Originally Posted 13 November 2025 – Quarterly thematic insights: thematic edge over broad equity markets

Key Takeaways

- Thematic strategies outperformed broad equity markets in Q3 2025, led by themes aligned with structural shifts in technology, energy and security.

- Investor flows remained concentrated in defence and AI-related exposures, reflecting ongoing geopolitical uncertainty and AI-driven innovation.

- ETFs strengthened their leadership in thematics, capturing the majority of inflows and new product launches that resonated the most with investors, while open-ended funds continued to see redemptions and slower innovation.

- AI-driven energy demand and geopolitical realignment are reshaping investor sentiment, reinforcing the strategic relevance of rare earths, critical minerals, and energy and defence supply chains in global allocation trends.

- Related Products WisdomTree Europe Defence UCITS ETF – EUR Acc, WisdomTree Artificial Intelligence UCITS ETF – USD Acc, WisdomTree Uranium and Nuclear Energy UCITS ETF – USD Acc, WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF – USD Acc, WisdomTree Quantum Computing UCITS ETF – USD Acc, WisdomTree Battery Solutions UCITS ETF – USD Acc, WisdomTree Cybersecurity UCITS ETF – USD Acc Find out more

Imagine knowing, even with just a 50% probability, that a global pandemic would strike in early 2020, triggering a rapid transition to a remote world. Any investor armed with such foresight would have repositioned their portfolios to capture the resulting growth opportunities. Similarly, 2025 is shaping up to be another defining year, one in which major global developments are expected to unlock strong returns across markets. Driven by geopolitical frictions, advances in Artificial Intelligence (AI) and continued macroeconomic uncertainty, the year is increasingly looking to be the year of thematics. In this blog, I explore the key trends reshaping the European thematic landscape, how investors and asset managers are responding, and what the latest allocation dynamics reveal about sentiment across the region.

Q3 performance leaderboard

Q3 2025 saw an improvement in investor sentiment across a range of thematic strategies, with tariff-driven uncertainty taking a backseat, as the worst fears hadn’t previously materialised. Global equities, represented by the MSCI All Country World Index (ACWI), posted a 7.62%1 return for the quarter, while 23 out of 44 European themes within the WisdomTree Thematic Classification performed even better. The average Q3 return of all outperforming themes was at 16.85%1, suggesting that investors not allocating to thematics are missing out on significant growth drivers in their portfolios. On a year-to-date basis, these figures correspond to a 36.21%1 average return of outperforming themes vs. an 18.44%1 return for the MSCI ACWI.

Figure 1. Year-to-date (YTD) and quarter-to-date (QTD) returns of themes in Europe within the WisdomTree Thematic Classification.

Source: WisdomTree, Morningstar, Bloomberg. As of 30 September 2025. All data based on WisdomTree’s internal classification of thematic funds. Performance is based on monthly returns from Morningstar. Please refer to Footnotes for the details around the calculation of performance for a given theme2. Historical performance is not an indication of future performance, and any investments may go down in value.

Q3 has redrawn the leaderboard of the top themes by year-to-date performance. In Q3, the ‘Energy Transition Materials’ theme took the lead, driven in part by rare earths emerging as a central bargaining point in US–China trade talks. The theme has entered the top five year-to-date (YTD) performers alongside ‘Rise of China Tech’, complementing Q2 leaders ‘Rise of Tension’, ‘Nuclear’ and ‘Space’. Having been catalysed by strategic policy moves in the US, the theme received fresh momentum when the US government, via the Department of Defense, announced a US $400 million investment in MP Materials in July 2025. This was further followed by the US and Australia signing a framework agreement in October 2025, aimed at strengthening critical-mineral and rare-earth supply chains and reducing dependence on China.

The ‘Rise of China Tech’ theme delivered a 30.9% return in Q3, the second-strongest performance among all themes. It benefited from China’s newly announced anti-involution policies, aimed at curbing oversupply and improving margins by addressing unfair price competition in the technology and manufacturing sectors. Earlier in the year, investor sentiment was boosted by DeepSeek’s release and a perceived shift in the Chinese government’s stance toward leading technology companies, which signalled greater regulatory support for innovation and capital markets. At the same time, China’s global leadership in electric vehicles, batteries and its growing strength in AI and robotics continued to underpin positive momentum in the theme.

