Originally posted 6 Jan 2025 – Global X 2025 Outlook

The equity market outlook for 2025 reflects the complex interplay of global macroeconomic conditions, evolving geopolitical dynamics, and sector-specific trends. While the US economy demonstrates resilience, challenges such as persistent inflation remain.1 Conversely, Europe faces structural hurdles which continue to weigh on growth, yet undervalued sectors, particularly infrastructure and nuclear energy, where fiscal support and policy initiatives could serve as catalysts for future growth.

Painting the Macroeconomic Picture

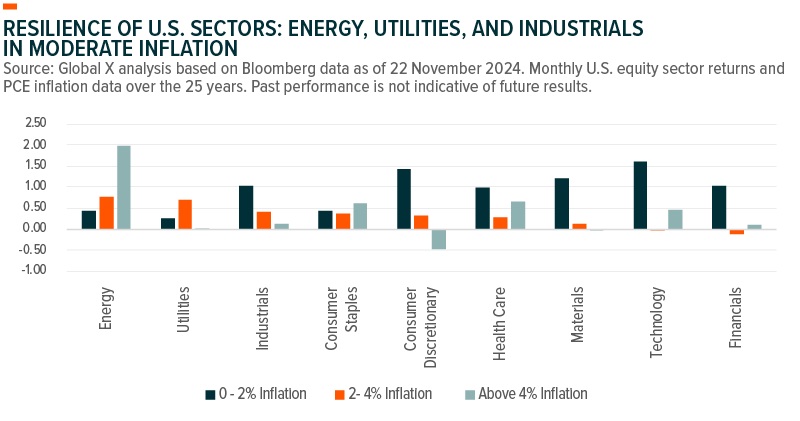

In the U.S., inflation could remain moderate in 2025, with markets anticipating two to three rate cuts amid a post-election surge in consumer and business sentiment.2 Following the resolution of election-based uncertainty, businesses may accelerate their capital spending on previously delayed projects if trends observed following Trump’s 2016 electoral victory are mirrored. Improved optimism surrounding regulatory and tax relief, and boosted investment demand, contributed to a significant rise in project activity by early 2017.

In Europe, growth faces external challenges. Chief amongst them is a slowing Chinese economy, a strong U.S. dollar, and capital outflows to U.S. equities. However, opportunities could emerge if undervalued equities gain appeal, and a weaker euro supports a potential rebound in exports. The European Central Bank’s anticipated rate cuts by mid-2025 could stimulate economic activity by significantly lowering borrowing costs for approximately €1.1 trillion in planned infrastructure projects, potentially providing a significant boost to GDP growth.3, 4

“With fiscal tailwinds and policy-driven initiatives, 2025 potentially offers growth opportunities in undervalued sectors like infrastructure and nuclear energy, despite global economic challenges.”

Regional Insights

In the U.S., bipartisan policies such as the Infrastructure Investment and Jobs Act (IIJA) and CHIPS Act could drive growth across both infrastructure and semiconductors.5 More than half of the IIJA’s $1.2 trillion funding remains currently unallocated, alongside $3 billion from the CHIPS Act.6, 7 While proposed tariffs and stricter immigration policies could exacerbate labour shortages and inflation in sectors like manufacturing and construction, the evolving regulatory and trade landscape, under a Republican administration, may accelerate reindustrialisation efforts to mitigate potential supply shocks and strengthen domestic production.8

In Europe, the NextGenerationEU fund and the Cohesion Policy will look to drive progress across projects spanning renewable energy, digital transformation, and public-private partnerships. Notably, approximately 60% of the Recovery and Resilience Facility’s €723.8 billion budget remains unallocated, highlighting infrastructure and clean energy projects, potentially including nuclear power. Additionally, the €392 billion Cohesion Policy funds continue to be distributed, further supporting regional development initiatives.9, 10

Sector-Specific

Defence Technology

Global defence spending is rising, driven by ongoing conflicts in Europe, the Middle East, and Asia. Germany, for instance, has met NATO’s 2% GDP defence spending target for the first time since the Cold War.11 This surge in defence budgets is fuelling seemingly growth in advanced military technologies, such as AI, cybersecurity, and autonomous systems.12 Shifting U.S. policies that prioritise modernised capabilities might further amplify this trend, although not guaranteed.

