Yields are jumping after Fed Chair nominee Kevin Warsh adopted a hawkish stance during today’s Senate hearing. His opinion that the central bank’s post-pandemic policy errors directly lifted price pressures well above the institution’s target are further positioning him as an inflation fighter that isn’t afraid to tighten financial conditions. The comments have fixed-income watchers doubtful about a cut this this year, as just a 30% chance exists of a reduction before January. The projection of a higher-for-longer regime is sending the yield curve north in bear-flattening fashion led by the short end, while climbing crude costs and strong economic data additionally weigh on Treasurys. Indeed, President Trump stating that if an Iran deal isn’t closed it’s likely that the war will resume, which has raised the geopolitical premium. Meanwhile, the strongest monthly retail sales increase in 38 months, the fastest number of weekly payroll increases reported by ADP and a beat on pending home transactions also contributed to loftier rates. In trading, all four major domestic benchmarks are now retreating subsequent to heavy morning gains in which the Russell 2000 marked a fresh record. All sectors are in the red minus tech and energy while hedging demand rises as volatility protection instruments catch bids. Elsewhere, the greenback is appreciating, non-energy commodities are sinking.

Retail Growth is Strongest in 38 Months

Retail sales growth in March accelerated to 1.7% month over month (m/m) from the 0.7% rate in February and exceeded the economist consensus estimate for a 1.4% jump, according to preliminary data from the US Census Bureau. Core retail sales, which exclude items with volatile pricing, were even stronger, jumping 1.9% m/m after February’s 0.7% northward movement. Economists estimated that the total value of transactions would be 1.4% higher than during February. The retail control group, which is used in computing the nation’s gross domestic product, was also encouraging. It ascended 0.7% m/m, which exceeded the economist estimate of 0.2% and strengthened modestly from 0.6% in the preceding month. When extracting the impact of gasoline, sales were up 0.6% m/m, matching February’s result.

Past performance is not indicative of future results.

The following categories and the extent of their respective sales changes supported the headline increase:

- Gasoline stations, 15.5%

- Furniture and home furnishing, 2.2%

- Ecommerce, 1%

- Electronics and appliance stores, 0.9%

- Building materials, garden equipment, and supplies dealers, 0.7%

- Motor vehicle and parts dealers, 0.5%

March’s decliner was the miscellaneous store retailer group. With a 0.9% contraction, it was the only category to post a negative. Additionally, the sporting goods and apparel categories were unchanged.

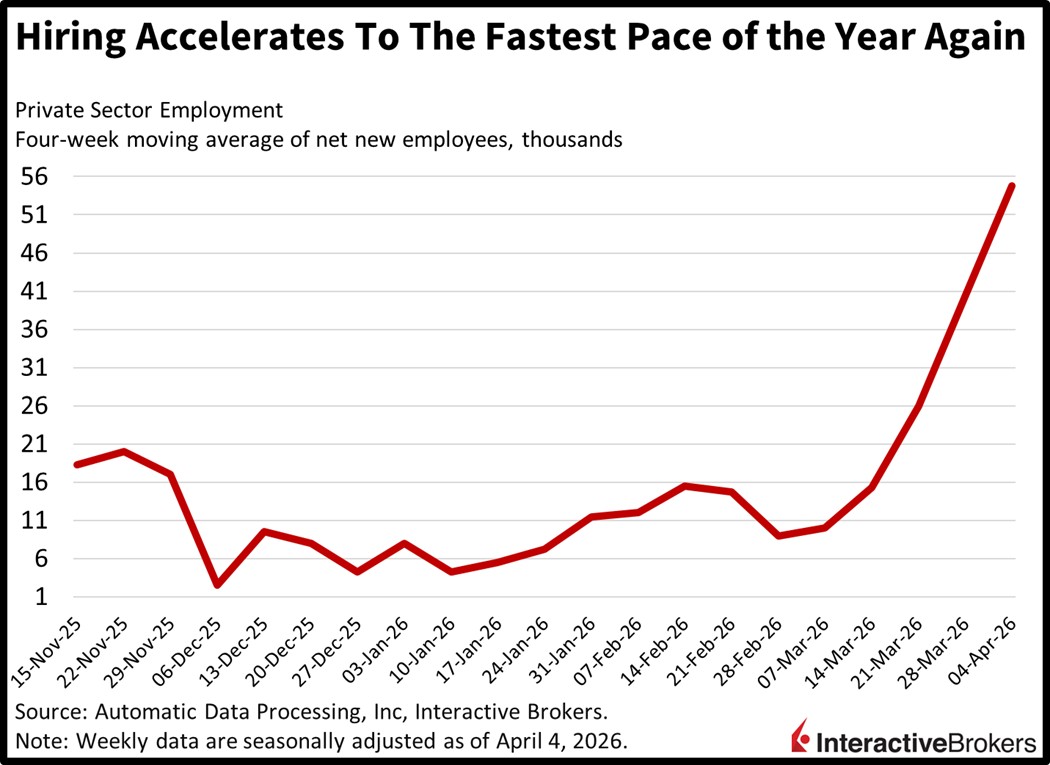

ADP Data Points to Uptick in Hiring

Private sector hiring leaped in March and in the beginning of this month as the rate of payroll expansions ramped up to the fastest pace all year. Worker rosters jumped by an average of 54.75k employees in each of the four weeks during the period that ended April 4, stronger than the 40.25k print from the prior publication, according to ADP.

