A colossal miss on fourth-quarter GDP raised economic slowdown worries and sent equities south prior to a ferocious recovery into the green after the Supreme Court ruled intraday that President Trump’s tariffs are illegal. Despite the White House remaining committed to finding alternatives to maintain the levies, investors stepped up to the plate and bought the dip, with potential government refunds to corporations expected to provide a short-term tailwind to profitability. But Treasuries went the other way because import levies have been a key factor in reducing budget deficits so their demise could worsen the fiscal picture, all else being equal. Stronger-than-expected price pressures in this morning’s PCE report alongside a beat on new home sales also contributed to sending yields north although the climb has been modest, offset by a trio of weaker-than-anticipated reports concerning growth, flash PMIs and UMich Consumer Sentiment. Elsewhere, the greenback is catching bids as well as the commodity majors minus crude oil and rate sensitive lumber. Volatility protection instruments were seeing heavier premiums; however, significant buying activity following the SCOTUS decision led traders to unwind hedges.

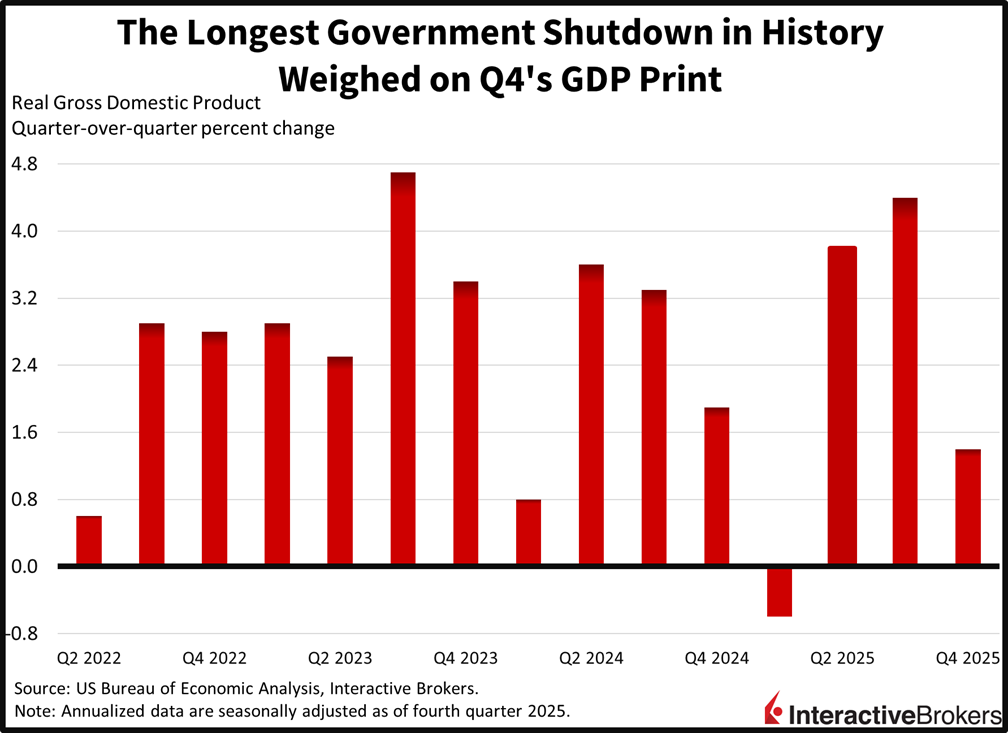

Washington Turmoil Hurts GDP

Fourth-quarter GDP grew at a much slower than expected pace of 1.4% as the government shutdown weighed on activity to end last year. The headline figure was well below the projected 3% and the prior period’s 4.4%. Still, consumer spending and business investment remained buoyant, offsetting the softness in fiscal outlays, residential capital expenditures and net exports. The drop in federal expenses trimmed 1.1% from fourth-quarter growth while an uptick in private inventories added 0.21%.