Infrastructure Development

Both the U.S. and Europe remain critical hubs for growth in infrastructure modernisation, semiconductor manufacturing, and energy transitions. If the Inflation Reduction Act (IRA) is repealed under the new administration, the remaining public funding would be available for allocation.13 In Europe, attractive valuations may present additional potential with a value tilt.14 As the U.S. and Europe look to navigate these pivotal moments, regional differences in valuations and economic growth could shape investor preferences.

A Strategic Investment Approach for 2025

In 2025, persistent inflation and fiscal pressures require careful portfolio construction. By focusing on diversification, forward-looking strategies, and risk management, investors can navigate this complex landscape.

Diversified strategies to mitigate risks associated with geopolitical and macroeconomic uncertainty.

Navigating Volatility: Equity Income and Derivative Strategies Amid Trade Policy Shifts (by Alexander Roll)

Key Takeaways:

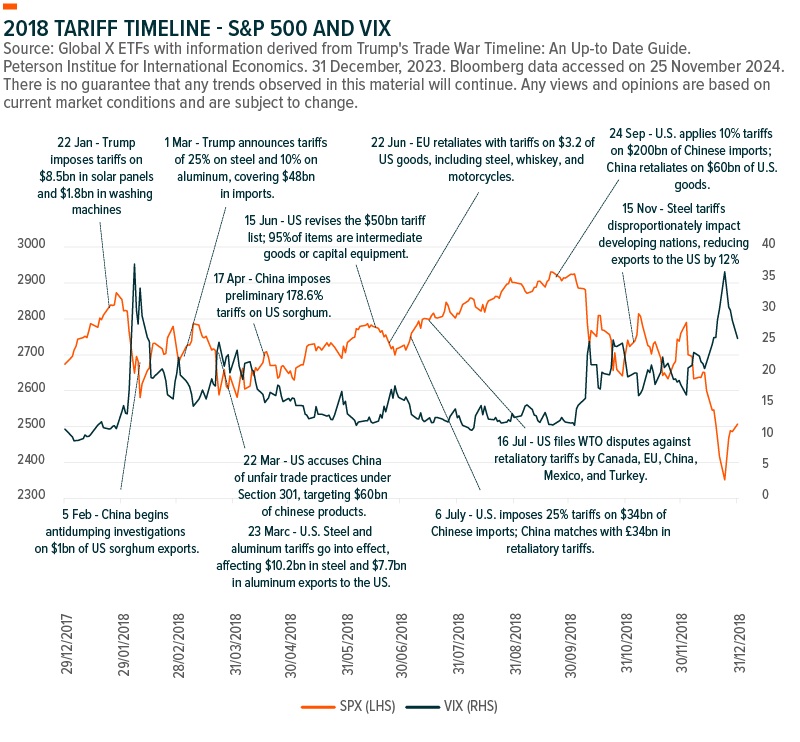

Proposed tariffs under the new U.S. administration could disrupt global supply chains, fuel inflation, and reintroduce market volatility reminiscent of the 2018 trade war.

Previous tariffs on solar panels, steel, and aluminium caused retaliatory measures and spiked the VIX to 37, underscoring the risks of protectionist policies.

With the new administration set to take office in January 2025, speculation is rising over renewed trade tensions in the U.S. Proposed policies include tariffs of 25% on all imports from Canada and Mexico, additional levies on Chinese goods, and potential blanket tariffs of up to 20% on all imports.15 These measures, aimed at reshaping trade relationships, could carry the risk of fuelling inflation and disrupting global supply chains, potentially reintroducing market volatility reminiscent of the turbulence experienced during the 2018 trade war.

Historically, trade policies targeting solar panels, steel and aluminium led to significant tariffs on Chinese imports, prompting retaliatory measures and subsequent spiking market volatility.16, 17 The CBOE Volatility Index (VIX), often called the “fear gauge”, surged to 37 at the height of those tensions.18 While these measures sought to address trade imbalances and support domestic industries, they served to highlight the delicate balance between protectionism and global economic stability.

Thematic Outlook (by Andrew Ye)

Key Takeaways:

U.S. manufacturing is experiencing growth, with semiconductor investments reaching $446 billion and construction surging 154% since the IIJA in 2021.

Government incentives and private investments appear to be driving reindustrialisation, reshoring critical supply chains, and creating potential opportunities for infrastructure developers.

