Markets are taking a breather following strong rallies in equities and fixed income alike as participants keep their eyes and ears on taxation and trade. The GOP tax legislation is working its way through the Senate for a potential approval this afternoon before it heads back to the lower chamber for confirmation. But republican party representatives in tight midterm races are concerned about the deep Medicaid cuts while the hardliners of the Freedom caucus are upset that the bill isn’t austere enough. Meanwhile, cross-border commerce developments were favorable in aggregate, as the EU seems set to accept a 10% tariff on its exports across the Atlantic; however, the Commander in Chief has expressed frustration with Tokyo and suggested the possibility of tightening the screws further on the Pacific nation. The domestic economic calendar was mixed, but downbeat overall, as the rate-sensitive manufacturing and real estate sectors remained burdened by heavy financing costs that are significantly hampering transaction volumes. Conversely, job openings rose to their highest level since November, although the sharp gain was driven by the leisure and hospitality sector, which has been suffering from a lack of workers due in part to immigration restrictiveness.

Trading is Bifurcated

Stocks are bifurcated in the session from an index perspective, with the cyclically oriented Dow Jones Industrial and Russell 2000 benchmarks advancing while the S&P 500 and Nasdaq 100 retreat. Breadth is strongly positive with just technology and communication services reversing today while the other nine segments climb. Furthermore, investors are increasing their commodity exposures minus natural gas and lumber, and they’re also purchasing greenback wagers, volatility protection instruments and forecast contracts. In contrast, traders are selling Treasuries as the yield curve shifts north in bear flattening fashion led by the short end with a big beat on JOLTS alongside remarks from Chair Powell reducing expectations for a Fed rate cut later this month. Additionally, bitcoin is experiencing fading interest above the 100k area.

