Last week, we taped an IBKR Podcast entitled “Socially Acceptable Volatility Strikes Again.” In light of today’s activity, the topic proved to be quite timely, even if it meant that I couldn’t re-use that title this morning. Today’s 2.5%-3% jumps in key equity indices are a huge bout of “socially acceptable volatility” amid a global sigh of relief. Interestingly, today’s move is quite similar to what the options market was already expecting.

Yesterday, we examined the pricing dynamics in S&P 500 (SPX) options and noted that there was a persistent bid for upside calls even as the President threatened that “a whole civilization would die tonight.” The memory of last year’s post-“Liberation Day” rally – almost exactly one year ago – is still fresh in investors’ minds. One of the comments that we made yesterday seems quite prescient today:

Seemingly no one was willing to speculate on an upward move; now they are willing to pay up for calls that hedge against a significant rally, and the peak probability for those options prices in a bounce to 6750.

Today’s rally is a combination of reflex and relief. Obviously, the world is relieved that the threatened attack was averted, so the rally in stocks and the plunge in crude are quite understandable. But from a macro viewpoint, things are better, but not yet back to where they were beforehand. Although the worst of the crisis seems to be behind us, many stock traders are reacting as though it is fully in the rear-view mirror. In contrast, commodity and fixed income traders are pricing in improved circumstances, not a full reversion to the norm.

For example, while the 15% drop in crude futures prices eases perceptions of future inflation, we only see modest improvements in bond yields and rate cut expectations. US Treasury yields are down, but only by about 1-2 basis points. Fed Funds futures are pricing in the best chances for a rate cut that we have seen in weeks, but they are currently anticipating a roughly 35% chance for a 25 bp cut in 2026. Bear in mind that 2 full cuts and a 50% chance for a third were priced in prior to the hostilities. Fixed income traders apparently have a more sober view about prospects for improving inflation than stock traders might.

