Equity markets sometimes have a way of burying the lead. Today’s release of major bank earnings marked the unofficial start to earnings season. We also received important reads on the economy with a better-than-expected PPI report and an atrocious set of sentiment readings from the University of Michigan. More significantly, bond yields are soaring and the dollar is plunging. Yet as I type this, major US equity indices are essentially unchanged.

Long-time readers know that I wish the banks didn’t lead off the earnings parade. Their reliance upon interest rates and the yield curve, and in some cases, trading results, makes them too idiosyncratic to be a reliable harbinger of the results to follow. We heard from JPMorgan (JPM), Wells Fargo (WFC), Bank of New York Mellon (BK), and other key financial stocks like Blackrock (BK) and Morgan Stanley (MS). The results are mixed, with JPM and BLK rising, and WFC, MS and BK falling. None are having particularly noteworthy moves.

Yet I have always noted that there is indeed something to be learned from the conference calls that accompany banks’ earnings. Their managements can offer insights into trends in their customers’ credit quality and loan demand. The key headlines today came from JPM’s CEO, as they often do. In his prepared remarks, Jamie Dimon said:

The economy is facing considerable turbulence (including geopolitics), with the potential positives of tax reform and deregulation and the potential negatives of tariffs and ‘trade wars,’ ongoing sticky inflation, high fiscal deficits and still rather high asset prices and volatility.

Seems obvious, no? Anyone paying attention to markets in the past few weeks would come to a similar conclusion. But business media focused on the word “turbulence”. And something about that word resonated with me.

I’ve been asked why the Cboe Volatility Index (VIX) is remaining so firm even on a day when stocks are meandering in a relatively narrow range. Dimon’s verbiage reminded me of how I described VIX in a podcast from August 2023 and again in an article from July 2024:

VIX is the price of parachutes when a plane hits turbulence.

We explained:

This comes from my experience as a market maker. Nobody really wants umbrellas when it’s when there’s a drought, nobody really thinks about a parachute if the plane is moving along smoothly at 30,000 feet, but as soon as you hit some turbulence, or as soon as the rain clouds develop, people want them, and they want them in a hurry. And to me, VIX is still the most efficient way for an institutional manager to hedge his or her risks.

There is certainly no shortage of risks to hedge against right now. Movements in US Treasuries and the dollar are telling us that international investors are concerned. At one point this morning we saw 10-year yields rise by as much as 16 basis points and the Euro rise by about 2 cents versus the dollar. Those trends abated at about 11am EDT, implying that European investors were actively selling US fixed income and stopped when it was time to go home for the weekend. The chart below shows how the selling in the USD abated, but amidst a few days of major losses against major currencies that could serve as alternative safe havens for global investors:

3-Days, EUR/USD (red/green 5-minute candles, right scale), CHF/USD (blue), USD/JPY (purple, left scale)

Source: Interactive Brokers

Past performance is not indicative of future results

One could certainly assert that the weaker USD should be a boon for US equities. The leading US companies are multinationals, with revenues in a wide range of currencies. A weaker dollar means that those foreign revenues are worth more when translated into USD.

Even though the worst of the week’s volatility in stocks and bonds appears to be behind us, at least for now, some might be wondering why VIX remains around the elevated level of 40. As noted above, that is partly because investors continue to be concerned about turbulence, but it is also mathematical. For starters, thanks to the “rule of 16”, we can assert that a 40 VIX roughly implies that the market expects that intraday moves could average 2.5% over the coming 30 days. That doesn’t seem truly implausible, especially when we consider that recent events play a disproportionate role in traders’ volatility assumptions.

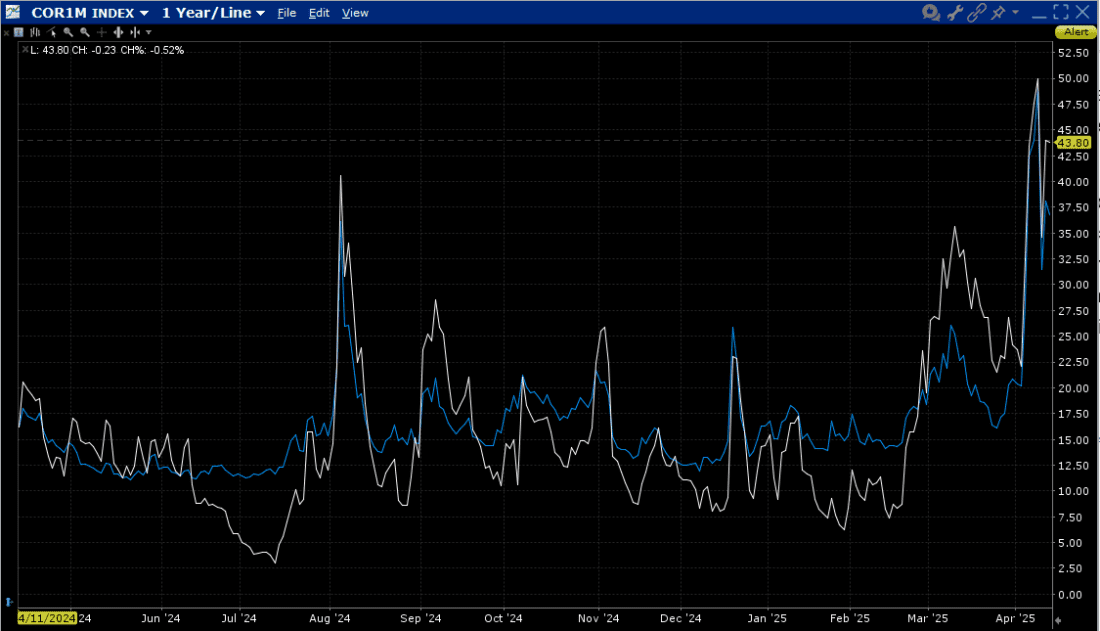

And a second mathematical rationale exists for an elevated VIX – market correlations remain extraordinarily elevated, and index volatility is heavily influenced by whether the index’ components are moving in synch or not. (More about that here.) Correlations tend to zoom when markets are extremely nervous, and as measured by the Cboe’s COR1M index they have been zooming recently. That has a strong influence on the level of VIX:

1-Year COR1M (white), VIX (blue)

Source: Interactive Brokers

Past performance is not indicative of future results

And once again, markets have changed dramatically in the time it took me to type this. We now see indices up more that 1%, most likely because US traders, ever eager to buy dips and chase rallies, perceived that those dour Europeans are done for the day. As we reminded yesterday, volatility – and turbulence — moves in both directions.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account