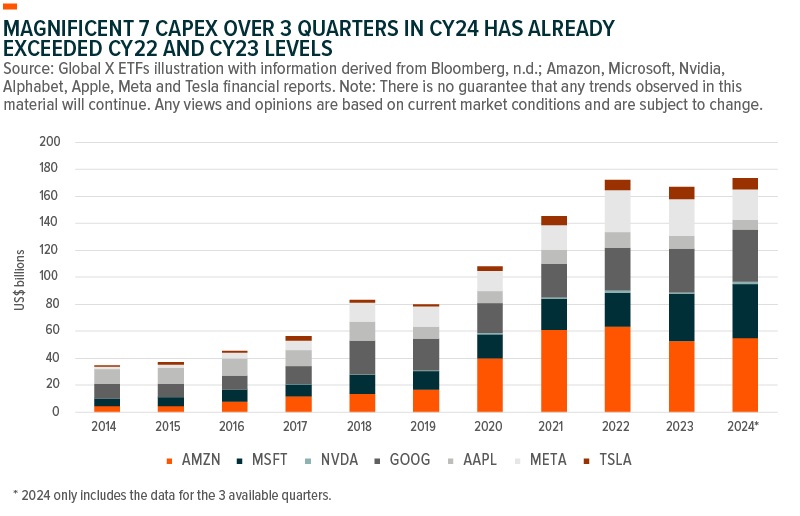

Major capital expenditure on AI by hyperscalers highlights transformative growth potential across the AI value chain, from hardware to software innovators.

The Reshoring Renaissance: A Catalyst for U.S. Manufacturing?

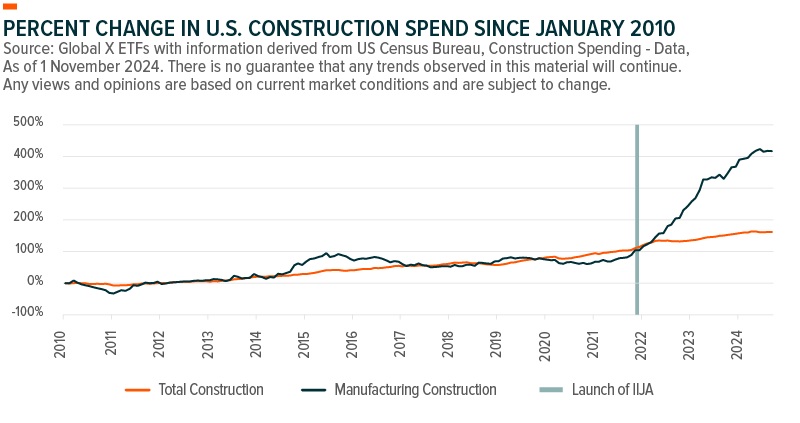

The reshoring of semiconductor manufacturing and broader reindustrialisation efforts could be key drivers of U.S. infrastructure growth. Private investment in semiconductors and electronics has already reached $446 billion as of November 2024,19 potentially fuelled by government incentives and a focus on addressing national security and supply chain concerns. This trend appears to be part of a broader surge in U.S. manufacturing construction, which has increased by 154% since the passage of the Infrastructure Investment and Jobs Act (IIJA) in November 2021, far outpacing the 24.3% growth in total construction.20 Over the longer term, manufacturing construction has increased 417.7%, since January 2010, reflecting sustained momentum.21 Looking ahead, policy focus to reindustrialise the U.S. and reshore critical supply chains could bolster manufacturing activity and unlock additional opportunities for infrastructure developers.22 These developments underscore the critical role of fiscal policies and private sector investment in driving transformative growth across U.S. industries.

“Reshoring and reindustrialisation are driving transformative growth in U.S. manufacturing, with semiconductor investment surpassing $446 billion and construction surging 154% since 2021”

Artificial Intelligence: The Capex Supercycle to continue into 2025?

The continued growth of Artificial Intelligence (AI) is driving major capital expenditure (‘capex’) among hyperscalers (large-scale data centre operators that offer cloud computing and data solutions to businesses that require significant digital infrastructure, processing, and storage), with companies prioritising AI investments to capitalise on its transformative potential.23 While some believe the theme is still in the early stages, AI adoption is already showcasing its ability to potentially reduce costs, and unlock revenue and growth opportunities.24

Investment in AI has predominantly focused on the build-out of the hardware layer, including chips, but the software layer is increasingly capturing value. Companies in industries such as customer relationship management (CRM) and creative industries are integrating generative AI functionality, potentially paving the way for enhanced productivity and customer engagement.25, 26 For investors, the opportunities may lie in targeting the full AI value chain, from the hardware manufacturers that may benefit from any surging demand to software innovators leading adoption across sectors.

