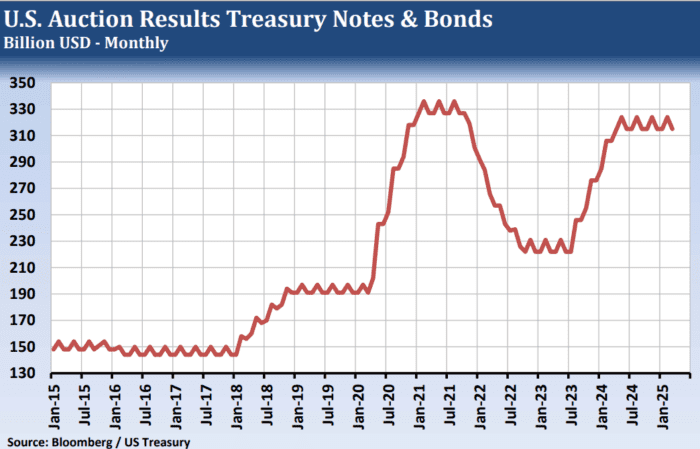

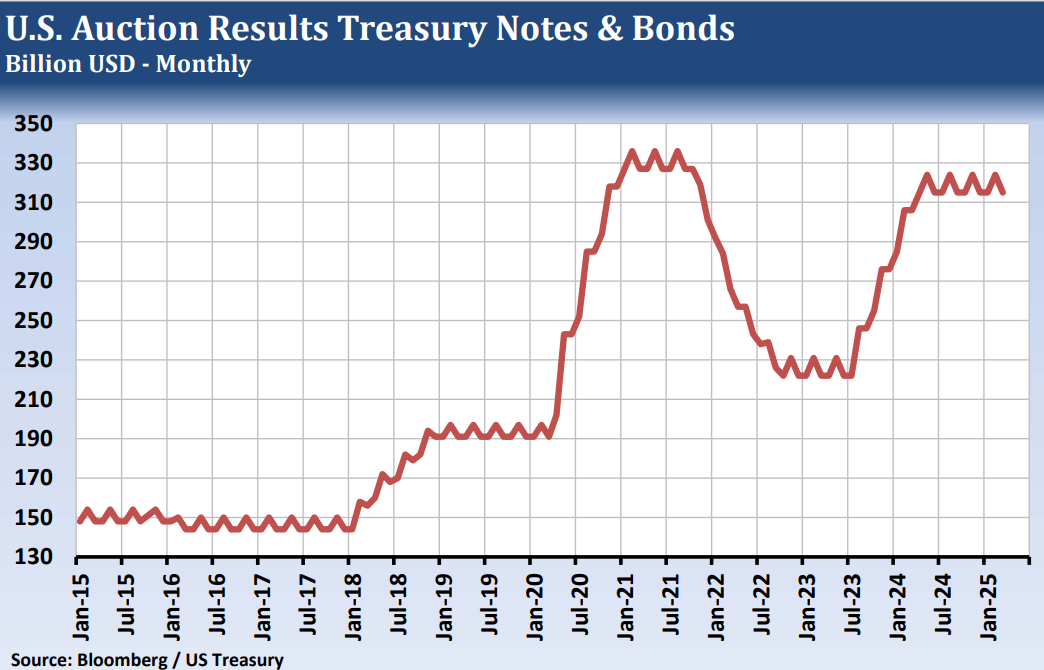

While some may interpret the March slide in Treasury prices as a sign of waning confidence in the US and one of the most prominent and enduring flight-to-quality instruments, additional forces are in play. Following the 9-point January through early March Treasury Bond rally, some measure of technical balancing was needed. However, significant historic supply changes are looming for the Treasury markets, which could eventually shut off an unending explosion of US debt instrument supply. On the other hand, anything associated with Washington, DC, will present significant twists and turns, with history suggesting major change is very unlikely and will take much longer than anticipated. Therefore, traders should separate near-term and long-term prospects in the Treasury markets, with the near-term presenting a bearish track while the long-term potentially creating a significant buying opportunity.

In our opinion, the early 2025 Treasury Bond rally was fueled by slowing fears and ideas that inflation would continue to come down, allowing the US Federal Reserve to cut interest rates. However, fears of economic headwinds flowing from the tariff war and sharp reductions in US government spending have had the surprising impact of sending Treasury prices higher and the US dollar higher. Indeed, traders may be liquidating Treasuries to avoid historic volatility from changes in how business has been done in Treasuries for decades. Treasury Bond open interest has fallen sharply; trading volume has dropped, and the latest net spec and fund long of 126,106 contracts is well below the February 18th high (the largest spec long since 2017), suggesting money is moving to the sidelines.

In the short term, June Bonds appear to be in a downtrend, perhaps due to bearish bond vigilantes who think “nothing will change in Washington.” We also believe negative views toward the US economy going into the March highs have not materialized, leading to traders selling Bonds due to the general resiliency of US economic data. On the other hand, the bearish track could be short-lived if tariff anxiety and Washington infighting reach a crescendo early in April. Remember that even financial markets are subject to classic supply and demand forces. From a technical perspective, the net spec and fund long leaves Treasury Bonds vulnerable to stop-loss selling, especially if prices trade below 115-20. While it might be considered premature and overly optimistic, a significant reduction in US refunding supply from less spending could drive Treasury prices sharply higher in the months ahead.

Past performance is not indicative of future results

—

Originally Published March 28, 2025

This article originally appeared in the March 28, 2025 issue of our Weekly Market Letter. For information about our other products and services, visit https://hightowerreport.com.

This report includes information from sources believed to be reliable, but no independent verification has been made, and we do not guarantee its accuracy or completeness. Opinions expressed are subject to change without notice. This report should not be construed as a request to engage in any transaction involving the purchase or sale of a futures contract and/or commodity option thereon. The risk of loss in trading futures contracts or commodity options can be substantial, and investors should carefully consider the inherent risks of such an investment in light of their financial condition. Any reproduction or retransmission of this report without the expressed written consent of The Hightower Report is strictly prohibited. The data contained herein is subject to revision; independent verification is recommended. Any third-party opinions regarding this report are not necessarily those of the authors. Due to the volatile nature of futures and options markets, the information contained herein may be outdated upon its release.

Disclosure: The Hightower Report

This report includes information from sources believed to be reliable, but no independent verification has been made, and we do not guarantee its accuracy or completeness. Opinions expressed are subject to change without notice. This report should not be construed as a request to engage in any transaction involving the purchase or sale of a futures contract and/or commodity option thereon. The risk of loss in trading futures contracts or commodity options can be substantial, and investors should carefully consider the inherent risks of such an investment in light of their financial condition. Any reproduction or retransmission of this report without the expressed written consent of The Hightower Report is strictly prohibited. The data contained herein is subject to revision; independent verification is recommended. Any third party opinions regarding this report are not necessarily those of the authors. Due to the volatile nature of futures and options markets, the information contained herein may be outdated upon its release.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from The Hightower Report and is being posted with its permission. The views expressed in this material are solely those of the author and/or The Hightower Report and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account