Past performance is not indicative of future results.

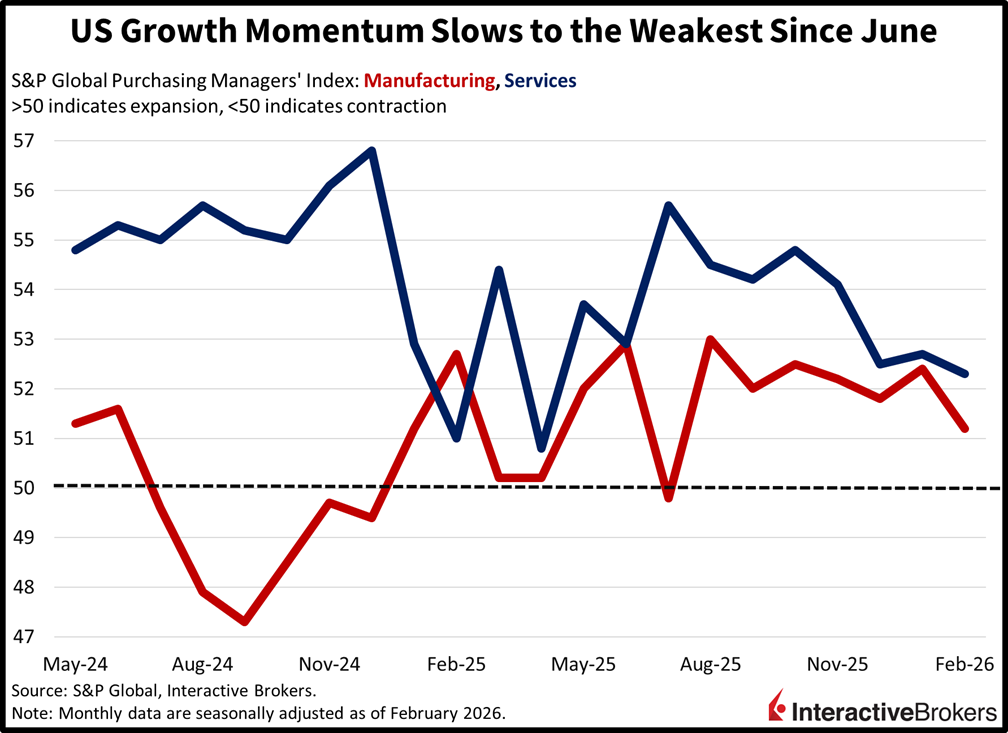

February Activity Drops to June Levels

Economic growth slowed in February as sluggish demand, elevated costs, slow hiring and adverse weather conditions weighed on activity in both the services and manufacturing sectors. The Flash Purchasing Manager’s Indices (PMI) from S&P Global came in at 52.3 and 51.2 across the segments, weaker than the 53 and 52.6 expected and the 52.7 and 52.4 from January. Inflationary forces, which especially dampened exports, stemmed from increased input charges, wage pressures and tariffs. Still, corporate sentiment improved significantly as executives remained optimistic about the outlook due to lighter taxation, milder regulations, and rate cuts on the horizon that are incentivizing substantial capital expenditures.

Past performance is not indicative of future results.

Delayed Inflation Data Hotter than Expected

Stale Personal Consumption Expenditures (PCE) data, delayed due to the shutdown, reflected December prices rising 0.4% month over month (m/m) and 2.9% year over year (y/y), a tenth higher than expected on both fronts. The core figures, which exclude food and energy, also exceeded projections by the same amounts, increasing 0.4% m/m and 3% y/y. During the month, meanwhile, a 0.4% increase in spending outpaced the 0.3% income gain, driving the savings rate down to 3.6%, a 38-month low.