2025 Metals Landscape: Supply Risks and Growth Catalysts (by Roberta Caselli)

Key Takeaways:

The uranium market appears set to potentially benefit from rising nuclear energy capacity, legislative support like the “Advance Act,” and supply chain shifts driven by geopolitical uncertainties.

Copper demand remains resilient due to its critical role in renewables and AI infrastructure, and supply constraints and concentrate shortages may lead to market deficits in 2025.

Precious metals may offer long-term appeal amid rising U.S. debt, inflation risks, and increased demand for silver in solar panels, supported by central bank accumulation and anticipated Fed rate cuts.

“With the U.S. pledging to triple nuclear power capacity by 2050 and AI-driven energy demand on the rise, uranium is cementing its role as a cornerstone of the global energy transition”

The uranium market appears to be potentially poised for growth in 2025, supported by increased nuclear energy capacity, supply concerns, and the push for energy independence.27, 28, 29 Outcomes from COP29 have reinforced commitments to expand nuclear energy, with the U.S. pledging to increase nuclear power capacity by 35 gigawatts over the next decade and a tripling by 2050.30, 31 Legislative support, including the bipartisan “Advance Act” (the Advanced Nuclear for Clean Energy), further accelerates the building of new reactors.32 Election risks may not hinder uranium’s momentum, and its growth could be further supported by increased energy consumption driven by the expansion of artificial intelligence.33 While geopolitical uncertainties, like restricted uranium exports from Russia, present supply risks, this could strengthen demand for Western uranium enrichment and conversion capacity, ensuring uranium remains a vital component of the global energy transition.34

Copper markets in 2025 could experience heightened volatility, largely driven by supply constraints and the ongoing demand from the energy transition and AI data centre infrastructure.35 Despite the threat of trade tariffs,36 the red metal’s essential role in renewables and AI-related technologies underpins its resilience.37 Acute concentrate shortages are anticipated to decrease refined capacity utilisation to 70% from 75%, leading to a possible deficit in the refined copper market.38 On the demand side, China’s policy support could play a critical role in stabilising the market, depending on the level and timing of its stimulus.39

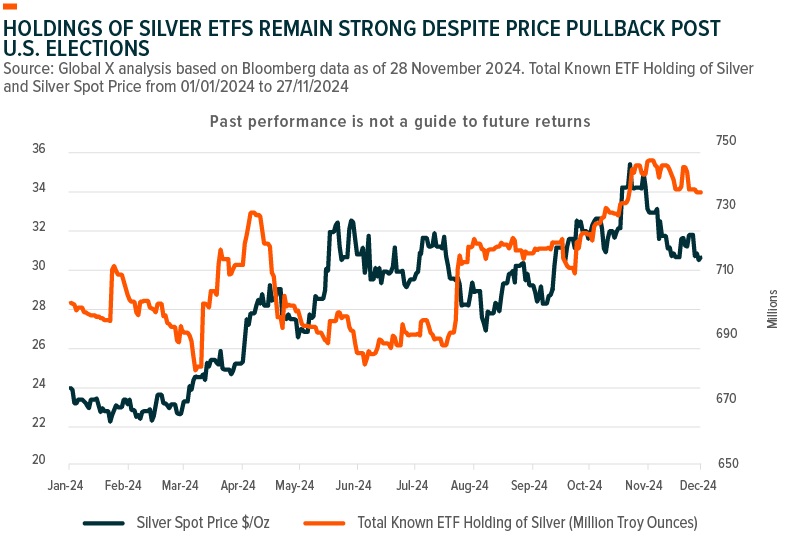

Despite the excellent performance so far in 2024, the strong dollar and higher U.S. yields caused gold and silver to react negatively following the U.S. election.40 Gold and silver are continuing to offer long-term appeal in 2025, bolstered by several factors, such as rising U.S. debt, inflation risks, and global uncertainty.41 Anticipated Federal Reserve rate cuts could lower the opportunity cost of holding these metals,42 while central banks may decrease their exposure to the U.S. dollar and maintain their accumulation of gold as a hedge against geopolitical risks.43 On the fundamental side, silver’s use in solar panels is projected to grow, potentially contributing to another market deficit.44 Despite, recent price volatility, exchange-traded funds holdings of silver have remained resilient, potentially signalling a bullish outlook for the year ahead.45