Past performance is not indicative of future results.

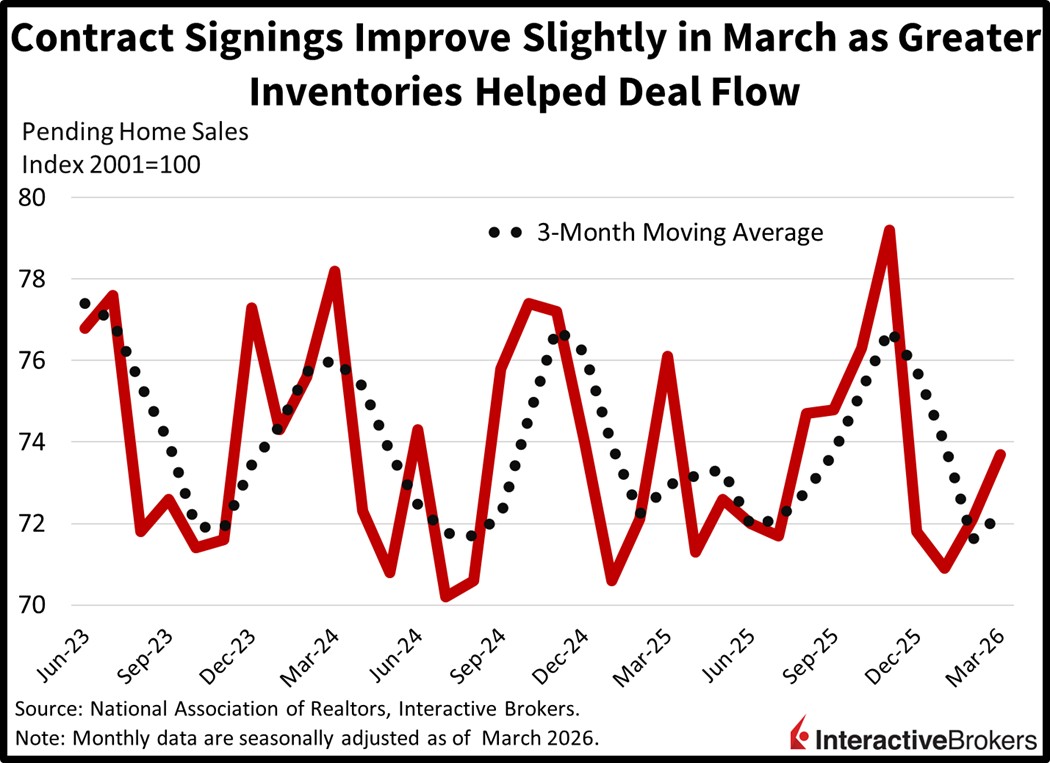

Pending Home Sales Climb Again

Pending home sales rose for the second consecutive month in March as increased inventory helped deal flow. The 1.5% m/m expansion beat the 0.1% median estimate but moderated from February’s 2.5%. Regional performance was bifurcated with the Northeast, and South expanding 4.4% and 3.9% while the West and Midwest sank 2.6% and 1.3% m/m. Still, the real estate sector remains in recession as closings and construction activity remain depressed relative to historical standards.

Past performance is not indicative of future results.

Markets Are Close to Pricing in a Hike

With the Middle East ceasefire deadline approaching alongside the potential that an inflation fighting Fed Chair is confirmed, markets are once again getting close to pricing in a hike. Towards late March and the beginning of April, rate watchers thought that the inflationary pressures from the Iran war would push the central bank to raise by the finish of the year, but those concerns were quelled after light appeared at the end of the geopolitical tunnel. Now, though, there’s a chance of dual risks that could present a lift in rates, with WTI currently north of $90 a barrel while nominee Kevin Warsh is highly critical of past monetary policies for their lack of restrictiveness. Pair those two factors with an acceleration in hiring, subdued unemployment and momentous consumer spending, as we saw in this morning’s reports, and President Trump’s wishes for lighter borrowing costs may simply not materialize in 2026.

International Roundup

UK Payrolls Declined in March

UK payrolls declined in March in a continuation of recent labor weakness, according to data from the Office for National Statistics (ONS). Early estimates point to the number of gainfully employed in March falling by 65,000, or 0.2%, year over year (y/y) but staying nearly flat relative to February, with a drop of 11,000, or roughly no percentage change. During the month, 26.8k individuals filed for unemployment benefits, much worse than the economist estimate of 21.4k and up from February’s 17.1k result. In a related matter, help-wanted postings also contracted with early estimates showing first-quarter job openings falling by 29,000, or 3.9%, compared to the October to December period.

And UK Wage Growth Slows

UK workers’ average earnings ex bonus and with bonus climbed 3.6% and 3.8% y/y as of February, with the pace slowing from 3.8% and 4.1% in January. The gains were also lower than the economist consensus estimates of 3.5% and 3.6%. Real wages, which include the impact of the Consumer Price Index including owner occupiers’ housing costs, however, were up only 0.2% for regular pay and 0.4% when including bonuses.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account