and 0.3%. WTI crude oil is trading at $69.03 per barrel on rising hostilities between Moscow and Kyiv.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account