A bear-steepening yield surge is igniting turbulence on Wall Street as investors lift inflation expectations in consideration of price pressure readings from around the world coming in way too hot. The continued blockage along the Strait of Hormuz amidst oil barrels remaining well above $100 is straining the fixed-income complex as there’s no light at the end of the geopolitical tunnel. Bond watchers were hopeful that President Trump’s meeting with Xi Jinping may have calmed the Middle East situation, but a lack of progress on the conflict has folks throwing in their towels as it relates to the possibility for lighter interest rates. Meanwhile, the US Treasury curve is essentially demanding that the Fed hike just as new Chair Kevin Warsh takes the helm. Indeed, there’s now a 50% chance that the central bank will raise by the end of 2026, and a 10% probability of two increases before Christmas. Stocks are plunging as a result, with every sector and subcategory retreating minus energy, as tighter financial conditions suppress risk premiums and make an economic slowdown more likely. Weakening speculative enthusiasms are also hitting non-energy commodities, conversely though, the greenback, volatility protection instruments are catching bids.

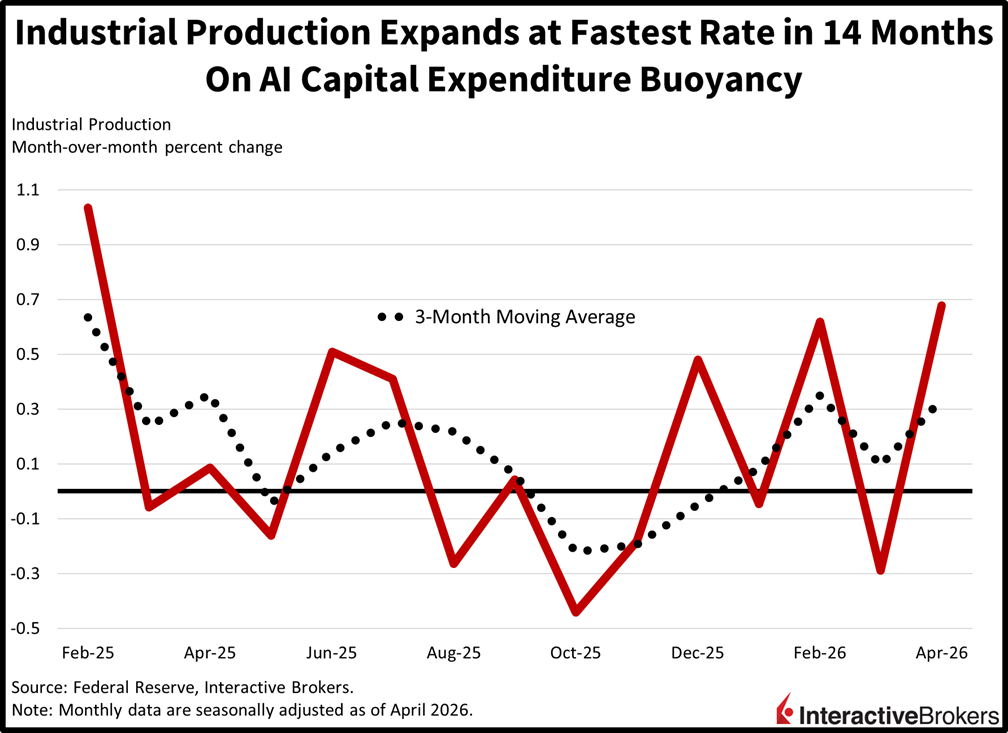

Industry Grows at Fastest Pace in 14 Months

April industrial production grew at the fastest pace in over a year, as robust capital expenditures tied to AI bolstered results. The 0.7% month-over-month (m/m) lift was much stronger than the 0.3% expected and marked a recovery from March’s 0.3% decline. Additionally, the year-over-year (y/y) figure accelerated notably from 0.8% to 1.4%. Among industry groups, utilities and manufacturing grew 1.9% and 0.6% while mining contracted a marginal 0.1% m/m. Across market segments, business equipment, consumer goods and materials saw lifts of 1.5%, 0.9% and 0.5%, while construction was unchanged.

Past performance is not indicative of future results.

Stellar Run Meets Friday Profit Taking

The stellar run in stocks is meeting Friday profit taking as investors decide to curb exposures in light of double-digit year-to-date percentage gains for the Nasdaq 100 and Russell 2000 indices. The risk of much higher yields is a real one, as inflation prints for May and June are poised to come in well above 4%. Meanwhile, the path for a 5-handle Consumer Price Index in August or September is widening substantially, and as a result, a 10-year yield north of 5% is in the cards. Cost pressures sourced from elevated energy charges are beginning to broaden out to the general economy as scarce oil supplies adversely affect food, goods and services, warranting a policy response from central banks while bond vigilantes protest accelerating inflation at the long end. Equity bulls, however, are hoping that President Trump shares some good news on the Middle East situation over the weekend as that could very well calm everyone down, reignite animal spirits and restore market confidence via lighter crude and softer interest rates.

International Roundup

Factory Gate Pressure Intensifies in Japan

Japan gate prices climbed 2.3% m/m and 4.9% y/y in April, blowing past the economist consensus estimates of 0.7% and 3% while accelerating significantly from the m/m and y/y climbs of 1% and 2.9% in March, according to the Bank of Japan. The gauge, which is also called the Corporate Goods Price Index, showed that import prices were up 4.9% m/m while exporters fetched 3.3% more for their products than during March. Within the headline print, petroleum and coal products soared 11.8% m/m. Electric power, gas and water, scrap and waste, nonferrous metals, chemicals and related products, and plastic products were also noteworthy with gains of 8.4%, 7.9%, 6.1%, 2.7% and 2.5%.

South Korea Export Growth Outpaces Imports

The value of South Korea’s exports and imports jumped 50.2% and 16.8% y/y in April with artificial intelligence demand causing shipments of computers, electronic and optical equipment to foreign lands to surge 141.3%, according to the Bank of Korea. The agriculture, forestry and marine products group, furthermore, enjoyed a 50.4% y/y increase in demand from beyond the country’s borders. The growth of imports was led by the computer, electronic and optical equipment category jumping by 37.8% y/y. Other noteworthy categories included basic mineral products and the group consisting of machinery and equipment, with growth of 25.4% and 22.8%.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account