At its core, the battle for Warner Bros. Discovery is less about superheroes, HBO prestige drama, and streaming platforms than about how corporate control is exercised. Paramount Skydance’s $108 billion hostile bid bypasses management and appeals directly to shareholders, while Netflix’s $72 billion board‑approved agreement shows the traditional route through a negotiated agreement.

This bidding war is a live case study in corporate control: one path relies on board authority, the other tests the raw power of shareholder democracy.

Lesson 1: The Mechanics of Hostile Bids

Hostile takeovers are corporate drama at its sharpest. Instead of negotiating with management, the bidder goes straight to shareholders, offering cash or stock at a premium.

If enough investors tender their shares, control shifts without board approval. In some cases, bidders escalate with proxy fights, persuading shareholders to vote in new directors who will back the deal.

Paramount has even launched a “Stronger Hollywood” campaign site to pitch its case: a reminder that hostile bids can be fought as much in the court of public opinion as in the marketplace.

Lesson 2: Financing Coalition

Paramount Skydance’s market value is only about $16 billion, with $3.3 billion in cash on hand last quarter, far short of the $108 billion needed.

The bid rests on the Ellison family’s financial muscle, alongside their trusted partner RedBird Capital, for equity funding.

The coalition extends to Affinity Partners and sovereign wealth funds from Saudi Arabia, Qatar, and Abu Dhabi. Affinity Partners is led by President Trump’s son-in-law Jared Kushner. Both Affinity and the Saudi fund are also backing the proposed takeover of video game giant Electronic Arts, underscoring how the same investors are shaping multiple mega‑deals in media and gaming.

The remainder, roughly $54 billion, will be financed with debt.

Lesson 3: Ownership Structures Matter

Paramount Skydance is publicly listed, but CEO and chairman David Ellison — son of Oracle founder centibillionaire Larry Ellison — holds decisive power. He controls the company through Class A super‑voting shares, giving him full command over strategy and board direction.

Public investors, by contrast, hold unusual Class B shares with zero voting rights. This rare corporate structure highlights how concentrated ownership can enable bold takeover strategies, even when the company’s market value is dwarfed by its ambitions.

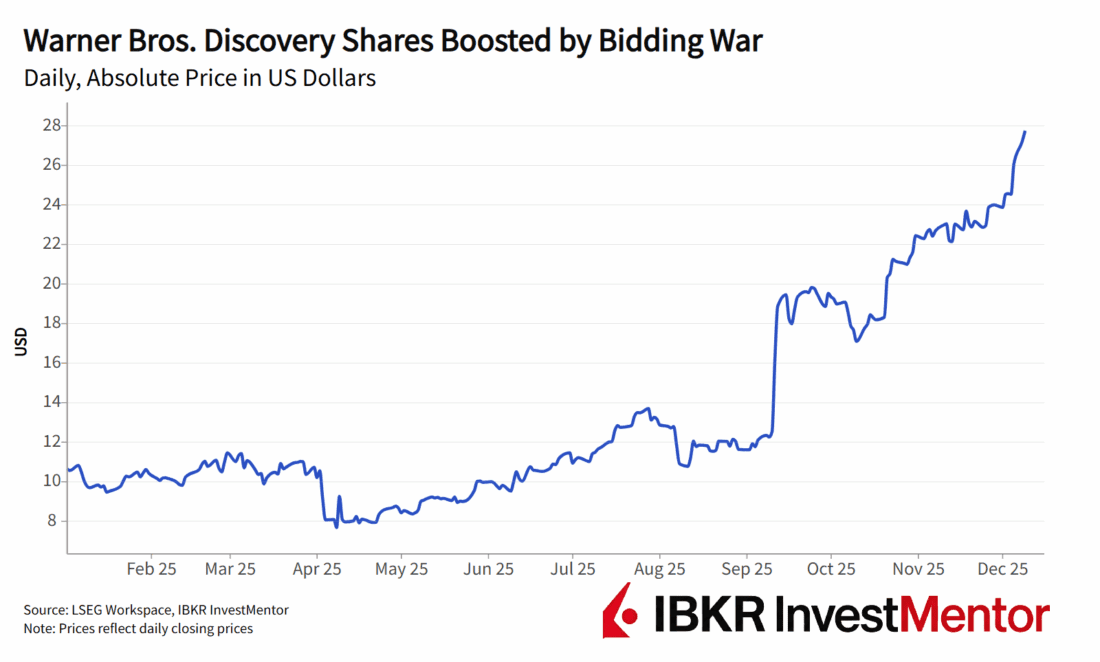

Paramount’s bid offers a whopping 139% premium to the WBD’s undisturbed stock price before the bidders began circling around it in September.

Lesson 4: Regulators Will Have the Final Say

Regardless of who wins, they will ultimately have to convince the antitrust authorities. Global regulators will examine whether consolidation harms competition, movie theaters, consumer prices, or advertiser bargaining power.

Paramount argues Netflix would control 43% of the global streaming market, risking a near‑monopoly. Netflix counters that the relevant comparison is the broader entertainment space, and warns of job cuts if Paramount prevails.

Politics also adds an element of surprise to this deal, as the White House has already signaled wanting to get directly involved in reviewing the deal.

Warner Bros. Discovery faces a $2.8 billion breakup fee if it abandons the already signed agreement with Netflix. Netflix, meanwhile, would have to pay $5.8 billion to WBD if the deal gets blocked by the regulators.

The credits will not roll until the deal has survived the spotlight.

To learn more about investing, download IBKR InvestMentor for jargon-free, interactive lessons and daily explainers on the biggest financial events.

Learn more about InvestMentor

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account