Markets are extending their rebound today even as attacks intensify in the Middle East. Investors are looking to the tech, earnings, economic and political fronts for buying motivation following Nvidia’s $1 trillion revenue projection, Delta’s beat-and-raise, ADP’s healthy weekly hiring figures and White House comments that are propelling optimism on Wall Street. Indeed, strengthening confidence regarding the future of AI, firmer discretionary consumer spending prospects and the stable state of employment in conjunction with NEC Director Kevin Hassett saying that the war will end in weeks and not months have stocks rallying strongly while Treasuries advance more modestly. An intraday pending home sales print arriving above estimates didn’t hurt either. Every equity sector, sub-category and major benchmark is gaining; however, fixed income is being held back by ongoing elevated inflation expectations, driven by a WTI oil price that is still north of $90 per barrel. Meanwhile, a weaker greenback and revitalized animal spirits are lifting the commodity complex overall, although copper is an exception. Elsewhere, lessening hedging demand resulting from offensive attitudes is depressing premiums on volatility protection instruments.

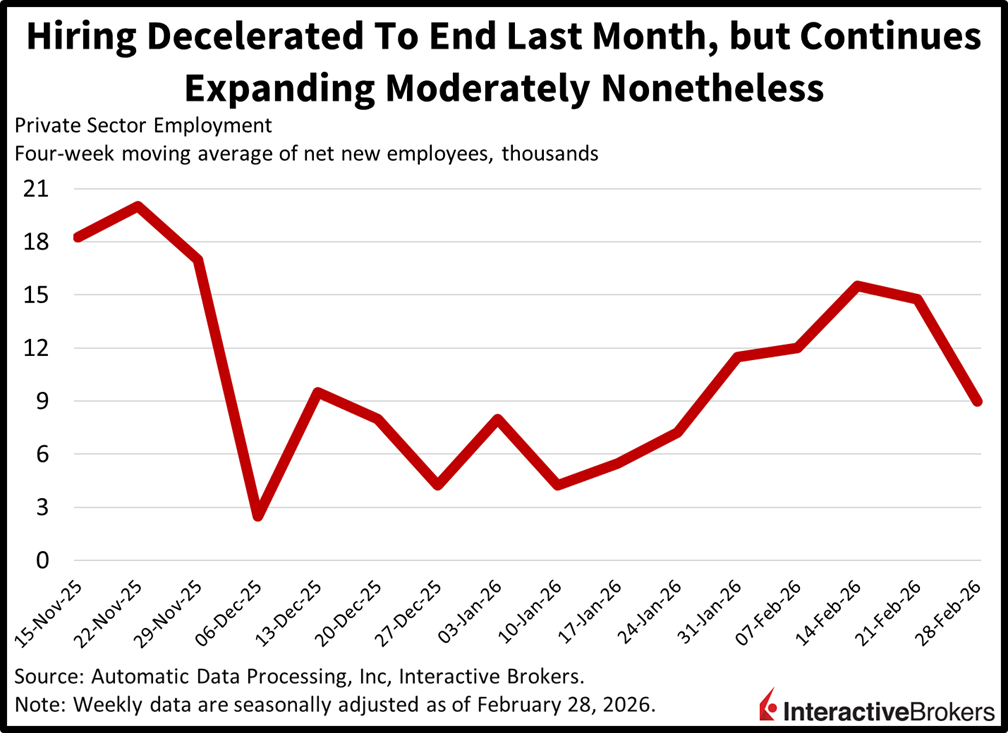

ADP Hiring Reflects Modest Slowdown

Private sector payrolls decelerated to end last month but nonetheless continued expanding moderately. Rosters increased by an average of 9k workers in each of the four weeks during the period that ended Feb. 28, below the 14.75k reported in the prior interval, according to ADP. Despite the slowdown, the print still exceeded the first four weeks of the year during which the gains were all lower than 8.1k.

