Tech stocks are rallying more than 1% and are heading to their tenth consecutive day of advances as Middle East peace hopes and a miss on PPI energize bulls. Optimism has grown about Washington and Tehran negotiating again in the near future against the backdrop of a ceasefire that expires in the middle of next week, which is bolstering animal spirits after causing WTI oil prices to tank to $91.92, the lowest level since last Wednesday. The US naval blockade appears to be pressuring Iran, as the regime considers pausing transit to avoid a confrontation with the US, and that, too, is strengthening confidence about a potential end to the war. Today’s economic calendar also supported the tape as a lighter-than-expected PPI weighed on yields while ADP reported the strongest numbers of weekly hiring all year. The results helped to sideline short-run inflation worries while boosting sentiment regarding the cyclical outlook. The four major averages are appreciating notably alongside Treasuries across the curve and non-energy commodities. Conversely, the greenback is slipping on sinking domestic rates and volatility protection instruments are seeing lessening premiums in light of risk-on attitudes on Wall Street.

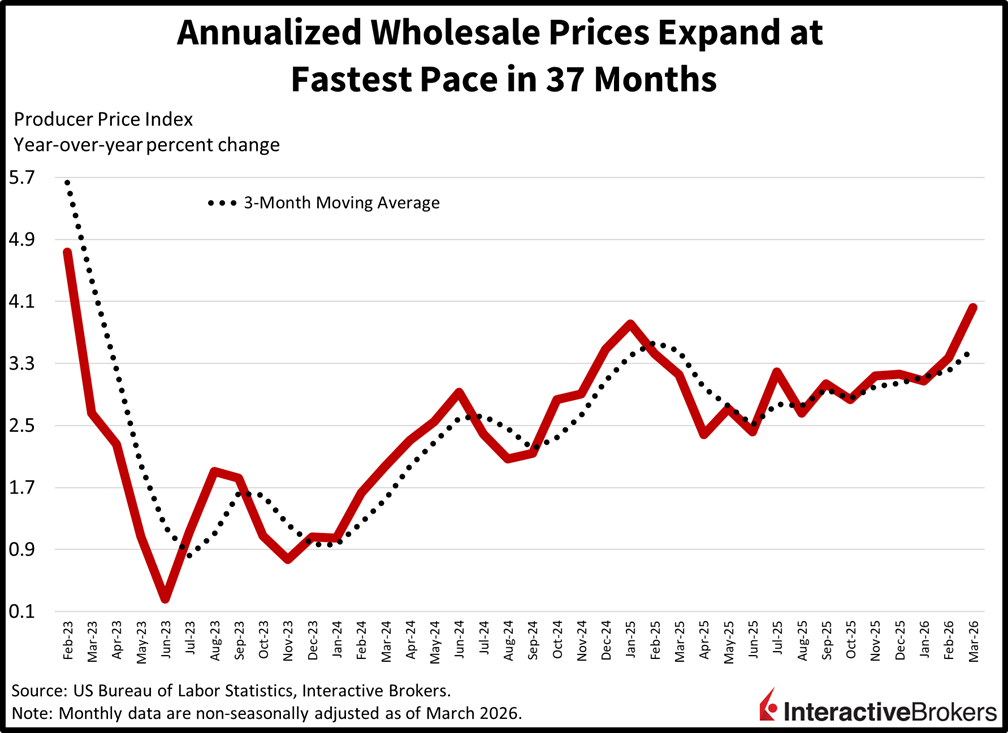

PPI Sooths Inflation Jitters

Wholesale inflation climbed at the same pace as February, dismissing worries that the Middle East conflict triggered a significant spike in March cost pressures. Indeed, last month’s Producer Price Index (PPI) rose 0.5% month over month (m/m) and 4% year over year (y/y), missing the median estimates of 1.1% and 4.6% by substantial amounts while the previous print came in at 0.5% and 3.4%. Despite coming in well beneath expectations, the annualized statistic was the loftiest in 37 months, or since February 2023. Helping drive the miss were flat m/m overall services charges and a 0.3% m/m decline in food. Categories that became more expensive, meanwhile, were energy, transportation/warehousing services, core goods and other services with prices climbing 8.5%, 1.3%, 0.2% and 0.1% m/m. Similar to last week’s more closely watch Consumer Price Index, this report downplayed the 41.7% and 25.1% m/m increase in crude oil and gasoline, which will likely show up in the subsequent release.

Past performance is not indicative of future results.

