Originally Posted, 3 Dec 2024 – Gold Silver: Major Factors That Could Impact Implied Volatility and Skew in 2025

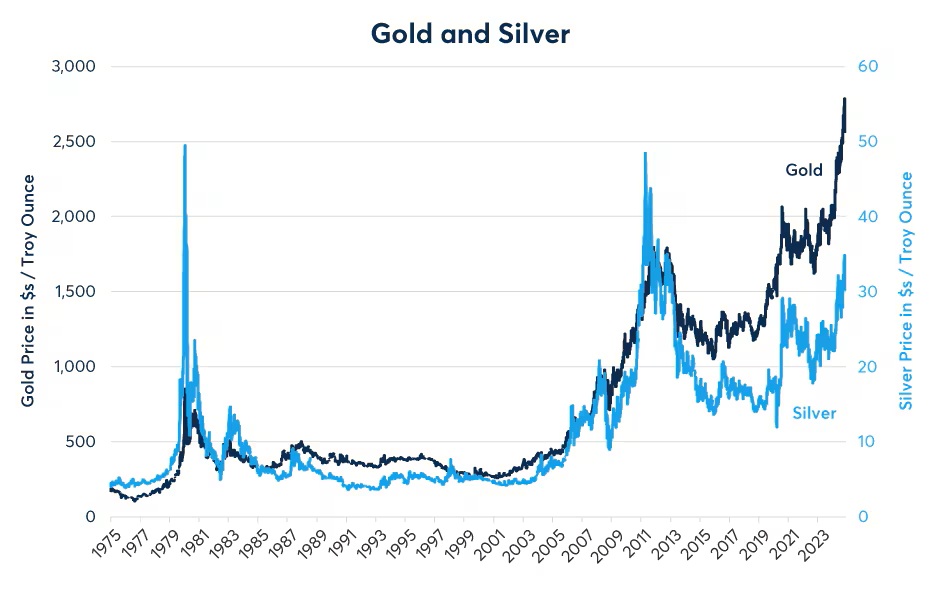

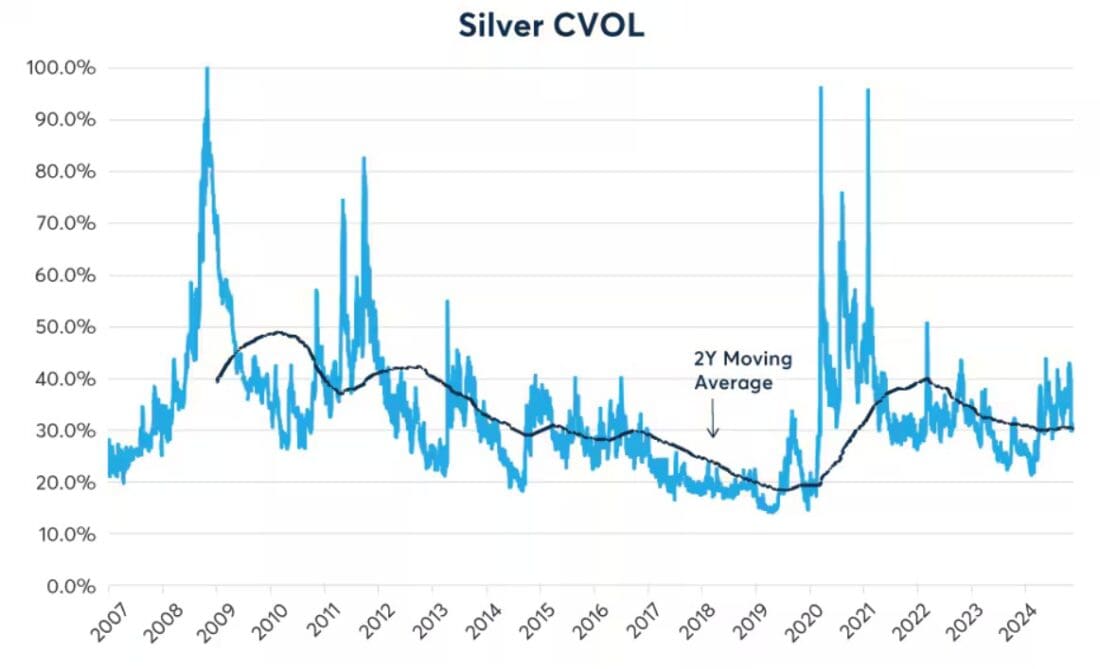

Gold and silver made significant moves in 2024, with the yellow metal hitting an all-time high of over $2,800 in November, while silver rose to its highest levels since 2013 (Figure 1). However, if one looked at the overall level of implied volatility on gold and silver options, one might not have guessed the scale of the price moves. Neither gold nor silver options implied volatility changed much in 2024, as indicated by CME Group’s comprehensive CVOL measure (Figures 2 and 3). That said, implied volatility did fall sharply for both metals during the post-election price correction.

Figure 1: Gold rallied to a record and silver to multi-year highs pre-election

Source: Bloomberg Professional (GOLDS and XAG) – Past performance is not indicative of future results

Figure 2: Gold implied volatility has been at average to somewhat low levels thus far in 2024

Source: QuikStrike (Gold CVOL, OG_30D_ATM_Vol Pre-October 2013) and CME Economics Research Calculations – Past performance is not indicative of future results

Figure 3: Implied volatility on silver futures options has also been at moderate levels

Source: QuikStrike (Silver CVOL and, pre-October 2018, SO_30_ATM) and CME Economics Research Calculations – Past performance is not indicative of future results