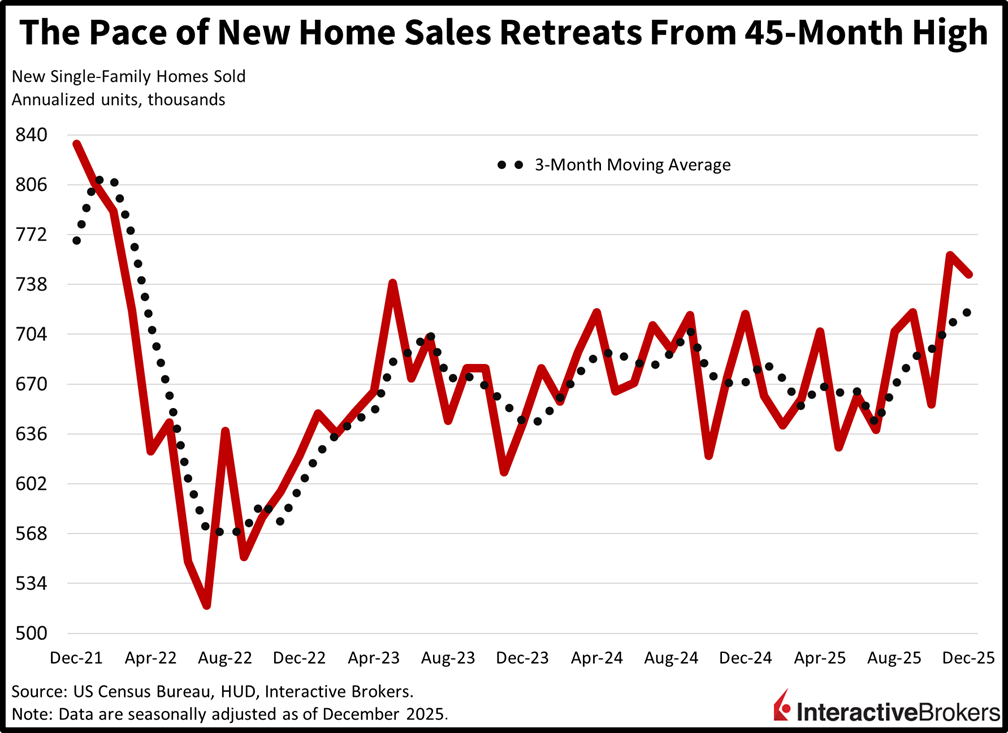

New Home Sales Weaken From 45-Month High

December new home sales declined 1.7% m/m from a 45-month high to a pace of 745k seasonally adjusted annualized units, as the Northeast and South regions weighed on performance with 37.3% and 6.7% descents. The fall was partially countered by increases of 31.7% and 9% in the Midwest and West. Inventories declined to a month’s supply of 7.6 from 7.7 and median and average closing prices rose 4.2% y/y and 0.5% m/m.

Past performance is not indicative of future results.

Consumer Sentiment Revised Down, Trio of 56.6s

The University of Michigan’s February Consumer Sentiment gauge was revised down to 56.6 from the preliminary estimate of 57.3, a result of current conditions, originally at 57.7, sinking to 56.6 as the buoyancy expressed by stock market participants was offset by folks without equities. Meanwhile, the future expectations reading remained steady at 56.6 as well, a trio of 56.6s indeed. Inflation projections were also adjusted lower by 0.1%, as the 1- and 5-year rates slipped to 3.4% and 3.3%.

Confusion Ushers in the Weekend

There’s a heavy amount of confusion on Wall Street ahead of the weekend concerning the economic outlook, what could occur on the tariff front and how disagreements between Washington and Tehran will be reconciled. This morning’s data were weak in aggregate, the Supreme Court decision came as an intraday surprise to investors and participants are wondering if imminent military action will occur in the Middle East. Despite the angst, the reacceleration theme remains intact, and consumption and employment are poised to remain supportive, but there’s no doubt that there’s risks of much higher interest rates stemming from a worsening fiscal picture and a surge in crude oil prices. It was precisely the surge in energy costs that drove the Fed to hike 525 basis points in 2022 following Russia’s invasion of Ukraine, as inflationary figures would have been much more contained if they weren’t accompanied by loftier gasoline charges. For now, investors are forced to wait and see how President Trump responds to the SCOTUS’s ruling as well as how he handles Iran’s nuclear threats to inform portfolio positioning.

