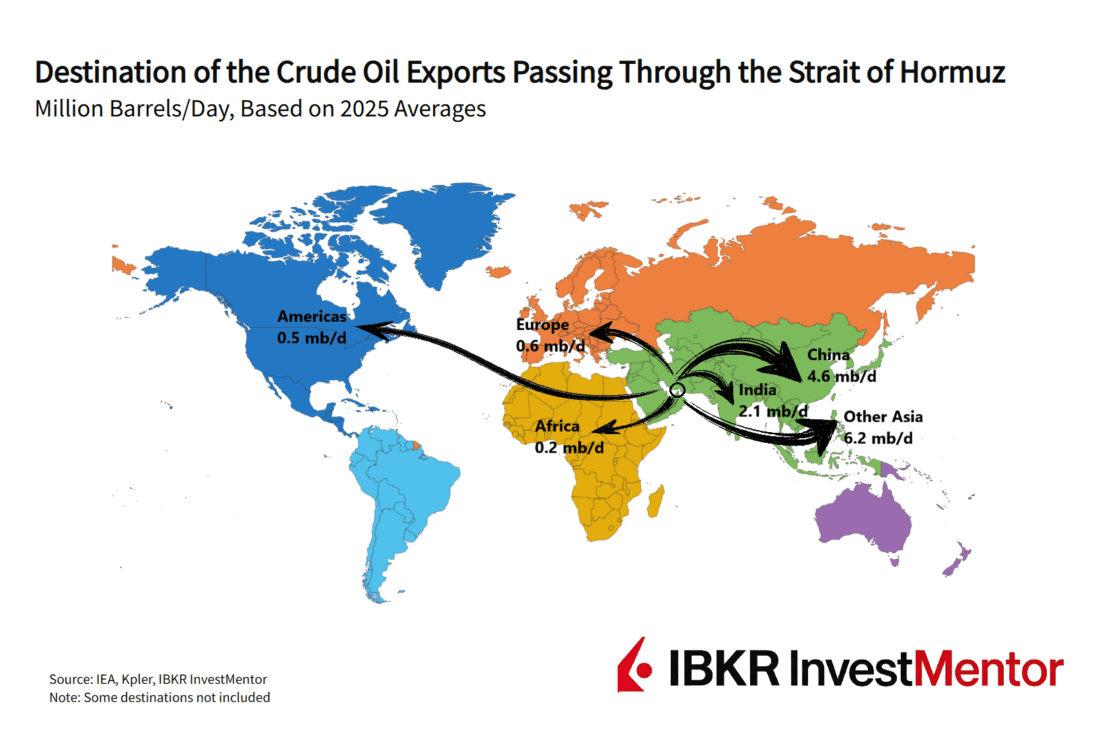

More than 80% of the crude oil that passes through the Strait of Hormuz ends up in Asian markets. When conflict in the Middle East disrupts flows or raises shipping risks, Asian economies feel it first.

Europe and the US are also hit by crude prices that are now trading 50-60% above pre-war levels, but they rely less directly on oil from the Gulf. For many Asian countries, the concern is not just price, but delivery. Large emergency reserves offer a buffer, yet governments across the region are already rolling out measures to cut oil and gas consumption.

Fuel costs are climbing. Currencies and stock markets are under pressure. Policymakers are being pushed into uncomfortable trade‑offs. Asia provides an early read on how higher energy costs move through inflation, markets, and policy. What happens in the region matters well beyond it.

Japan Shows How Oil Shocks Travel

Japan offers a clear example of how an oil shock filters through an economy. The country imports about 95% of its oil from the Middle East, leaving it highly exposed when the Gulf supply is disrupted.

In some ways, Japan was well prepared for the disruption. At the end of 2025, it held oil reserves covering more than eight months of consumption. Those stockpiles help manage short‑term shortages but Japan is also entering this crisis with stretched public finances and fragile investor sentiment. Markets have been wary of Prime Minister Sanae Takaichi stimulus plans, with government bond yields at the highest levels in decades and policymakers openly talking about interventions to support the weak yen. Rising energy costs fuel these concerns.

Oil is priced in dollars. When the Japanese yen weakens, imported fuel becomes more expensive in local terms, even if global oil prices do not move much. Higher fuel and electricity costs push up prices across transport, food, and household bills. The yen recently traded near 160 to the dollar, close to its weakest level in about 40 years.

Past performance is not indicative of future results.

China Is the Oil Shock Prepper

China is also dependent on oil imports, with very little domestic production despite its vast landmass. It is the world’s largest importer of oil that passes through the Strait of Hormuz, yet it enters this shock from a stronger position than most of Asia.

It has systematically tried to diversify its energy mix and reduce dependence on crude oil. The rapid take‑up of electric vehicles has lowered fuel demand, cutting oil imports just as prices rise. Electricity generation relies mainly on domestic coal and a fast‑growing base of renewables, limiting spillovers into power costs. Large oil stockpiles, bolstered greatly in recent years, and pipeline links to Russia and Central Asia add further flexibility.

Supply is also spread out. China buys oil from many countries rather than depending heavily on a few Gulf exporters — although the closure of the strait still hurts.

To mitigate the impact, China has been willing to negotiate with Iran. Some of its ships have now managed to pass through the strait, paying toll fees to the Iranian government. Iran’s parliament recently approved a plan to enforce tolls, with some ships reportedly charged $2 million for a safe passage.

In normal times, around 140 vessels pass through the strait daily, making toll fees potentially a lucrative revenue source for Iran, even if the prices come down during peacetime.

But despite the new toll fees, marine traffic trackers show that most of the ships still avoid the strait, with only a few vessels passing daily.

Cutting Demand Enters the Picture

For most Asian economies, the pressure shows up faster and with fewer shock absorbers. Many countries rely heavily on imported energy but lack China’s diversification or Japan’s huge stockpiles.

As oil prices climb, cutting demand has moved back onto the policy agenda. The International Energy Agency is urging countries around the world to cut energy use using a mix of old and new tools. Some, such as lower speed limits, were widely used during the oil shocks of the 1970s. Others, including working from home, reflect how modern economies operate.

Across Asia, governments have already acted.

The Philippines declared a national energy emergency, cutting work weeks and limiting official vehicle use. South Korea reintroduced public‑sector car restrictions, with discussion about expanding them to the general population. Pakistan closed schools temporarily and reduced speed limits. Thailand ordered civil servants to work from home. Bangladesh extended holiday periods. Myanmar introduced work‑from‑home days and alternate driving schedules.

These measures show how quickly energy shocks reach daily life. Air conditioning is turned a few notches down. Dress codes are ditched to accommodate cooler clothing. Just when companies were calling employees back to the office en masse, WFH makes a big comeback.

Softening the Blow to Consumers

But at the same time, there’s a second set of measures to stop energy prices rising too much: fuel tax cuts, energy price caps, and subsidies. These are meant to soften the blow on households and businesses, but they also keep the demand high. Finding the right balance is tricky, and often politically costly.

Asia is testing in real time how to survive the oil shock, which the International Energy Agency considers larger than the 1970s shocks combined. Just like during the pandemic, how Asia manages that test will likely influence policy response around the world.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account