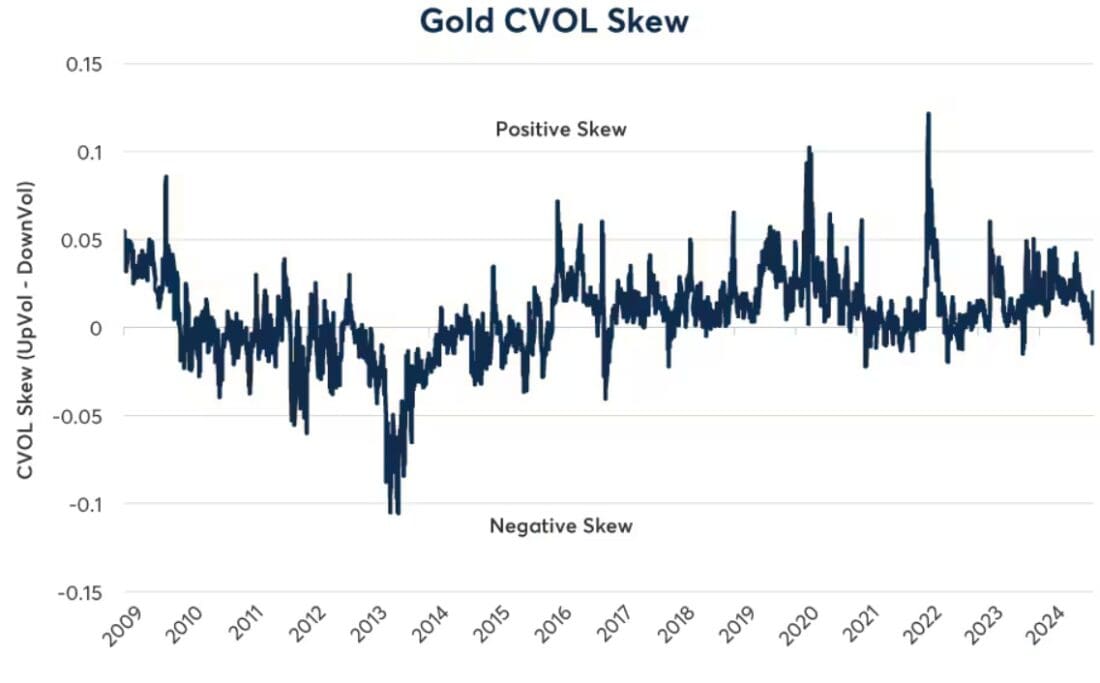

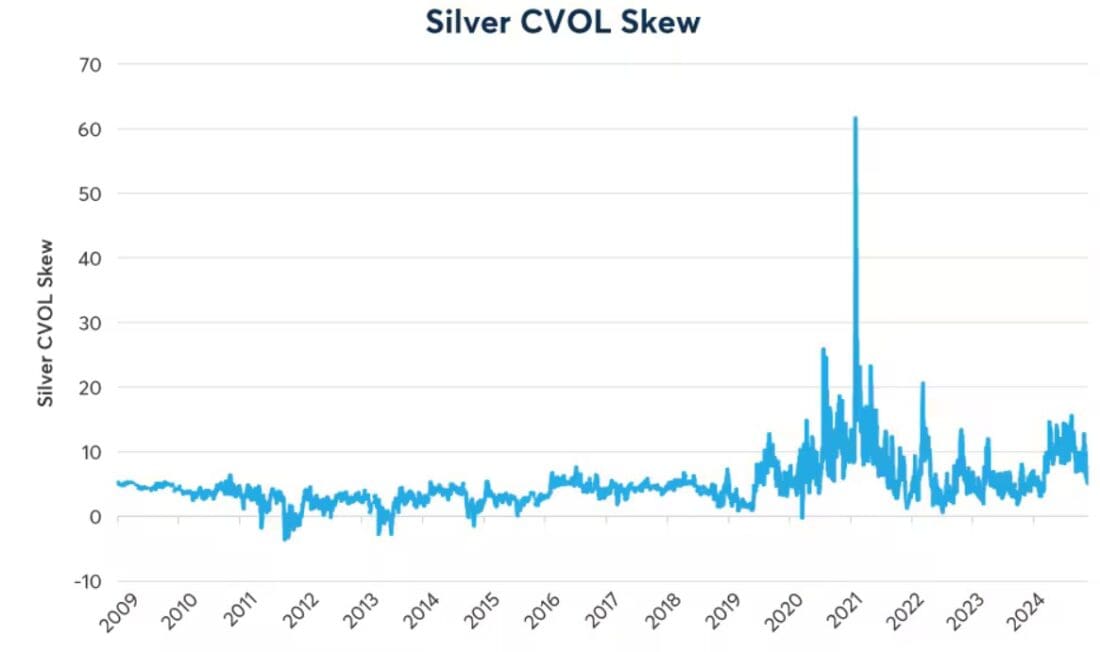

During the selloff, the skew on gold and silver options, which had been positive earlier in the year with out-of-the-money (OTM) calls substantially more expensive than OTM puts, headed back towards neutral (Figures 4 and 5).

Figure 4: The post-election correction in gold prices has taken the skew back towards neutral

Source: QuikStrike (Gold CVOL Skew, OG_30 Risk Revseral Skew (C-P) Pre-October 2013, Bloomberg Professional (FDTRMID) – Past performance is not indicative of future results

Figure 5: The post-election decline in silver prices also dampened silver’s normally positive skew

Source: QuikStrike (SILVER CVOL Skew and, pre-October 2018 SO_30 Risk Reversal), Bloomberg Professional (GC1) and CME Economics Research Calculations – Past performance is not indicative of future results

Here are what we see as some of the major influences on gold and silver prices going forward that could impact both overall implied volatility and skew:

Rate expectations

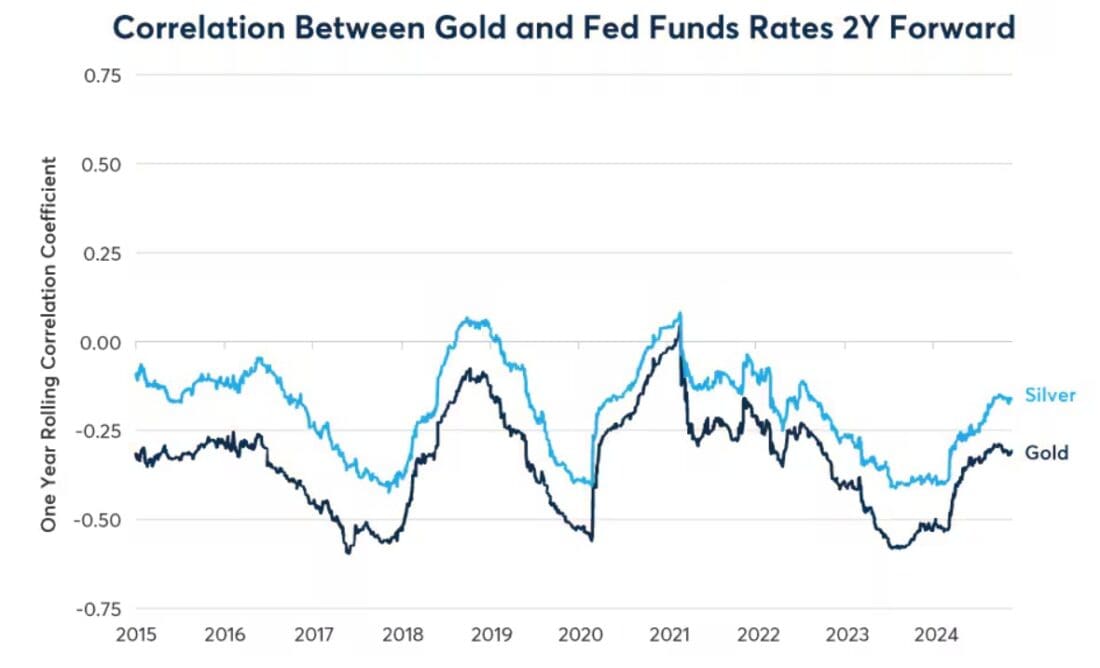

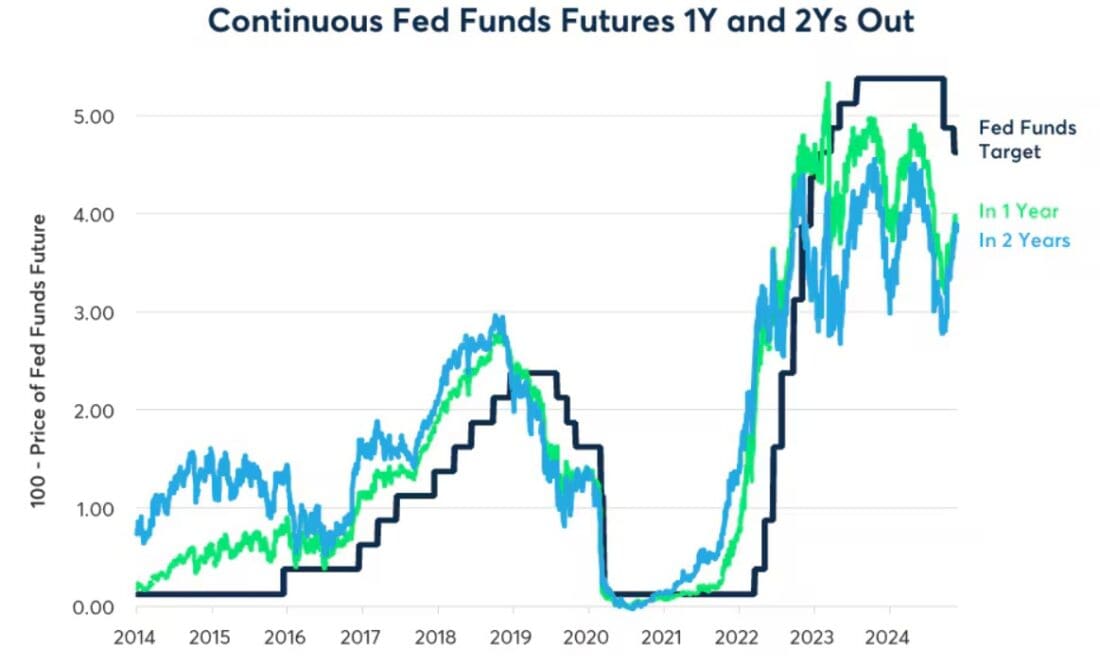

Gold and silver prices both typically react negatively to changes in interest rate expectations (Figure 6). During Q3, Fed Funds futures went from pricing relatively few rate cuts to pricing the Fed would likely lower rates to 2.75% from above 5%. Thus far in Q4, rate expectations have moved back in the opposite direction, and this may have contributed to the post-election correction in precious metals’ prices (Figure 7). This move happened amid solid employment gains and stubborn core inflation, which has stablized at around 3.3% for the past six months and remains well above the Fed’s inflation target of 2%.

