Originally Posted 24 November 2025 – Capex, capacity, compute: What Q3 signals for AI

Key Takeaways

- Advanced-chips supply remains tight, while memory and interconnect constraints persist and power and cooling often dictate deployment timing.

- Capital expenditure guides are higher into 2026, with cloud growth and backlogs supporting ongoing demand for compute.

- Compute capacity is being pre-secured through multi-year contracts with neocloud providers, and revenue timing mainly reflects facility readiness.

- Early software monetisation is visible, and a rising share of large companies report measurable AI-related benefits.

The latest earnings from companies exposed to artificial intelligence (AI) show continued strength across the supply chain. Demand for advanced manufacturing, memory and connectivity remains robust, while hyperscalers have reaffirmed higher capital spending plans and customers are still securing compute capacity ahead of need. Cloud revenues remain resilient, and several software firms are beginning to see early benefits from AI deployment. Together, these trends offer a solid foundation for assessing the next phase of AI investment and adoption.

Upstream signals: still tight, and getting tighter

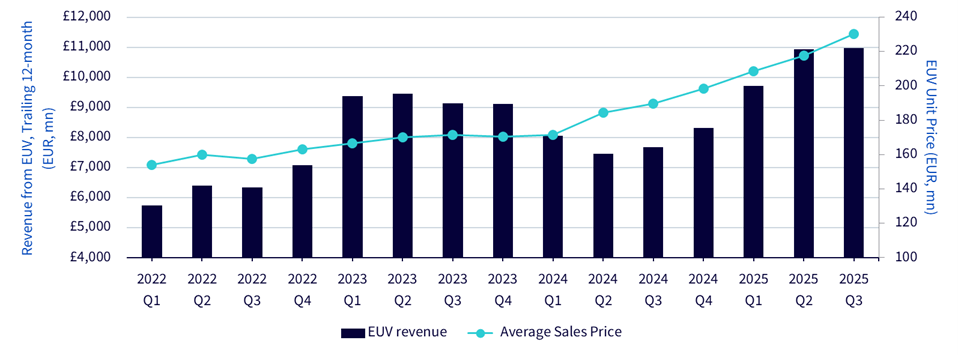

At the top of the AI supply chain, ASML remains the only company in the world that makes extreme ultraviolet (EUV) scanners, the machines used to produce the most advanced computer chips. In its third-quarter update, the company reported steady demand for both EUV and deep ultraviolet (DUV) systems, driven by the ongoing growth of AI-related technology. Orders and future demand were further supported by the rollout of ASML’s next generation of tools. Strong interest in EUV systems has also pushed prices up by around 21% over the past year.

Figure 1: ASML – trailing 12-month revenue from EUV & average EUV unit price

Source: ASML’s filings and earnings call transcripts, as of 10 November 2025. Past performance is not indicative of future results and any investments may go down in value.

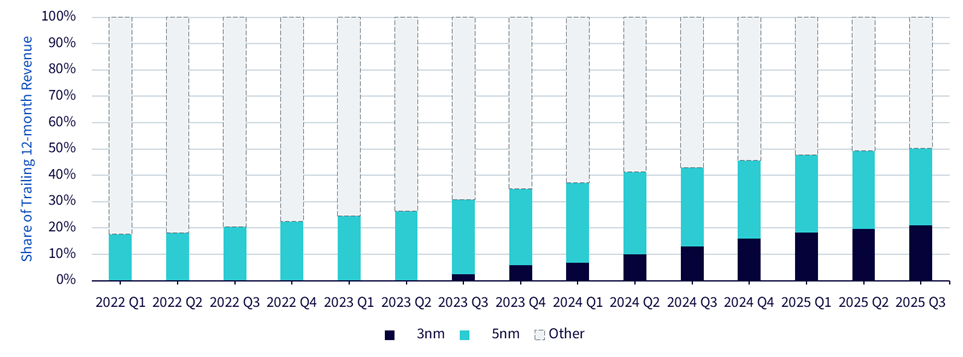

At the chip manufacturing stage, TSMC (Taiwan Semiconductor Manufacturing Company) remains the clear industry leader and a good indicator of overall AI-related demand. In its third-quarter results, the company reported that 3-nanometre (nm) chips, its most advanced and efficient semiconductors, made up a record 22.4% of total revenue. When combined with 5 nm chips, these cutting-edge products now account for about half of TSMC’s revenue, up from less than 20% previously. This shift highlights the surge in demand for advanced chips used to power AI technologies.

Figure 2: TSCM – share of revenue generated by 3nm and 5nm chips, trailing 12 months

Source: TSMC’s filings and earnings call transcripts, as of 10 November 2025. Past performance is not indicative of future results and any investments may go down in value.

Beyond graphics processing units (GPUs), the tightest supply constraints today are in memory and connectivity, with power and heat limits becoming increasingly significant. Shortages of memory chips, including dynamic random-access memory (DRAM), high-bandwidth memory (HBM), double data rate (DDR) and NAND flash, reflect the rapid build-out of AI infrastructure. A clear sign of this is the sharp rise in DRAM spot prices in recent months. As Samsung’s management noted in their latest earnings call: “It is expected that customers’ demand for next year will exceed our supply, even considering our investment and capacity expansion plan.”

These supply shortages were also evident in the latest results from Samsung and SK hynix. SK hynix reported record profits driven by booming orders for AI-focused memory (HBM) and expects more than 30% annual growth in demand for AI memory over the next five years. Samsung’s memory business also delivered record revenue, up around 20% year on year. Connectivity demand is rising in parallel. Astera Labs, a company specialising in high-speed data connections, reported third-quarter revenue of about US $231 million, up roughly 104% year on year. Overall, the ongoing expansion of AI infrastructure is benefiting the wider semiconductor sector, from memory and connectivity through to GPUs.

