Originally posted, 16 June 2025 – What’s Hot: US-China Trade Talks Highlight Strategic Value of Rare Earths

Key Takeaways

- China’s dominant share of rare earth output and reserves enables it to wield export controls as a geopolitical instrument.

- Developing viable alternative supply chains requires overcoming significant investment, regulatory and environmental challenges.

- Potential US support under the Defence Production Act could accelerate domestic rare earth mining and processing capacity.

- The positive market momentum of non-Chinese rare earth miners underscores growing investor confidence in the sector.

The recent US-China trade talks held in London in June 2025 have once again thrust rare earth elements (REEs) into the spotlight. As negotiations concluded, China agreed to ease its export restrictions on rare earth metals, demonstrating clearly how Beijing uses these essential commodities strategically—much like the US employs tech export controls—to advance geopolitical interests. This strategic move highlights an increasingly clear truth: rare earths have become potent geopolitical tools.

Why Rare Earths Can Be Weaponised

Rare earth elements are crucial to the functioning of high-tech industries and defence sectors globally. They are fundamental components of advanced technologies, from radar systems used in defence and aviation, to precision-guided munitions, and even essential elements in semiconductor manufacturing.

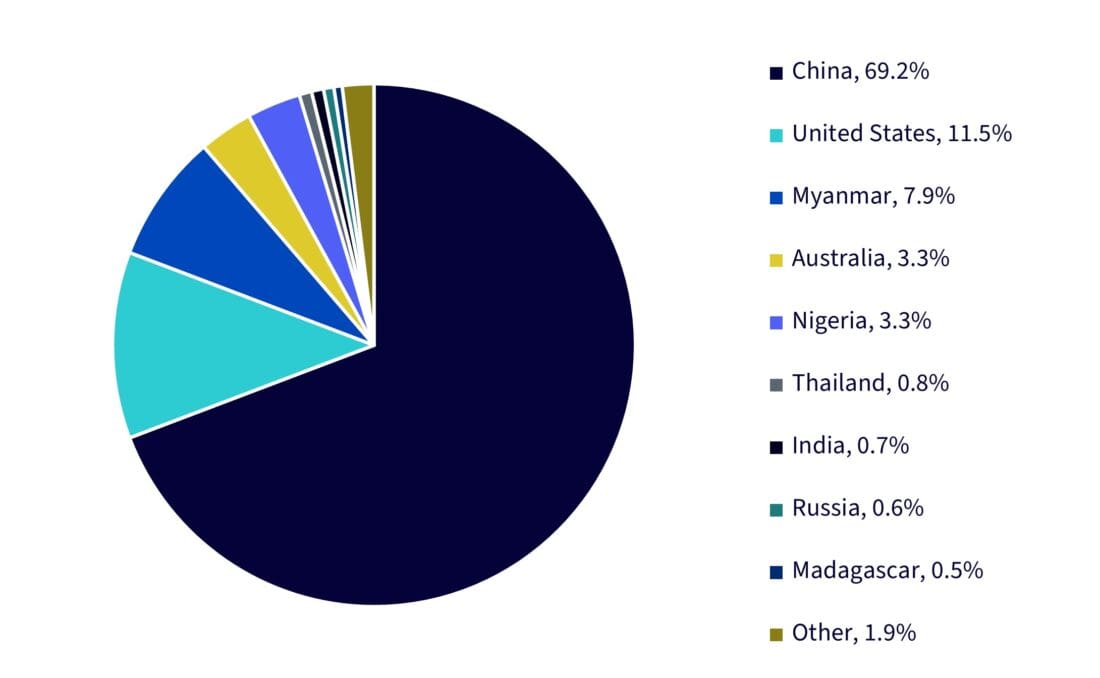

China’s overwhelming dominance in rare earth production provides it with a unique geopolitical lever. Accounting for nearly 70% of global rare earth output, according to the latest US Geological Survey (USGS) figures, and holding approximately half of the world’s known reserves, China’s position grants significant influence over global supply chains. The ease with which Beijing can adjust export quotas or enforce export bans means rare earths are easily weaponised to counterbalance geopolitical pressure from Washington.

Figure 1: Rare Earths Mine Production (2024)

Source: United States Geological Survey.

In recent years, China has strategically utilised rare earth exports as leverage during geopolitical tensions, notably during trade disputes. This control not only provides direct economic advantages but also significant indirect geopolitical influence, placing pressure on high-tech industries in competitor nations reliant on these materials. Such dependence exposes vulnerabilities, making it difficult for nations like the US and its allies to effectively challenge China’s manoeuvres without risking substantial economic disruption.