Figure 6: Gold and silver correlated negatively with changes in Fed rate expectations

Bloomberg Professional (GC1, SI1 and FF1 .. FF24) and CME Economic Research Calculations – Past performance is not indicative of future results

Figure 7: Fed rate expectations have been very volatile for the past three years

Source: Bloomberg Professional (FF1 … FF24), CME Economic Research Calculations – Past performance is not indicative of future results

The U.S. Dollar, Tariffs and Sanctions

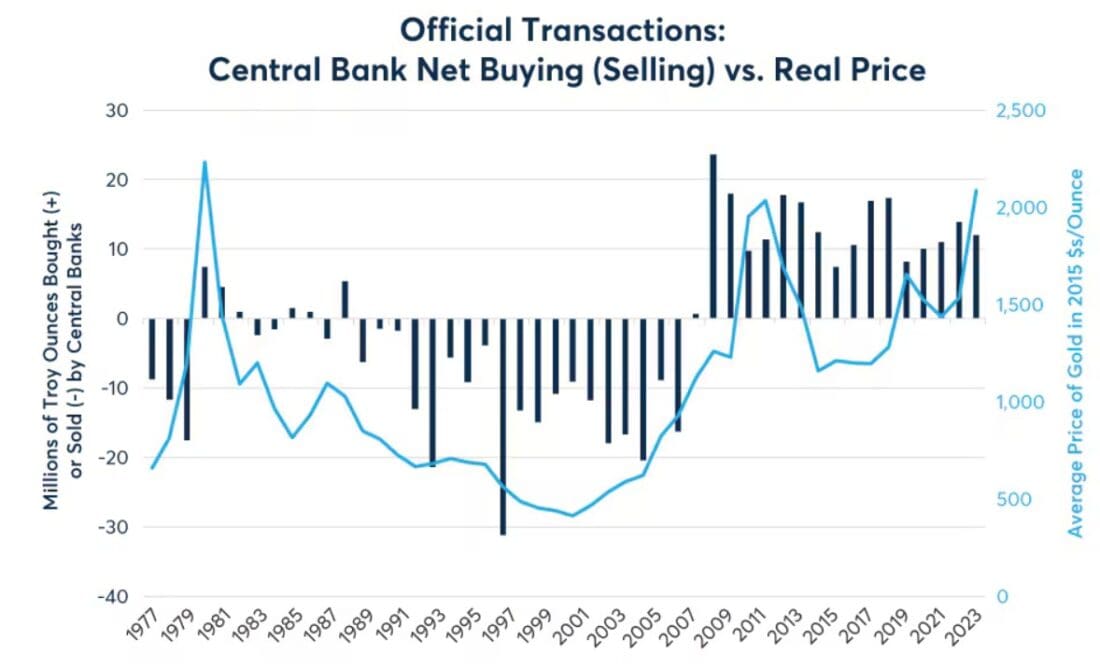

While gold and silver are usually classified as commodities, they are also considered monetary assets. The world’s largest holder of gold is the Federal Reserve (Fed). Moreover, after being net sellers of gold for most of the period from 1982 to 2007, central banks from 2008 onward have been net buyers of gold every year, and their pace of buying appears to have accelerated in 2024 (Figure 8). This tells us two things: first, central banks see gold as a monetary asset; and second, they would prefer to accumulate gold more than to build reserves of other currencies.

Figure 8: Central banks have been net buyers of gold since 2008

Source: CPM Group Gold Yearbook 2024, CME Economic Research Calculations, Bloomberg Professional (CPI INDX) – Past performance is not indicative of future results