This document is not intended to be, or does not constitute, investment research

Footnotes

- Financial Times (25/11/2024), US and Europe diverge on monetary policy as Trump scrambles outlook

- Reuters (20/11/2024) Fed to lower rates in Dec but slow pace in 2025 on inflation risks: Reuters poll

- European Central Bank (17/10/2024), Monetary policy decisions

- Euronews (11/12/2024) ECB set to trim interest rates again: What’s next and why it matters

- Deloitte (4/11/2024) 2025 Engineering and Construction Industry Outlook

- Construction Dive (12/09/2024) $720B in IIJA funds yet to be allocated

- Tom’s Hardware (07/09/2024) Chipmakers race to get CHIPS Act dollars before White House changeover — TSMC and GlobalFoundries finalize applications, facilitating payouts

- Fox Business News (13/08/2023) US manufacturing sector reaping benefits of reshoring

- European Commission (23/02/2024) NextGenerationEU

- European Commission (02/12/2024) Available budget of Cohesion Policy 2021-2027

- Reuters (14/02/2024) Germany hits 2% NATO spending target for first time since end of Cold War

- Market Watch (25/11/2024) Defense IT Spending Market to Grow by USD 23.53 Billion (2024-2028), Driven by Autonomous Systems Development, Market Evolution Powered by AI – Technavio

- Fastmarkets (7/11/2024) Inflation Reduction Act in focus in Trump presidency

- Invesco (07/10/2024) Why European equities are attractively valued

- Financial Times (26/11/2024) Donald Trump says he will hit China, Canada and Mexico with new tariffs

- Ibid.

- Guide Peterson Institute for International Economics (31/12/2023) Trump’s Trade War Timeline: An Up-to Date

- Global X ETFs with information derived from Bloomberg Terminal. VIX Price data. Accessed on 25 November 2024.

- US Census Bureau (accessed 26/11/2024) Construction Spending – Data

- Ibid.

- Bain & Company (13/12/2024) Businesses accelerate reshoring and near-shoring amid heightened geopolitical uncertainties and rising costs, Bain & Company finds

- Microsoft, Amazon and Alphabet Earnings Call Transcripts, n.d..

- McKinsey (05/2024) The state of AI in early 2024: Gen AI adoption spikes and starts to generate value

- Salesforce (07/03/2023) Salesforce Announces Einstein GPT, the World’s First Generative AI for CRM

- Salesforce Earnings Call Transcript, Q2 2025.

- International Atomic Energy Agency (18/11/2024) Nuclear Power in the COP29 Spotlight as Countries and Companies Eye Climate Solutions

- World Nuclear News (18/11/2024) Russia places ‘tit-for-tat’ ban on US uranium exports

- EIA (1/10/2024) Data center owners turn to nuclear as potential electricity source

- International Atomic Energy Agency (18/11/2024) Nuclear Power in the COP29 Spotlight as Countries and Companies Eye Climate Solutions

- Ibid.

- US Senate Committee on Environment & Public Works (9/07/2024) SIGNED: Bipartisan ADVANCE Act to Boost Nuclear Energy Now Law

- Ibid.

- Ibid.

- Morningstar (15/11/2024) Is Copper Entering a New Supercycle?

- Reuters (28/11/2024) China’s scrap copper imports set to slump over US trade worries, analysts say

- Ibid.

- Bloomberg (14/11/2024) Global Copper Smelters to Cut Runs to 70% on Short Supply: CRU

- Ibid.

- Bloomberg data as of 28/11/2024. Gold and Silver Spot price from 01/01/2024 to 27/11/2024.

- Reuters (6/11/2024) US fiscal strain looms as key challenge for newly elected Trump

- Reuters (20/11/2024) Fed to lower rates in Dec but slow pace in 2025 on inflation risks: Reuters poll

- Bloomberg UK (15/10/2024) Central Bankers Make Rare Comments in Favor of Bigger Gold Stash

- The Silver Institute (17/04/2024). World Silver Survey 2024.

- Ibid.

- Bloomberg (22/11/2024) Silver’s Solid ETFs Suggest Prices Can Stage a Fightback

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Global X ETFs Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or Global X ETFs Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account