Can the US Find Alternatives?

The US is increasingly aware of the vulnerability inherent in relying heavily on Chinese rare earth supplies. Efforts to develop domestic or allied alternative supply chains are gaining momentum but are fraught with complexity. MP Materials Corp’s Mountain Pass mine in California and Lynas Rare Earths Ltd’s operations in Australia and Malaysia represent notable non-Chinese producers. Yet, despite their promising production capacities, these firms face significant hurdles.

Firstly, rare earth extraction and processing require significant capital investment and advanced technology. Building and scaling these facilities swiftly enough to reduce reliance on China poses substantial financial and supply chain challenges. Additionally, environmental concerns and stringent regulations in Western countries can slow project approvals, further complicating the rapid scaling of alternative production facilities.

Opportunities on the Horizon

Nevertheless, recent developments hint at significant opportunities in the rare earth sector, driven by both governmental backing and favourable market sentiment.

The Trump administration is currently considering invoking the Defence Production Act—historically a Cold War-era tool—to provide robust financial backing, loan guarantees, and direct investments for rare earth projects across mining, processing, and downstream technologies. While the precise details and timelines remain uncertain, the move signals potentially substantial government investment to bolster America’s strategic autonomy.

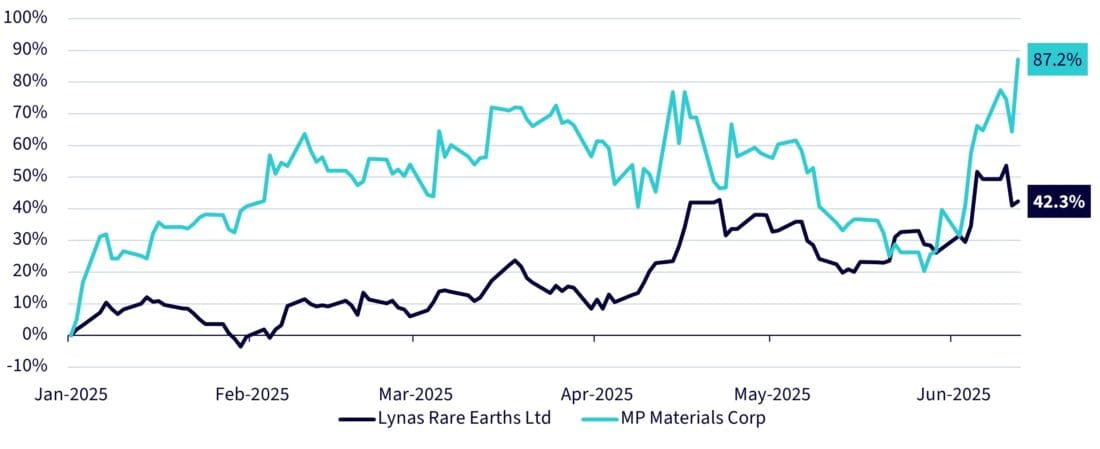

From a market perspective, investor sentiment toward companies positioned in the rare earths supply chain has been exceptionally positive in 2025. Shares of Lynas Rare Earths and MP Materials have soared significantly year-to-date, reflecting investor optimism and anticipation of further strategic moves and investments by the US government.

Furthermore, the broader strategic metals sector—encompassing not only rare earths but also lithium, cobalt, and other critical minerals—presents additional growth opportunities. With electric vehicle production accelerating and advanced technological manufacturing expanding, demand for these essential elements is expected to remain robust.

Figure 2: YTD Performance: Lynas Rare Earths Ltd. and MP Materials Corp.

Source: WisdomTree, Bloomberg. As of 12 June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

The geopolitical tensions underscored by recent US-China trade talks provide a compelling narrative for the growing strategic importance of rare earth elements. China’s dominance in global rare earth production highlights both the risks of reliance and the imperative for the US and its allies to build alternative supply chains.

For investors, rare earth mining and processing sectors appear increasingly attractive, supported by strong government signals of substantial financial backing and buoyant market sentiment. While challenges in environmental management, regulatory approval, and capital intensity remain, the opportunities for significant returns in this strategic sector appear tangible. Thus, the rare earths and broader strategic metals sectors merit close attention from investors looking to navigate the geopolitical complexities shaping today’s global markets.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account