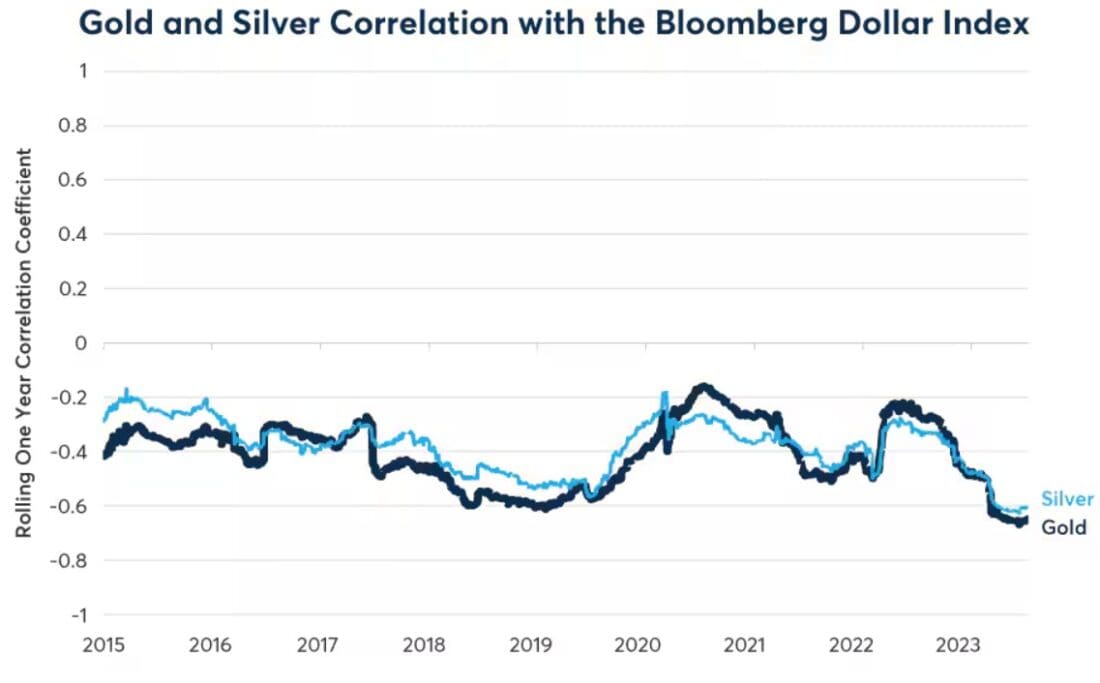

Gold and silver tend to correlate negatively with the U.S. dollar. When the Bloomberg Dollar Index (BBDXY) rises, gold and silver prices tend to fall (Figure 9). Since early October, BBDXY has risen by 6.5% due in part to stronger U.S. economic data and the prospects of potential tariffs. Tariffs might be dollar-bullish, at least in the short run, for three reasons:

- Tariffs raise revenue, which can narrow the budget deficit or be used to fund tax reduction in other areas such as corporate or individual income that could boost productivity growth. Currencies tend to react positively to reduced government budget deficits.

- Increased tariffs could also narrow the U.S. trade deficit by raising the prices of imported goods. Currencies tend to rally when trade deficits shrink.

- Tariffs could also raise consumer prices and lead to fewer rate cuts from the Fed. Currencies tend to outperform when markets shift towards higher interest rate expectations.

Figure 9: Gold and silver have a strong negative correlation to BBDXY, which has been strong recently

Past performance is not indicative of future results

By way of concrete example, in 2018 when the U.S. placed tariffs on many Chinese-made goods, the U.S. dollar (USD) rose by 10% versus the Chinese yuan. Also, any potential changes to sanctions on Russia could impact the USD and demand for gold.

All of these points constitute major volatility risks for precious metals prices in 2025. It’s not clear, which, if any, tariffs will be implemented, and one should not ignore the possibility that other countries responding to any U.S. tariffs by putting up barriers of their own against U.S. exports. Moreover, the outcome of the Russo-Ukrainian war and related sanctions remains highly uncertain.

It’s also worth pointing out that the combination of large budget deficits and falling interest rates could keep a strong bid in precious metals prices in 2025. In the U.S., the budget deficit is running at 7% of GDP. It’s about the same in Italy, and nearly as large as in China, France, Japan, Spain and the UK Moreover, outside of Brazil and Japan, most central banks are cutting rates. The combination of large budget deficits and falling rates could boost the appeal of hard assets like gold, silver and crypto currencies going forward, potentially creating strong trends that are subject to sharp pullbacks. In this environment, the advent of weekly options on gold and silver can also offer traders in these markets greater flexibility for their hedging needs.

Disclosure: CME Group

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account