Today was a “rip up the script” day. It originally seemed reasonable to focus on key economic news: the reports on December PCE and 4Q GDP. Although we were aware of the possibility that the Supreme Court could rule today on the legality of tariffs imposed under emergency authority, several possible prior decision dates had come and gone without comment. That changed at 10 AM ET when the Justices ruled against the President’s ability to authorize tariffs under emergency authority in a 6-3 decision.

First things first. The economic reports disappointed, though not with too noticeable of an impact on markets. Core PCE rose by 0.4% on a month-over-month basis, above the 0.3% consensus. There is no obvious way to put a positive spin on a higher-than-expected reading on the Fed’s preferred inflation measure, but that report nonetheless had little impact on rate cut expectations. Today, as yesterday, we see one rate cut fully priced in for July and a second priced in for December. The underlying odds diminished only very slightly.

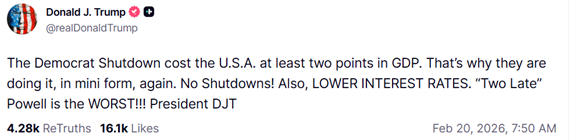

GDP came in significantly lower than anticipated, at an annualized 1.4%, which was well below the consensus expectation of 2.8% and the prior quarter’s 4.4% reading. For better or worse, some of the bad news was already priced in about 40 minutes earlier, when President Trump posted the following:

It certainly seems as though the President leaked the direction of the GDP data. Prudence now dictates that traders should monitor social media ahead of economic reports that the White House receives in advance.

Even before the tariff decision, traders once again demonstrated their ability to turn economic lemons into stock market lemonade.

The S&P 500 (SPX) opened about 20 points lower but had already crossed the unchanged line before the Supreme Court’s ruling. The weaker GDP report was treated less as a cause for concern than an excuse to reverse some of the recent rotation from growth into value. This morning, stocks bounced almost immediately after the market opened even as value stocks meandered around their initial lows. As noted above, there was no meaningful change in rate cut expectations, so the pre-ruling move was more about trader preferences.

Remember, investors recently began to favor more economically sensitive cyclical stocks after years of favoring growth stocks. Comparing two extreme examples, Microsoft (MSFT) is down about 18% this year while Deere (DE) is up about 40% after an 11% post-earnings rally yesterday. If you’d like some perspective on how rapid these moves have been, bear in mind that the year is only seven weeks old.

Thus, some of this morning’s trends were already in place before the 10 AM ruling. It was key news, but even though the exact timing came as a modest surprise, prediction markets had been indicating an expectation that the verdict would occur in this manner. I was asked for immediate comments, and I stand by these initial responses:

“Huge news, though hardly unexpected. That’s why the initial reaction was a big spike that faded a bit. This is certainly a positive for many stocks and the economy as a whole. But the fact that yields have only moved up about 2 bp is a ‘tell’ that the economic benefit is perceived as modest.”

“The tariff decision is clearly good news for the economy as a whole and certain sectors specifically, but the impacts are muted because it was widely expected and the talk is immediately turning to other tariff measures that the administration can take. If it was wildly positive for the economy and created a big deficit shortfall, we would expect to see yields move even higher than they are. 2 bp isn’t much. Interesting to see that no sectors are really standing out. [Communications] is the best performer, which is more about general market sentiment than tariff enthusiasm.”

Tuesday night’s State of the Union address just got quite a bit spicier. Despite the potential for fireworks aimed at the Justices who typically take front row seats, investors should instead listen carefully to what the administration’s “Plan B” might be. We also need to be vigilant about whether the on-again, off-again saber rattling about Iran takes another nasty turn. But the most immediate attention should turn not toward the White House but to whether today’s interruption in the recent relentless rotation is temporary or a sign that it might have run its course for a while.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account