The ‘Nuclear’ theme rounded out the top three performers in Q3, extending its strong momentum from Q2. Propelled by US executive orders in May 2025 aimed at quadrupling the country’s nuclear power capacity by 2050, the theme was buoyed in Q3 by the surge in AI-driven energy demand and a series of partnerships announced between OpenAI and major technology companies. The theme also gained visibility as a key area of collaboration under the US-UK Tech Prosperity Deal. In late October 2025, the announcement of a US $80 billion partnership between the US government, Cameco, and Brookfield Asset Management, aimed at building nuclear reactors, provided an additional boost to nuclear-supply-chain players.

The ‘Sustainable Energy Storage’ theme was a surprising entrant into the top five in Q3, marking a reversal of its weaker trend in prior periods. As AI-driven energy demand rises, global power generation is expanding across all sources, including renewables, where energy storage plays a critical role in balancing supply from intermittent sources such as solar and wind. For instance, some data centres have begun deploying fuel cells to meet surging power needs, in contrast to small modular reactors (SMRs), which remain several years away from large-scale deployment. In parallel, the continued growth of electric vehicles provides an additional tailwind for battery demand.

The ‘Blockchain’ theme rounded out the top five performers, benefiting not only from supportive US policy developments but also from crypto miners’ strategic pivot toward providing high-performance computing infrastructure to meet the surge in AI-related workloads. Overall, the top five themes delivered returns ranging from 21% to 36%, demonstrating clear outperformance versus broad equity markets. The strong outperformance of a range of themes in 2025 versus global equities is especially evident in comparison to previous years (see Figure 2).

Figure 2. Calendar returns across sub-clusters in the WisdomTree Thematic Classification.

Source: WisdomTree, Morningstar, Bloomberg. Period from 31 December 2022 to 30 September 2025. Calculations are based on WisdomTree’s internal classification of thematic funds. Performance is based on monthly returns from Morningstar. Historical performance is not an indication of future performance, and any investments may go down in value.

Flows roundup

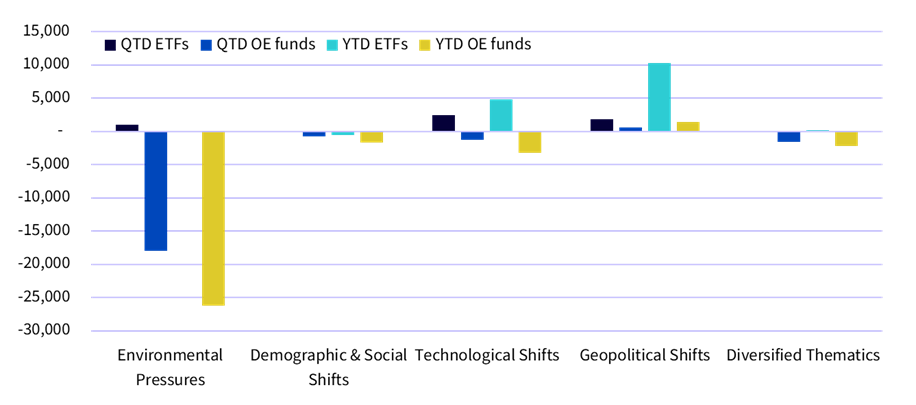

Q3 flows into thematic strategies in Europe highlighted the widening divergence between exchange-traded funds (ETFs) and open-ended funds, with ETFs attracting $4.9 billion in inflows while open-ended funds saw $4.5 billion in redemptions. On a year-to-date basis, the split is even more pronounced, at $9.4 billion of ETF inflows versus $10.9 billion of outflows from mutual funds.

The quarter also marked a turning point, as ETFs posted positive flows across all thematic clusters except for ‘Demographic and Social Shifts’. In contrast, mutual funds registered net inflows only within the ‘Geopolitical Shifts’ cluster, which includes defence-focused strategies under the ‘Rise of Tensions’ theme. During the period, investors allocated $560 million to open-ended funds and $1.85 billion to ETFs following this theme. The ‘Rise of Tensions’ theme has been a stand-out winner in 2025 in flows ($11.3 billion) and investor interest, reflecting Europe’s strategic pivot toward greater military independence.

