14 January 2026 – Cyclical sectors regain leadership: Financials and Industrials drive momentum

Cyclical sectors are reclaiming leadership as the economic growth outlook strengthens on the back of monetary and fiscal support. Industrials, Financials, and Energy have led performance since late 4Q25—a broad advance in cyclical sectors.1

After months of underperformance in 2025, Energy had a bullish technical breakout on the first trading day following the US capture of Venezuelan President Nicolás Maduro on January 3. More importantly, other cyclical sectors, such as Financials and Industrials, have also shown notable upside price movement to start the year.2 These positive developments within Financials and Industrials are built on the sectors’ strong performance in December, with both outperforming the broad market for the month.3

Recent performance strength in Financials and Industrials has led to a reversal of their underperformance in 3Q25 relative to the S&P 500.4 Positive developments at the industry level are key to advances in Financials and Industrials.

Financials: Monetary easing and deregulation provide tailwinds

Within Financials, bank and capital market industries were important contributors to the sector’s bullish breakout in December and the ongoing positive outlook for 2026. Federal Reserve (Fed) interest rate cuts—both the lagging effect of the cumulative 75 basis points of rate cuts since last September and the additional two cuts expected by the market for this year—could boost business lending and capital markets activity. And the resulting steeper yield curve may lead to improving profitability in Financials more broadly.

Past performance is not indicative of future results

In terms of deregulation, banking regulators and supervisors issued several final or proposed regulatory changes that have led to lower capital requirements and supervisory standards, including modifications to the enhanced supplementary leverage ratio (eSLR) and stress test models. Additionally, a capital neutral Basell III Endgame and lower additional capital requirements for Global Systemically Important Banks may further improve banks’ capital efficiency, lower the cost of capital, and boost return on equity.

Moreover, supported by an improved antitrust and macroeconomic backdrop, M&A and IPO activity within the sector may continue to accelerate beyond its current below average cyclical activity level, likely leading to strong investment banking revenue growth.5

Regulatory progress on digital asset market structure and asset tokenization also are likely to stimulate innovation in capital markets and drive new opportunities.

Industrials: Powered by defense spending and infrastructure investment

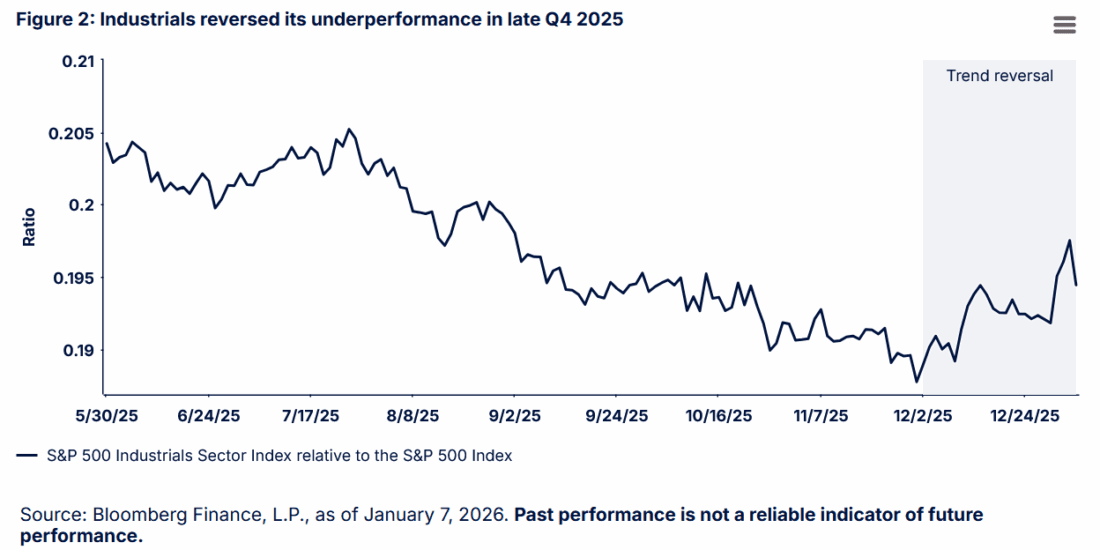

Industrials reversed its underperformance trend in late Q4 (Figure 2), aided by improved performance in the aerospace & defense industry. As the global geopolitical landscape remains volatile from Venezuela and Ukraine to the South China Sea, the industry has been benefiting from both higher global defense spending and rising power demand and competition.

The US alone has allocated $1.16 trillion to national defense expenditures and gross investment, an all-time high, and the geopolitical environment likely points to that figure steadily rising.6 Analysts project industry earnings will rise 51% in 2026, following an 81.5% increase in 3Q25 and an anticipated 144% surge in 4Q25.7

Past performance is not indicative of future results

In addition to defense spending, the machinery and electrical equipment industries, which represent more than 47% of the Industrial sector, stand to benefit from increasing demand and investment in power infrastructure—a crucial component in the current AI capital expenditure cycle. Analysts are projecting machinery earnings to grow by 10.5% in 2026, while electrical equipment is slated to grow by 20%.8

Energy: Short-term catalysts, medium-term constraints

Following the US capture of Maduro, the Energy sector experienced a positive technical breakout from a multi-month triangle pattern (Figure 3). This resulted in the S&P 500 Energy Index reaching its highest intraday price since November 2024.9

Past performance is not indicative of future results

Yet, given the dynamic nature of the political situation, price action is likely to remain volatile as evidenced in the sector’s heightened implied volatility.10 Near-term catalysts for Energy are now in motion as major oil producers and refiners as well as energy equipment and service providers may benefit from expectations of improved operating ability and asset recovery in Venezuela.

But the sector’s medium-term outlook remains constrained as the global oil oversupply story persists and the prospect for higher long-term Venezuelan oil production limits the potential upside of any oil rebound when demand begins to recover. This dynamic is reflected in the contango shape of the oil futures curve for this year.11

Although Venezuela holds the world’s largest proven oil reserves, years of underinvestment and deterioration across its production and transportation infrastructure mean that substantial capital and technical support will be required to restore output to meaningful levels. Any increase in supply over time is likely to introduce downward pressure on oil prices and the sector’s earnings.

Cyclicals outlook: Where to focus in 2026

Amid uncertainty in Venezuela, one investment implication is clear: an emerging opportunity in cyclical sectors is underway. The strong yet volatile breakout in Energy has brought more attention to the emerging leadership across cyclical sectors, but Financials and Industrials are particularly well-positioned to advance further on the back of strong earnings outlooks, easing monetary policy, and expansive fiscal stimulus.

Disclosure: State Street Global Advisors

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account