Past performance is not indicative of future results

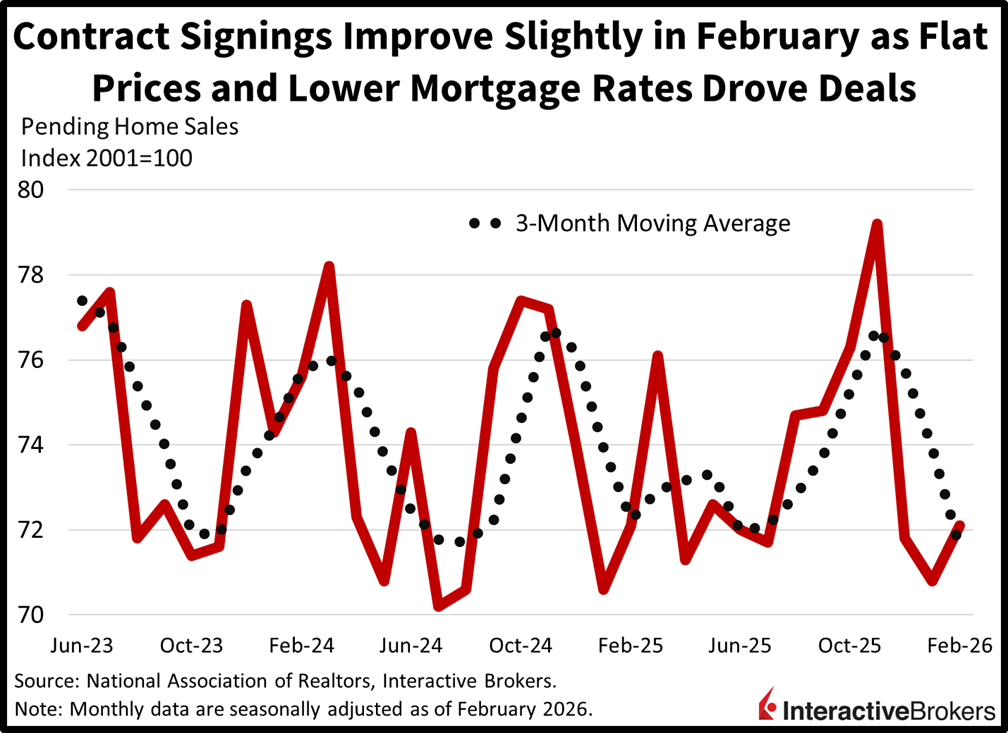

Pending Home Sales Improve

Slowly improving inventories, flat valuations and sliding mortgage rates last month drove an improvement in pending home sales. Contract signings for homes rose 1.8% month over month (m/m) in February, much stronger than the -0.5% expected and January’s 1% decline. Results were restrained, however, by a 3.6% m/m reduction in the Northeast, a region that notoriously has supply constraints amidst stringent building regulations. More encouragingly, in the Midwest, South and West, deals grew 4.6%, 2.7% and 0.9% m/m. Despite the progress, the recent climb in long-dated yields threatens to keep the real estate sector in contraction over the longer term as construction, transactions and renovations are increasingly out of reach when financing costs rise.

Past performance is not indicative of future results.

Fed To Consider One-Time Shock Vs. Lasting Effect

As the Fed meets today and tomorrow to make an interest rate decision, a key focus across the committee is whether the Middle East war will cause a one-time shock to inflation or a lasting effect. Although a pause is widely expected, surging oil prices are clouding the outlook for future cuts, with Wall Street anticipating only a single 25-basis point (bps) reduction in 2026 after having previously believed policymakers would cut two or three times this year. Meanwhile, some of the Fed’s global counterparts have begun moving in the other direction or are considering hikes in light of greater risk stemming from heavier energy costs. Indeed, Australia hiked this morning, and the EU and the UK are carefully contemplating if they should begin raising as well. The Iran conflict is leading to substantially tighter financial conditions in a similar way as Russia’s invasion of Ukraine did, an event that if avoided would’ve only led the Fed to lift its benchmark by about 400 bps rather than 525 back in 2022. Against this backdrop, Fed Chair nominee Kevin Warsh faces a challenging road ahead, as he balances the institution’s 2% objective with a commander in chief that wants imminent loosening. Finally, our real-time indicator of the CPI is running at 3% in March, which is an unfortunate circumstance after January and February printed at 2.4%. The unfavorable dynamic weakens the argument for near-term trims, as a 3-handle on CPI signals an even loftier number on PCE, due to the latter weighing decelerating housing expenses less than the former.

International Round Up

Reserve Bank of Australia Tightens

Australia’s central bank hiked its key cash rate from 3.85% to 4.10% this morning, citing concerns that risks to price stability have increased with the Iran war causing oil to become more expensive while disrupting supply chains. In making its second hike of the year, the Reserve Bank of Australia maintained that inflation is likely to remain above target for some time. Additionally, while developments in the Middle East are uncertain, a wide range of scenarios for the conflict could increase price pressures. Five of nine members voted in favor of the increase. The organization is expected to hike again in May.

Singapore’s Trade Surplus Contracts

Singapore’s trade surplus sank from S$12.5 billion in January to S$4.5 billion last month with the growth of non-oil exports, or NODX, and re-exports decelerating.

Shipments within the NODX category climbed 4% year over year (y/y) and 3.9% m/m following 9.2% and 0.6% jumps in January. In this segment, integrated circuits and disk media product exports grew while non-electronics fell. Re-exports also weakened, falling from a 51.3% gain in January to a 21.9% increase last month.

South Korea’s Export Price Jump

South Korea exporters charged 10.7% more in February than in the year-ago period, a significant acceleration from the 7.8% y/y gain in January. On a m/m basis, stickers were up 2.1% compared to January’s 4% hike. February’s import prices, meanwhile, climbed 1.2% y/y and 1.1% m/m following a 0.9% y/y drop and 0.7% m/m increase in January.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account