Another day, another set of declines in popular financial assets. Unfortunately, there is nothing new about that. What is different this time – and I acknowledge that to be among investors’ most dangerous phrases) – is that today is less about rotation than outright selling. Although this morning’s declines in major indices are roughly commensurate with those of recent days, the underlying metrics are not.

As I type this before noon ET, the S&P 500 (SPX) and Nasdaq 100 (NDX) have recovered from their intraday lows. Both are about -0.9% lower, but SPX has recouped about a third of its worst losses, and NDX has recovered a bit more than half. That is commensurate with the daily trading patterns that have prevailed over the past few days. Stocks sold off, then recovered from their worst levels when dip buyers stepped in. The chart below shows this occurring in five of the prior six sessions, with today following that pattern for a sixth:

SPX, 8-Days, 5-Minute Candles

Source: Interactive Brokers, Past performance is not indicative of future returns.

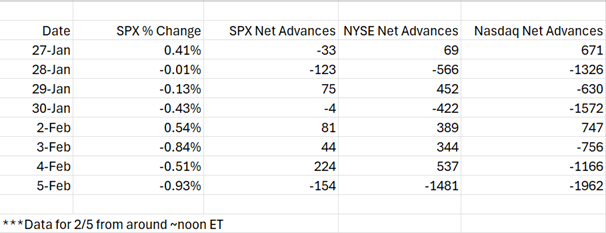

Today, however, we see more selling across the board. In the period covered by the above graph, it was not uncommon to see more SPX stocks advancing than declining even as the index sank. Note yesterday’s figure, which showed nearly half of SPX stocks advancing despite a -0.51% selloff:

Net Advances vs. Daily % Change

Source: Interactive Brokers, Past performance is not indicative of future returns.

The net advances on the NYSE roughly followed those of the SPX, while Nasdaq, unsurprisingly, leaned more negatively. The recent selloff – it’s not even close to a correction, by the way – has been led by technology stocks, particularly in the software sector. Think of how many times you’ve heard the phrase, “tech-heavy Nasdaq.” Our previous assertion that the relatively modest index declines were more the result of turbulent rotation under the market’s surface than broad-based selling was borne out by the data. Today’s advance-decline statistics indicate that situation has changed.

Perceptions about the economy are the main culprit for this morning’s change in psychology. Challenger Job Cuts soared by 117.8% on a year-over-year basis, largely thanks to major layoffs at UPS, Amazon, and Dow Chemical (DOW). Initial Jobless Claims rose to 231,000 from 209,000, well above the 212,000 consensus. Continuing Claims rose from a revised 1,819K to 1,844K, though today’s figure was slightly below the 1,850K consensus. And JOLTS data added to the gloom at 10:00 AM ET. The December figure came in at 6,542K, well below the 7,250K consensus and November’s 6,928K, which itself was revised down from the originally reported 7,146K.

The jobs data gave economic bulls a bit of pause, particularly with the January employment report pushed back from tomorrow to Wednesday. Bond yields fell about 6 basis points across the curve. The move at the short end reflected that Fed Funds futures were now pricing in a full cut for the June FOMC meeting rather than July and a second cut is now solidly priced in for December. The rotation reflected enthusiasm for the economic outlook. Today’s reports dampened that enthusiasm, and hence the rotation turned to outright negativity.

Yet most questions that I continue to receive involve the selloff in software, and more broadly in technology stocks. I believe that to be the result of two key factors:

- The consensus has flipped to software companies being AI victims – not beneficiaries. Investors were willing to pay premium multiples for software companies that could reap efficiencies from utilizing AI in their coding and final products. That view abruptly reversed, with software companies now perceived as victims of AI’s disruption.

- Crowded trades are difficult to exit. Assets that have been granted premium valuations, whether through rational expectations or speculative fervor, are more prone to messy selloffs if perceptions and/or momentum change.

We discussed some of this yesterday, how highly valued stocks can be much more vulnerable to unpleasant hiccups. Many of the popular software stocks traded with very high P/Es, reflecting high expectations for future growth.

Unfortunately for other recent speculative darlings, such as silver, there are no earnings expectations. It’s much more about supply and demand, and those dynamics have flipped markedly. Dip buying is very different when there are fewer obvious fundamentals to base one’s buying upon.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account