It is customary, and not incorrect, to divide the investment universe into a low-risk, high-risk paradigm, with volatility being a reasonable proxy for risk. It should surprise no one that on that basis, stocks tend to be more volatile and thus considered more risky than short-term fixed income. Yet this month, we have seen even safer assets become more volatile. As we have asked before, “If a relatively low-risk asset like 2-year notes is getting clobbered, what chance do risky assets have?”

We have seen 2-Year Treasury yields rise substantially since hostilities in the Persian Gulf began on February 28th. The one-month high-low range exceeds 50-basis points thanks to a nearly complete reassessment of the likelihood for interest rate cuts in the coming year. If the market removes two 25-bp cuts from its near-term calculus, it should come as no surprise that 2-year rates will reflect that change.

2-Year Treasury Yields, 4-Months, Daily Candles, with 30-day Moving Average (green line)

Source: Bloomberg, past performance is not indicative of future returns.

After a move of that magnitude, it should also not be surprising to see the implied and historical volatilities of options on 2-year note futures (ZT) rise accordingly. Implied volatility has more than doubled, 10-day historical has roughly tripled, and 30-day historical is up by about 50%.

4-Months, Implied (white), 10-day historical (yellow), 30-day historical (orange) Volatilities on June ZT Futures Options

Source: Interactive Brokers, past performance is not indicative of future returns.

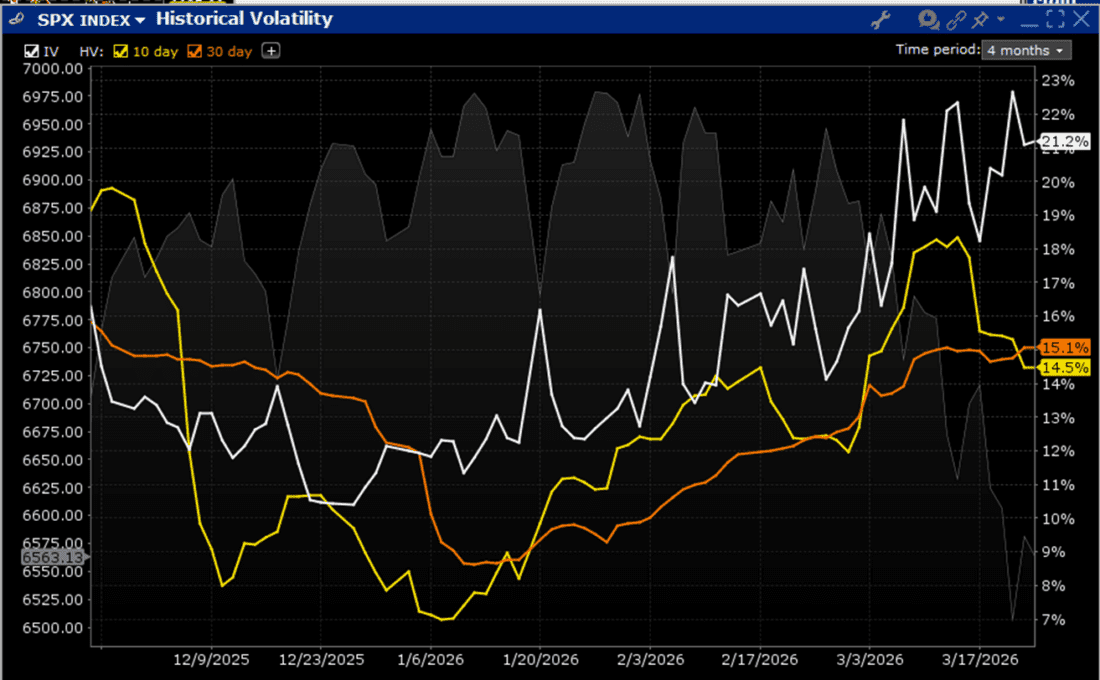

Stock traders will undoubtedly find the absolute levels of volatility in the prior example to be laughably low, since they are roughly 1/10 those of the S&P 500 (SPX). But the relative moves, the respective jumps in volatility, are far greater in the less volatile product.

4-Months, Implied (white), 10-day historical (yellow), 30-day historical (orange) Volatilities on SPX

Source: Interactive Brokers, past performance is not indicative of future returns.

This matters for an important reason. When we first laid out our thesis for why equity traders needed to become concerned when low-risk assets become risky, we explained it this way:

…it is important to remember that risk-free rates are utilized in nearly every asset pricing model. If you think of current stock prices as the present value of a company’s future cash flows – which I do – then those future values are diminished. Investors are being forced to reevaluate their holdings. That is a difficult process under any circumstances, and incredibly so when a drastic reevaluation must occur in a very short period of time.

If a key pillar supporting equity valuations becomes wobbly, it becomes quite difficult to expect those valuations to remain stable.

Interestingly, the quoted paragraph was written in June 2022. At the time, stocks were plunging because, among other things, the Fed was raising rates to combat the nasty bout of post-Covid inflation. It is easy to forget that while inflation is unpleasant, so is the medication required to purge it from the system. Rising yields throughout the curve reflect concerns that supply shocks, not only in crude oil, but in liquefied natural gas, fertilizers, and even helium, could become pervasive and create price pressures in unexpected corners of the economy.

This is why a quick end to the hostilities is critical. The longer the Strait of Hormuz remains closed, the longer that the prices of these key commodities remain elevated and the greater that they put sand in the gears of the global economy. While it is unrealistic to think that these prices return immediately to pre-war levels, it is sensible to consider the effects of a short-term disruption as largely “transitory”, to borrow a dirty word from the Federal Reserve. The longer the conflict, however, the less transitory and more embedded the effects become. Thus, without some real clarity, one should continue to expect volatility from both safer and riskier assets.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Options (with multiple legs)

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account