Originally posted – 24 February 2025 – Europe’s comeback: unleashing the 2025 export advantage

Key Takeaways

- European equities are staging a strong 2025 comeback, fuelled by attractive valuations, robust earnings, and a clearer ECB policy outlook, with key sectors like financials and industrials driving gains.

- Catalysts such as a potential resolution to the Russia-Ukraine conflict, Germany’s fiscal loosening, and underpriced tariff risks are reinforcing Europe’s competitive advantage in global markets.

- European exporters are benefitting from underpriced tariff risks and tailwinds from Chinese stimulus policies.

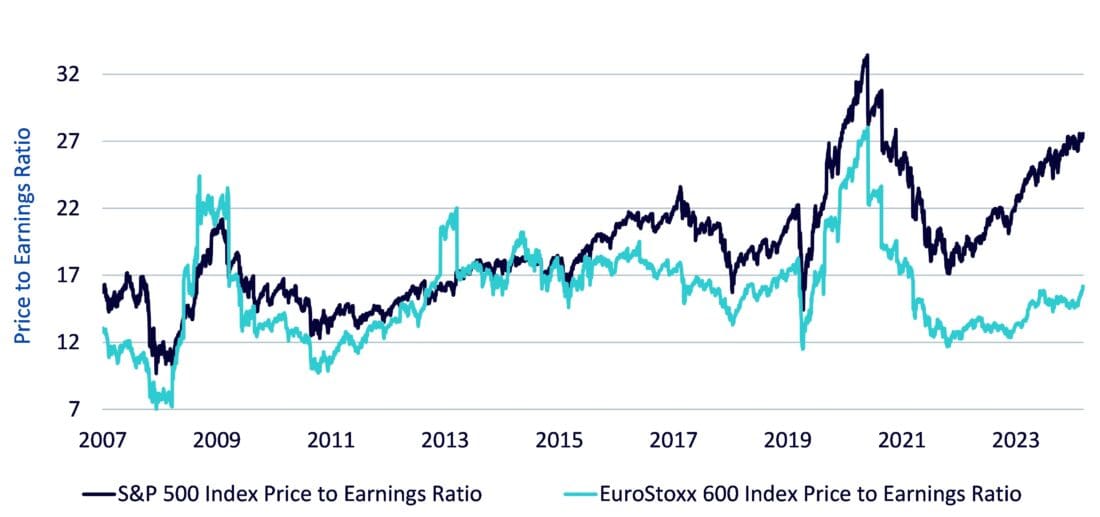

Europe has got off to a flying start in 2025, driven by a combination of attractive valuations, robust corporate earnings and a clearer European Central Bank (ECB) policy outlook. With European stocks trading at significant discounts relative to their US counterparts—often at record-low forward price-to-earnings (P/E) ratios—investors have increasingly turned to Europe for opportunities. This ‘catch-up rally’ is further bolstered by robust performance in key sectors like financials, consumer goods, and industrials, which have not only delivered steady earnings growth but also provided attractive dividend yields.

Figure 1: Europe trading at a significant discount to the US

Source: Bloomberg, WisdomTree, as of 17 February 2025. Historical performance is not an indication of future performance and any investment may go down in value.

Geopolitical catalyst

A deeper dive into the rally reveals several additional catalysts that could sustain the momentum throughout the year. One of the most compelling is the possibility of a resolution to the Russia-Ukraine conflict. Should diplomatic breakthroughs emerge, European markets could benefit from a reduction in geopolitical risk and improved energy supply dynamics. Lower commodity prices and easing inflationary pressures would support earnings across energy-intensive sectors.

Debt brake relief: Germany’s potential loosening opens doors for increased public investment

Another significant catalyst lies in the realm of fiscal policy, specifically the potential loosening of Germany’s debt brake following the upcoming elections. Polls suggest that a coalition government—most likely led by the CDU/CSU and SPD1—will emerge, with a greater willingness to relax rigid fiscal constraints. Proposals under discussion include reclassifying certain government subsidies as “financial transactions” and increasing the permitted structural deficit. These measures could unlock much-needed public investment, fuelling economic growth and corporate earnings. Although any major amendment to the debt brake would require a two-thirds majority in both the Bundestag and Bundesrat, current polls indicate that such a scenario is increasingly plausible.

Exporter advantage from tariff under-pricing

Adding another layer to the rally is the under-pricing of tariff risks, which has given European exporters a distinctive edge in domestic markets. By not fully pricing in the potential impact of US tariffs on European goods, these exporters have been able to maintain competitive pricing and expand market share. The underperformance of the Euro versus the dollar has made European exporters that much cheaper. This under-pricing has been a critical factor behind the stellar performance of many export-oriented sectors, as it helps offset cost pressures and drive revenue growth. Exporters have been able to leverage this pricing advantage, further boosting the overall performance of European equities in 2025.

Chinese stimulus impact

European exporters also stand to benefit from favourable policy initiatives coming from China. As outlined in a recent Politburo announcement on 09 December 2024, China is shifting from incremental support to full-on stimulus mode, with top priorities that include vigorously boosting consumption, improving investment efficiency, and expanding domestic demand3. This bold policy stance is expected to reinvigorate Chinese demand and help end disinflation, thereby providing additional tailwinds for European exporters who benefit from increased demand in China’s vast market.

Conclusion

European equities are being propelled by attractive valuations, robust earnings, supportive monetary policy, and a series of strategic catalysts—from the potential end of the Russia-Ukraine conflict to a more flexible fiscal framework in Germany, along with the competitive boost provided by underpriced tariff risks. Together, these factors make a case for investors to consider European stocks, even as they remain vigilant to the inherent risks in a dynamic geopolitical and economic landscape. While the outlook remains largely positive, it is important for investors to remain mindful of potential risks. Geopolitical uncertainties, lingering trade tensions, and the uneven pace of economic recovery across European countries could all introduce volatility.

1 CDU/CSU = Christian Democratic Union of Germany/Christian Social Union. SPD = Social Democratic Party of Germany.

2 China Central Economic Work Conference (CEWC) as of 16 December 2024.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account