A heightening of Middle Eastern tensions has investors running for cover this morning following Israeli attacks against Iran. The conflict is propelling inflation expectations via the cost of crude oil, which advanced as much as 12% in a single session, on worries that supplies could be disrupted in the region. The sharp gain is especially problematic for a marketplace that was cheerful due to back-to-back lighter-than-projected price pressure reports this week that bolstered rate cut hopes and widened the path for additional upside in stocks. Furthermore, a pivotal focus of the Trump administration is subdued gasoline costs through expanded production levels as a way to hedge the potential for tariff-sparked charge forces. The geopolitical violence has traders ignoring today’s much better-than-anticipated consumer sentiment print, as they unload equities in all sectors ex energy, Treasuries across the curve, bitcoins and the copper and silver commodities. But folks are increasing their exposures to volatility protection instruments, the greenback, forecast contracts and the energy, lumber and gold commodities.

US Consumer Sentiment Rebounds

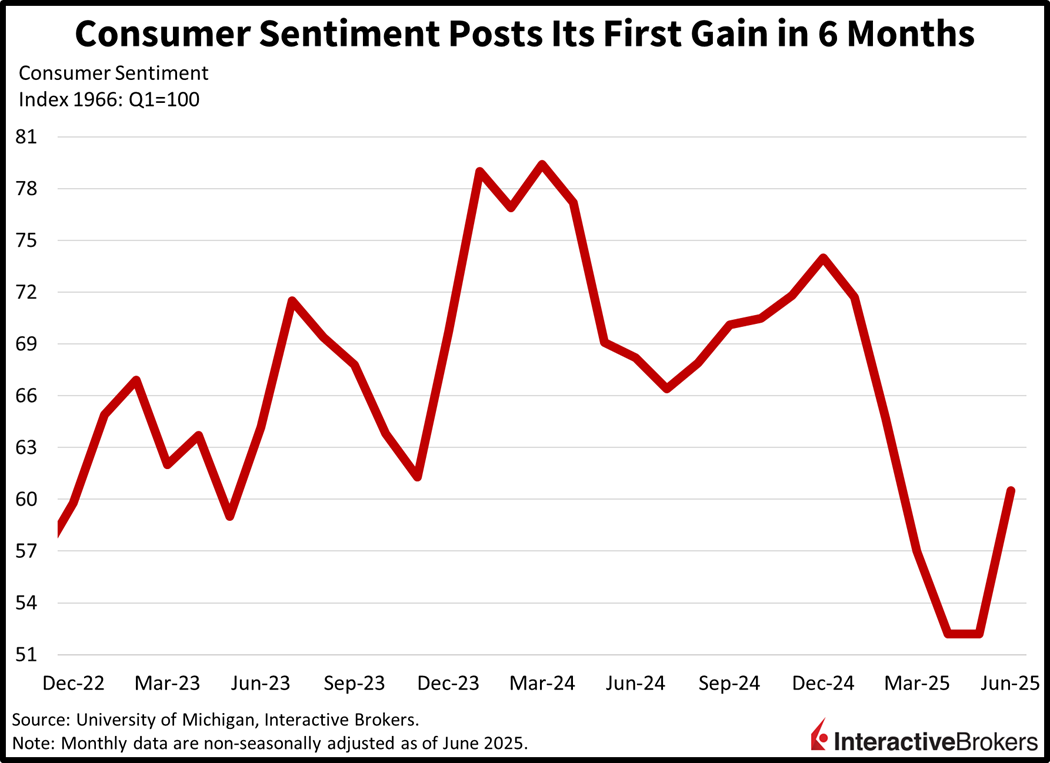

A comeback in the stock market and softer-than-feared Trump tariffs drove a significant increase in the University of Michigan’s consumer sentiment print this morning. It was the first gain in six months and the 60.5 level reported in June was much better than the 53.5 median estimate and the 52.2 from May. The sub-indices for current conditions and future projections rose from 58.9 and 47.9 to 63.7 and 58.4, well above the estimated 59.4 and 49. The short- and long-run inflation expectations segments declined to 4.1% and 5.1% over 1- and 5-years, below the prior month’s 4.2% and 6.6%.

Can’t Afford Spiking Energy Prices

A potential spike in energy prices would be a significant problem for the economy and markets. A prolonged conflict during which oil supplies are reduced and costs surge above $85 per barrel could threaten a return to a 3-handle on the Consumer Price Index; it almost reached $78 last night. That kind of increase would certainly deter the Federal Reserve from reducing short-term yields and may push central banks around the world to begin raising rates. Furthermore, heavier stickers for gasoline, diesel and jet fuel would likely pressure corporate margins since shoppers have been balking at loftier charges lately amidst a decelerating labor market and ongoing budgetary stress. What stocks and Treasuries need for resumed upside is a quick de-escalation because without it, risk premiums, volatility and inflation expectations will march higher, hurting equities and fixed-income assets simultaneously while benefiting gold.

International Roundup

Europe’s Industrial Production Slows

Industrial production in the euro area sank 2.4% month (m/m) in April, significantly below the -1.7% median forecast and the preceding month’s 2.4% gain. The metric was up only 0.8% year over year (y/y) with economists expecting a 1.4% jump following the last reporting period’s 3.7% boost. Also in April, the region’s trade surplus shrank from $37.3 billion to $9.9 billion, well below the expectation for $18.2 billion.

Japan’s Industrial Output Falls

Japan’s industrial production retreated 1.1% m/m in April, slightly better than the prediction of -0.9% but a reversal from the 0.2% increase in March. The Tertiary Industry Activity Index, a measurement of services, descended 10.90 points after increasing 14.90 in March.

Cold Weather Heats Up Canada’s Capacity Utilization

Canada’s industrial sector utilized 80.1% of its capacity during the first three months of this year compared to 79.7% during the final quarter of 2024, according to Statistics Canada. Economists predicted an increase to 79.8%. Below normal temperatures heated up activity in the electric power generation, transmission and distribution sector with the portion of capacity operating in the first quarter climbing from 83.2% to 86.1%. In a related matter, the mining, quarrying and oil gas extraction sector rate moved north by 0.7 percentage points to 76.7%.

Conversely, manufacturing weakened with activity relative to capacity falling 0.2 percentage points to 77.9%. Within this category, the petroleum and coal product manufacturing segment and the fabricated metal group fell 6.9 and 3.1 percentage points, respectively.

Canada Wholesale and Manufacturing Sales Volumes Retreat

US tariffs appear to have hit Canada’s wholesale and manufacturing sales in April. Sales on the wholesale level dipped 2.3% m/m, worse than the forecast for -0.9% and March’s 0.2% result. Meanwhile, manufacturing sales sank 2.8% compared to the estimate of -2 % and March’s -1.4% result.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account