Figure 3. Year-to-date (YTD) and quarter-to-date (QTD) thematic flows in ETFs and open-ended (OE) funds in Europe across clusters in the WisdomTree thematics universe ($ millions).

Source: WisdomTree, Morningstar, Bloomberg. As of 30 September 2025. Data based on WisdomTree’s internal classification of thematic funds. Historical performance is not an indication of future performance, and any investments may go down in value.

Within the ‘Environmental Pressures’ cluster, ETFs attracted over $1 billion of inflows in Q3, led by ‘Energy Transition Materials’ ($511m) and ‘Nuclear’ ($220m). These flows reflect positive investor sentiment toward themes aligned with recent performance trends.

In the ‘Technological Shifts’ cluster, ‘AI and Big Data’ and ‘Rise of China Tech’ stood out, recording ETF inflows of $1.15 billion and $976 million, respectively, during Q3. This brought year-to-date flows across both wrappers (ETFs and open-ended funds) to $2.5 billion and $1.97 billion, respectively. While AI has not yet been a standout performer in 2025, it remains a dominant structural force driving returns across global equity markets, explaining strong investor interest in the theme. This focus on AI has elevated the theme to the top position within European thematics, with $31.3 billion in assets under management (AuM), reflecting its core status within the thematic space. Meanwhile, ‘Rise of China Tech’ continued to benefit from renewed investor interest in the Chinese market and its technology-driven sectors in particular.

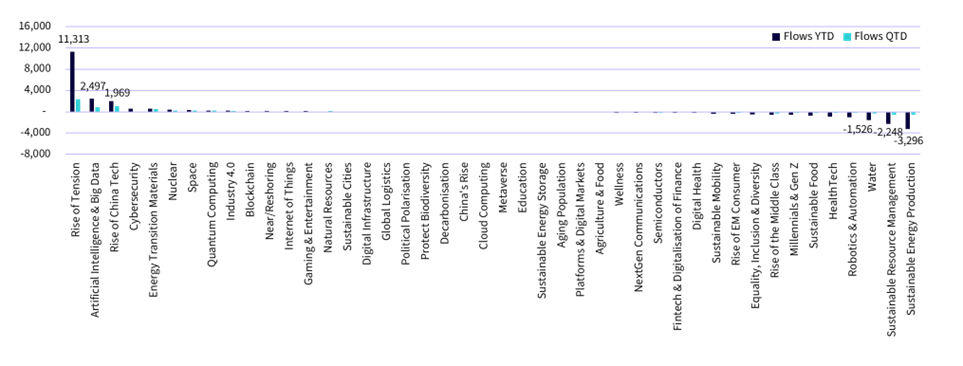

Figure 4. Year-to-date (YTD) and quarter-to-date (QTD) flows across themes in Europe within the WisdomTree Thematic Classification ($ millions).

Source: WisdomTree, Morningstar, Bloomberg. As of 30 September 2025. Data based on WisdomTree’s internal classification of thematic funds. Historical performance is not an indication of future performance, and any investments may go down in value.

On the other end of the spectrum, sustainable themes continued to face headwinds, with investors withdrawing approximately $7.1 billion year-to-date from the three weakest-performing themes, led by ‘Sustainable Energy Production’. While outflows slowed sharply in Q3, they highlighted a broader investor rotation away from sustainability-focused exposures, as AI-driven energy demand renews attention on the full energy mix needed to support surging energy needs.

Notable trends in ETFs vs. open-ended funds

The divergence in flows between thematic ETFs and open-ended funds has driven a rapid rise in ETFs’ market share, increasing from 14.7% at the end of 2024 to 21.9% at the end of September 2025. Most of this expansion can be attributed to strong inflows into defence-focused strategies, particularly the European Defence segment. In this area, ETFs have proven more agile, being the first to market and scaling assets faster compared to open-ended funds.