International Roundup

Retail Sales in Canada Falter

Canadian shoppers trimmed their outlays by 0.4% m/m in December, a slightly lower descent than the 0.5% drop anticipated by a consensus of economists. In November, retailing was 1.2% higher than in the preceding month. December retailing was also 0.4% lower than in the final month of 2025, a notable weakness relative to the 1.2% y/y gain in November.

While the volume of sales was unchanged, transaction values sank in three of nine subsectors, with motor vehicle and parts dealers experiencing a 1.6% decline, the sharpest contraction during the month. Conversely, gasoline stations and fuel vendors enjoyed a 2.8% gain.

While Input Costs Grow Faster than Gate Prices

Gate prices in Canada were up 2.7% m/m and 5.4% y/y, significantly trailing the 7.7% and 8% m/m and y/y ascents of raw materials, according to the Industrial Product Price and Raw Materials Price indices. Among finished products, non-ferrous metal items and energy/petroleum surged 18.2% and 1.7% m/m. Chemicals and lumber were up 2.2% and 1.4% while vehicles were 0.7% more costly. Input cost pressures were led by metal ores, concentrates and scrap becoming 15.6% more costly while crude energy product stickers were up 4.6%.

Eurozone Manufacturing Lifts Composite PMI

Eurozone economic activity climbed to a three-month high this month with both services and manufacturing sectors strengthening, according to the HCOB Flash Eurozone Composite PMI. Despite the broad gains, however, expansion within the goods producers was minimal. The composite climbed from 51.3 to 51.9, depicting an economy that is solidly above the contraction-expansion threshold of 50. Economists anticipated a 51.5 result

The gain was supported by the manufacturing sector’s 50.8 print following the January result of 49.5. The level, while only slightly above the contraction-expansion threshold, significantly outperformed the economist consensus estimate of 49.9. At the same time, the services sector climbed from 51.6 to 51.8, narrowly missing the estimate of 51.9. In manufacturing, production experienced the sharpest rise since August 2025, helping to push the sector’s headline to a 44-month high. Additionally, new order growth increased for the first time in four months, hitting the fastest growth pace in almost four years. Goods producers also increased their purchasing but continued to reduce payrolls.

In the services sector, staffing levels were unchanged after five years of expanding workforces. More broadly, input prices increased across both manufacturers and service providers at the fastest rate in 34 months. Firms increased their gate fees, but at a slower pace than input inflation. Regarding firm’s expectations, manufacturers’ sentiment reached a four-year high and services providers, while confident that activity will increase over the next 12 months, were slightly less optimistic.

UK Retail Sales Growth Surpasses Expectations

The volume of UK retail sales grew 1.8% m/m in January, solidly outperforming the 0.2% gain expected by economists and accelerating from December’s 0.4% advance, according to the Office for National Statistics (ONS). Relative to January 2025, the volume was up 4.5%. Economists anticipated 2.8%. In December, sales volumes were 1.9% higher than in the year-ago period. The m/m print received a boost from auction sales of artwork and antiques. Online sales of sports supplements and jewelry were additional tailwinds. Jewelers noted that demand hit unprecedented levels.

Hong Kong Unemployment Rate Creeps Up

Hong Kong’s unemployment rate of 3.9% during the November through January period was up from 3.8% during the three-month period ended in December. In the recent print, the number of individuals punching the time clock sank by 1,100. The unemployment rate grew in the insurance sector, construction industry and financing category while easing in the transportation classification and the cleaning and similar activities industry. A government spokesman acknowledged that businesses are experiencing challenging operating environments but maintained that sustained economic growth should buttress the labor market.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account