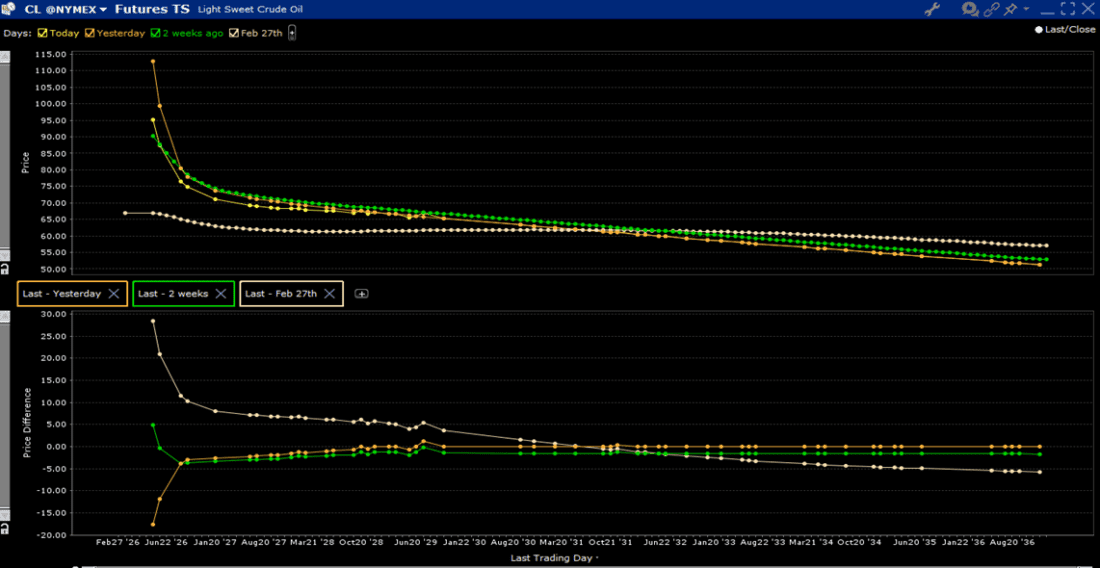

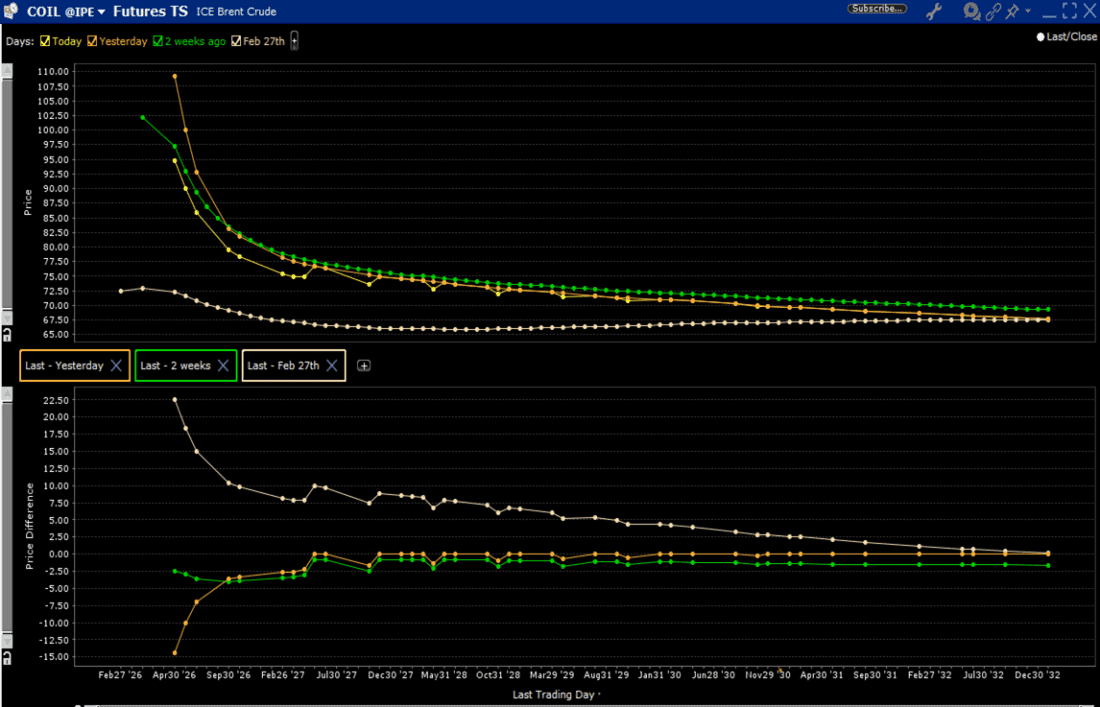

Similarly, while today’s plunge in oil prices is highly significant, crude futures remain well above the levels that prevailed prior to February 28th. When we look at futures for delivery over the next few months, they are indeed about $2.50 below their recent highs, but still about $7-$10 above the prices that prevailed prior to the hostilities. Oil traders are more sanguine today than they were recently, but remain cautious about the prospects for medium-term supply.

Term Structure of WTI Futures

Source: Interactive Brokers, past performance is not indicative of future returns.

Term Structure of Brent Futures

Source: Interactive Brokers, past performance is not indicative of future returns.

I’ll leave it to others to decide how to term the decision to avert major hostilities – TACO, brinksmanship, skillful negotiations, etc. How we got here is less relevant for investors than where we are now and what might come next. We got a two-week break from an extraordinarily nerve-wracking situation, and we should be thankful for that. But we already hear back-and-forth chatter about different terms for a lasting outcome, and it will take some time for the backlog of tankers to emerge from the Persian Gulf – with or without threatened tolls for passage. Enjoy the relaxation of hostilities and the socially acceptable volatility, but as we often counsel during times of geopolitical stress, listen to the messages from commodity and fixed income markets. They are indeed optimistic – as they should be – but I’m not hearing an “all clear” from them.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Options (with multiple legs)

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Disclosure: Bonds

As with all investments, your capital is at risk.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account