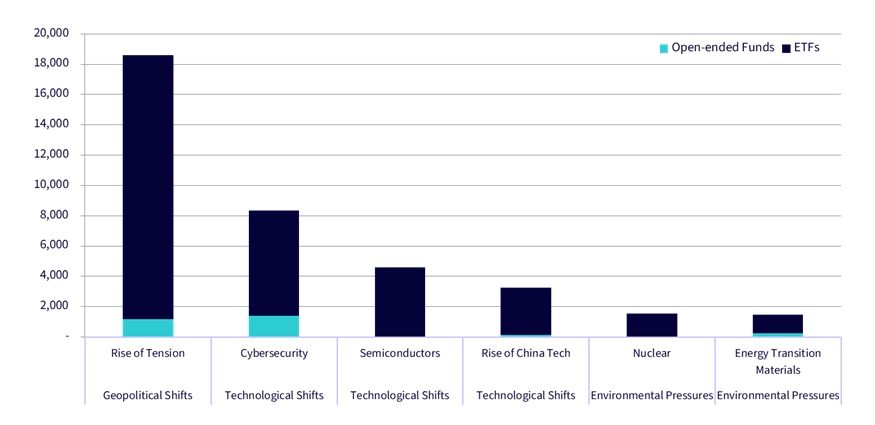

A similar pattern emerges across other top themes by AuM, where ETFs account for more than 80% of thematic assets (see Figure 5). This dominance is most evident in the themes that captured the bulk of investor interest outside of ‘Rise of Tensions’. For instance, ‘Energy Transition Materials’, ‘Rise of China Tech’, and ‘Nuclear’ – the top three performers in Q3 – are primarily represented by ETFs. In addition, ETFs continue to lead in ‘Semiconductors’ and ‘Cybersecurity’, two themes closely linked to the proliferation of AI and underpinned by a compelling long-term structural growth narrative.

Figure 5. Top five themes with AuM share of ETFs > 80% ($ millions).

Source: WisdomTree, Morningstar, Bloomberg. As of 30 September 2025. Data based on WisdomTree’s internal classification of thematic funds. Historical performance is not an indication of future performance, and any investments may go down in value.

Outflows from thematic open-ended funds have led to a notable slowdown in the launch of new strategies by active asset managers. In contrast, ETF issuance has accelerated in 2025 compared with 2024, highlighting a growing divergence in product development momentum. This widening gap may further disadvantage open-ended funds, which risk missing out on key emerging themes that are likely to drive future investor interest and asset growth.

Figure 6. Historical launches of thematic strategies in Europe.

Source: WisdomTree, Morningstar, Bloomberg. As of 30 September 2025. Data based on WisdomTree’s internal classification of thematic funds. Historical performance is not an indication of future performance, and any investments may go down in value.

Bottom line

The latest trends in performance, flows and product launches place ETFs firmly at the forefront of innovation within thematic investing. Over the past few years, thematic ETFs have evolved into a key component of investors’ equity toolkits, offering targeted exposure to structural growth drivers aligned with the technological, regulatory, geopolitical, macroeconomic and consumer trends shaping global markets.

As these forces continue to unfold, thematic strategies are well-positioned to offer compelling satellite exposures to broad equity strategies by capturing opportunities linked to long-term transformation. To stay on top of the latest developments in thematics and allocation ideas, stay tuned for our next quarterly update.

1All figures are based on the WisdomTree’s internal classification of thematic funds and WisdomTree’s calculations using the underlying data from Morningstar and Bloomberg.

2Performance of a theme. Each month, we include all ETFs and open-ended funds classified under a specific theme that have reported a monthly return in Morningstar. We calculate the average of these returns to determine that month’s performance for the theme. For example, the January 2020 return for a theme might include 19 funds, while February 2020 might include 21, if new funds were launched. By combining these monthly averages, we build the theme’s historical performance. This approach includes every fund active in a given month, regardless of its future success or survival, ensuring the results are not biased towards funds that still exist. Funds that span multiple themes and are classified only at the Cluster or Sub-Cluster level are excluded.

Disclosure: WisdomTree U.S.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Alternative Investments

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account