Socially acceptable volatility is rearing its head again today. The proximate cause of today’s rallies in stocks and bonds was a better-than-expected month-over-month Core CPI reading, but the magnitude of the rallies reflected the jittery sentiment that had pervaded markets – particularly in the fixed income arena. Extremes in sentiment lead to outsized moves.

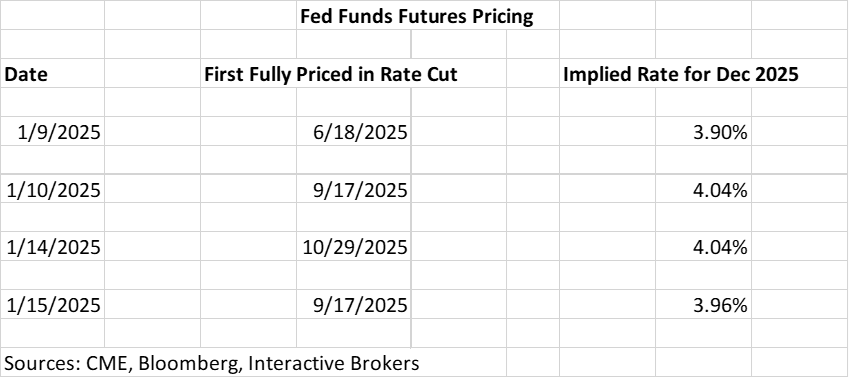

Seeing a 0.2% rise in December’s Core CPI was unequivocally a positive development. Decelerating inflation is always welcome, particularly after Friday’s jobs data inspired traders to temper their expectations for rate cuts in the coming year. Today’s report hasn’t caused traders to fully restore their rate cut expectations to the levels that prevailed last Thursday, but they have improved since yesterday:

The swings in the implied rates for December 2025 roughly correspond with the moves in 2-year and 10-year Treasuries that we have seen over that period. For example, 2-year rates are 9 basis points lower and 10-year rates are 13bp lower so far today. Throw in a bit of a relief rally into the more volatile long end of the yield curve and we can see that positive sentiment about the Fed is once again driving a wide range of asset prices.

But we should also take note of the fact that volatility is having a bit of a resurgence lately. Today is the 18th trading day since (including) the December 18th FOMC meeting. Assuming we hold onto at least most of the current gains, this would be the 9th day when the S&P 500 (SPX) closes with a move of greater than +/- 1%. You wouldn’t know that from seeing the Cboe Volatility Index (VIX) plunge to a 16 handle today, but the rally certainly quelled some demand for hedging protection.

The current period of greater than average volatility is not a particularly ominous sign, though the only period that featured a concentrated set of moves of this magnitude was late July – early August, when the yen carry trade imploded. After a brief period of jitters, markets quickly recovered, certainly buoyed by the recognition that the Fed was poised to cut rates – which they did just a few weeks later.

That said, when I was discussing the recent bout of volatility with a friend this morning, a quote came to mind:

Short term volatility is greatest at turning points and diminishes as a trend becomes established.

Regardless of your personal opinions about his politics, George Soros is one of history’s most successful investors and traders. Thus his insights about investing are worthwhile. As noted above, it is far too early to consider this an ominous sign about a potential turning point for markets, but if the current volatility persists or increases, then this quote would become very pertinent. And remember, volatility encompasses moves in either direction: UP and DOWN. Investors of course prefer the up moves to the down moves, so many are quite pleased today.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account