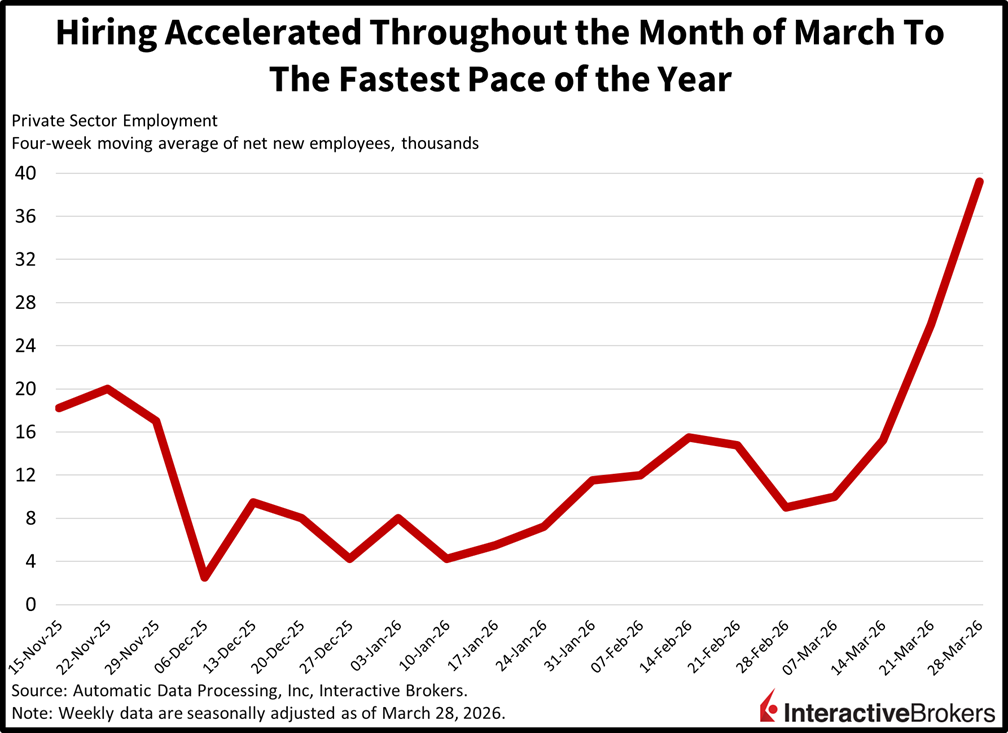

Labor Market Strengthens

Private sector hiring soared in March as employment additions accelerated at the fastest pace all year, defying worries about slowing payroll expansions and a decelerating economy. Employer headcounts jumped by an average of 39.25k workers in each of the four weeks during the period that ended March 28, ahead of the 26k print from the previous publication, according to ADP.

Past performance is not indicative of future results.

But Small Business Optimism Weakens

Small business optimism sank last month with weaker profitability and deteriorating economic conditions weighing the most on the outlook. The 95.8 March headline was below the 98.6 median estimate and February’s 98.8. Firms grew increasingly pessimistic about expansion prospects, hiring and inventory levels. Additionally, the single most important problem was taxes, which were cited by 19% of respondents, followed by labor quality, inflation, poor sales and employee costs at 15%, 14%, 10% and 10%.

Past performance is not indicative of future results.

Middle East Peace, Earnings to Sustain Stocks

With investors now increasingly pricing in Middle East peace and elevated fuel costs likely to be overlooked when corporates offer earnings guidance as a result of a simmering conflict, stock market volatility is looking like it can stay suppressed. But yields are poised to become a threat, as annualized inflation figures are geared to remain in the 3s all year irrespective of what happens between Tehran and Washington. Indeed, despite the reprieve in crude oil today, it remains 50% above where it was 12 months ago, which actually bodes well for price pressures in 2027; however, it will impede a 2-handle on the CPI or PPI in 2026. Still Treasuries are about 25 basis points (bps) away from levels that would signal trouble for equities, namely 4% on 2s and 4.50% on 10s, meaning that shares can continue to run higher, especially if President Trump can seal a deal with Iran.

International Roundup

China’s Trade Surplus Takes a Hit From Middle East Crisis

Demand destruction from the Middle East conflict weighed heavily on China’s exports last month, causing the country’s year-to-date trade surplus through March to contract 3% y/y to $264.3 billion. In the third month of this year, the surplus of $51.13 significantly missed the economist consensus estimate of $112 billion. Indeed, March exports climbed only 2.5% y/y, an abrupt deceleration from the 21.8% jump in February and below the economist consensus estimate of 8.3%. The value of products shipped to the Middle East were particularly weak with China’s customs vice minister commenting that fierce oil price fluctuations have created a “complex and severe” trade environment. Imports were a different story, jumping 27.8% y/y, more than twice the estimate of 11.1%. They were considerably stronger than the 19.8% expansion in February.

Singapore Quarterly GDP Contracts

Singapore’s first quarter gross domestic product declined by 1.3% relative to the last three months of 2025 but was still up 4.6% when compared to the year-ago period, according to preliminary data from the country’s Ministry of Trade and Industry (MTI). Nevertheless, the quarter-over-quarter (q/q) contraction was more severe than the economist consensus estimate for a 0.5% decline following the fourth quarter’s 1.3% ascent. It was also the first q/q descent since the 0.6% drop during the three months ended in February 2025. The y/y metric, furthermore, missed the economist estimate for a 5.4% growth rate and was weaker than the fourth-quarter positive 5.7% print. In releasing the data, the MIT noted that the country’s economic growth is likely to slow as a result of the Iran War, which in addition to raising prices pressures is snarling supply chains. The Monetary Authority of Singapore, in a separate statement, echoed those concerns.

Japan Industry Weakens

Industrial production in Japan slipped 2% m/m in February, a notable deterioration from the 4.3% advance in January. It was only slightly better than the economist consensus expectation for a 2.5% drop. Capacity utilization, furthermore, declined 0.1% m/m in February after increasing 2.9% in January.

Australia Biz and Consumer Sentiment Sinks

Australia business confidence fell in March and consumer sentiment weakened considerably this month with higher energy prices and concerns about the Middle East clouding the outlook for the country’s economy. The NAB Business Confidence print pegged confidence at a negative 29 from February’s goose egg result. It was the second largest plunge in the gauge’s history. The transport and utilities category, the construction segment and the retail category experienced the largest declines, largely due to those economic areas having the most sensitivity to higher costs for consumers. Survey respondents’ views of current business conditions were resilient, remaining unchanged at six. NAB attributes the resiliency to the economy having a healthy level of momentum prior to the start of the Middle East hostilities. Sentiment among consumers also weakened significantly with the Westpac Consumer Sentiment Index dropping 12.5% to 80.1. It is the largest decline since the Covid-19 pandemic. Westpac attributes the deterioration to a cost-of-living shock caused by a spike in fuel Australia’s central bank increasing its key interest rate by 25 basis points. Declines in sentiment occurred across the gauge’s five main categories, led by the consumers’ assessments of their current conditions and family finances relative to the year-ago period.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account