Buyers’ chequebooks: hyperscaler capex still rising

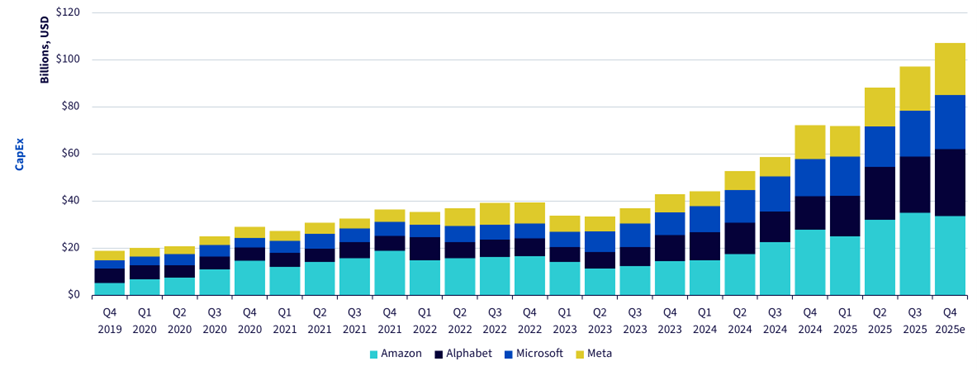

Hyperscalers continued to push capital expenditures (capex) higher in Q3 and pointed to another leg up in 2026. The combined capex of Alphabet, Amazon, Microsoft and Meta increased by roughly 65% year on year to an all-time high. Meanwhile, the three major cloud service providers among them: Alphabet, Amazon and Microsoft, reported strong cloud growth, which in turn is driving demand for AI infrastructure.

Figure 3: Hyperscalers’ capex over the last 5 years

Source: WisdomTree, Bloomberg. As of 10 November 2025. Figures for Q4 2025 are averages of analysts’ estimates available on Bloomberg. Past performance is not indicative of future results and any investments may go down in value.

Alphabet raised its 2025 capex outlook again to US $91–93 billion and disclosed Google Cloud revenue growth of 34%, with backlog up to US $155 billion, a strong forward indicator of demand for compute and AI services. Meta guided to US $70–72 billion, with 2026 set to step up as training capacity scales. Microsoft’s Azure revenue grew 40%, and management indicated capex will step up again, with the CFO flagging more than $30 billion of spend in the current quarter to support AI infrastructure. Amazon’s AWS (Amazon Web Services) grew 20% year on year in Q3, its best pace since 2022, and the company highlighted a sharp increase in property and equipment purchases that depressed free cash flow, another clear sign that physical capacity is being added.

Compute is being pre-booked: the rise of neocloud

Compute demand is rising faster than self-build capacity, so large buyers are pre-securing supply from neocloud operators. The gating factor is often facility readiness rather than chips, with deployment timing tied to powered-shell availability.

CoreWeave illustrates this dynamic. Q3 revenue reached about US $1.36 billion and its contracted backlog rose to US $55.6 billion1, but guidance was trimmed after a third-party data-centre partner delayed a powered shell. Management emphasised that this was a timing issue and that customers extended contract windows, so demand and deal value remained intact.

Nebius reported a similar pattern of strong demand, with third-quarter sales rising 355% to US $146 million and capacity fully sold for the period2. The company also announced new multi-year contracts with large cloud customers, giving it better visibility on future revenue. Taken together, these developments suggest that customers are increasingly turning to neocloud providers to secure computing power in advance. The short-term changes in revenue mainly reflect how quickly new data-centre sites can come online, rather than a slowdown in demand.

Signs of software monetisation is becoming visible

The application cycle is still in its early stages, but earnings are showing more tangible signs. Palantir’s Q3 reported continued growth in commercial revenue alongside brisk adoption of its AI platform, and management emphasised deal velocity for AI-driven use cases. Akamai pointed to progress with its AI Inference Cloud and noted AI-related workloads as a contributor. These are small next to hyperscaler numbers, yet they mark a shift from pilots to production.

A broader look across large-cap companies shows the momentum building. In recent research from Morgan Stanley3, 28% of S&P 500 companies discussed a measurable AI cost or revenue impact this quarter; across the full index, 15% cited at least one measurable benefit, up from 14% in Q2 and 11% a year ago. This steady rise suggests that AI-driven revenue effects are beginning to extend beyond semiconductors and cloud computing.

Conclusion

Q3 points to an investment cycle that is broadening from wafers to workloads. Supply remains tight where it matters most, particularly in memory and connectivity, with power and cooling often dictating deployment pace. Buyers are still increasing capital plans and are pre-securing compute through neocloud contracts, which extend visibility beyond the next couple of quarters. Financial impact from AI application is now showing up in reported numbers, albeit from a small base.

Bubble concerns deserve context. Past manias left long-lived assets such as railway networks and fibre backbones. Today’s AI build involves faster-depreciating chips, but it is also creating durable capacity in data centre infrastructure and network fabrics, and it is generating revenue and backlog now rather than hypothetical demand later. Sector valuations remain below the most extreme levels seen in 2000, Nvidia’s forward price-to-earnings multiple is elevated but sits in the high-20s on recent readings, whereas Cisco peaked above 100x at the top of the 2000 cycle. This is not a prediction about future returns, but it does indicate a more moderate starting point than the extreme valuations seen during the dot-com era.

1Source: CoreWeave, third quarter 2025 results, 10 November 2025.

2Source: Nebius, third quarter 2025 financial results, 11 November 2025.

3Source: “Momentum Around AI Adoption Is Building”, Morgan Stanley, 06/11/2025.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account