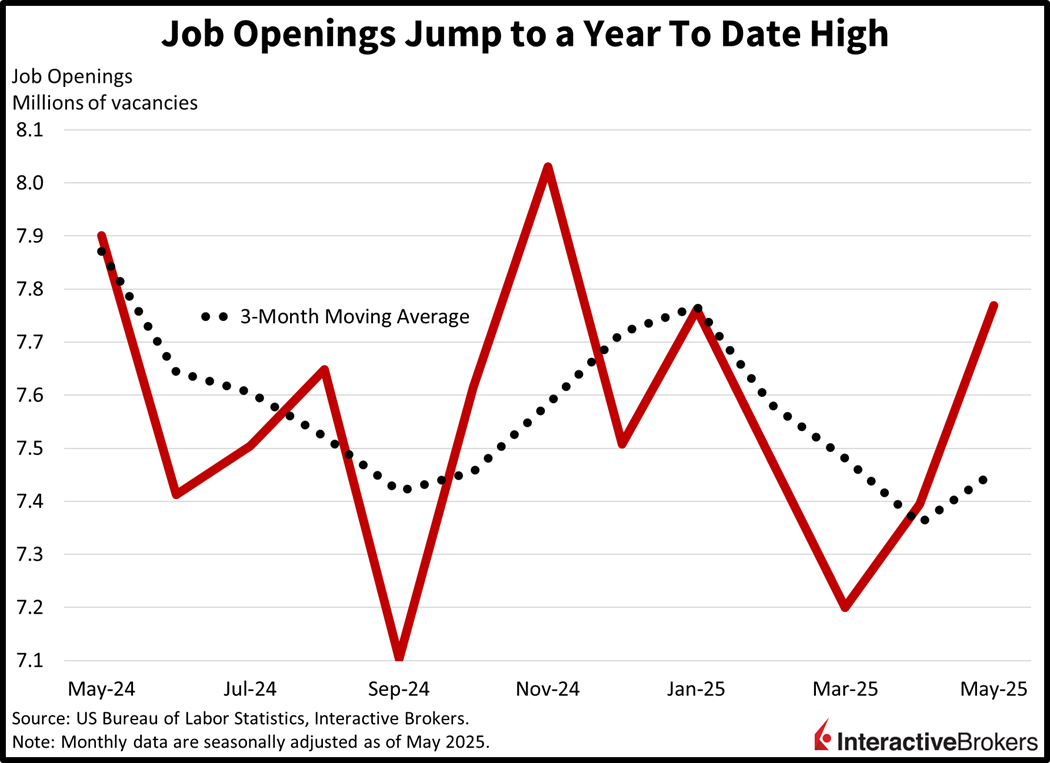

Labor Shortage in Accommodation and Food Services Persists

Job openings surged to a fresh year-to-date high as 374,000 additional for-hire signs were posted across the nation in May. But a whopping 314,000 of those came from the accommodation/food services sub sector, which has been struggling to retain workers due to immigration restrictiveness. No other segment added over 100,000 vacancies, although finance/insurance, transportation/warehousing/utilities, health care/social assistance were amongst the leaders below the six-figure mark. The retail trade, federal government and arts/entertainment/recreation components trimmed vacancies by 71,000, 39,000 and 37,000. The 7.769 million headline number exceeded the median estimate of 7.3 million and April’s upwardly revised 7.395 million.

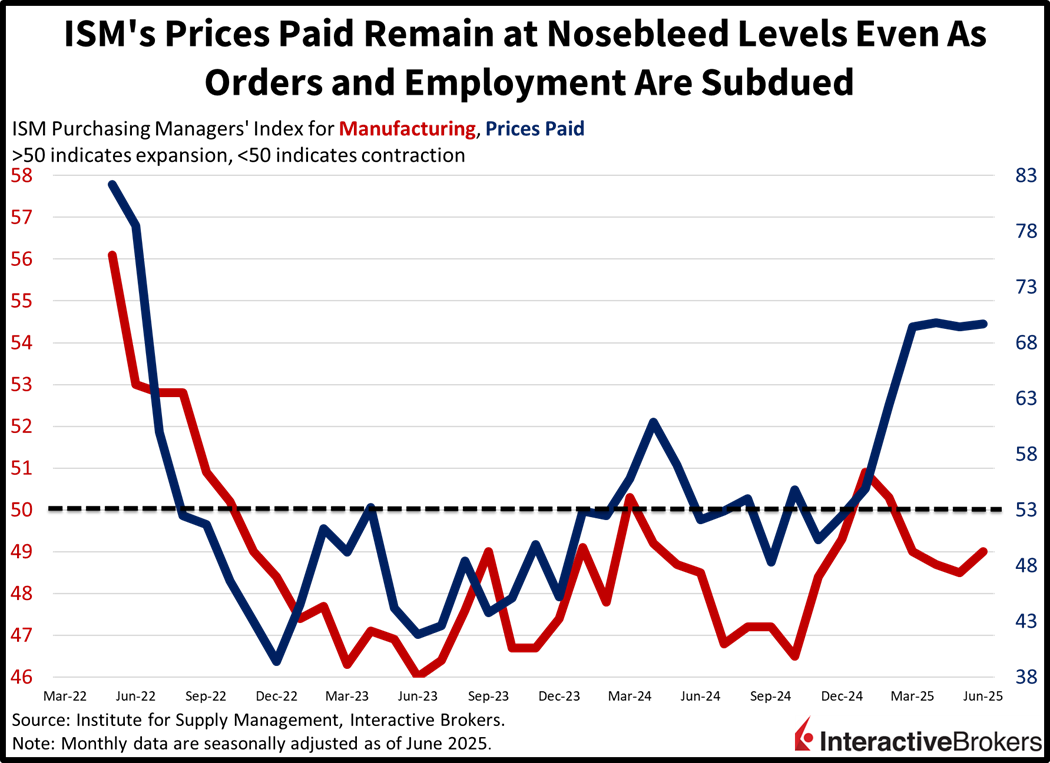

US Manufacturing Contraction Extends to Fourth Month

Manufacturing conditions contracted for the fourth-consecutive month in June as weak transaction momentum drove headcount reductions. The Institute for Supply Management’s Purchasing Managers’ Index (PMI) print of 49 was an improvement from May’s 48.5 and ahead of the 48.8 median estimate, but still below the expansion-contraction threshold of 50. Despite orders and employment softening, with scores of 46.4 and 45, factory production and prices expanded at levels of 50.3 and 69.7. Indeed, the inflation aspect of the report has been signaling the potential for higher cost pressures in the coming months. But goods continue to comprise a reduced share of the domestic economy year after year and the category’s influence on the overall inflation picture may prove light, as services have grown consistently over the decades when excluding the pandemic, lock-down era.

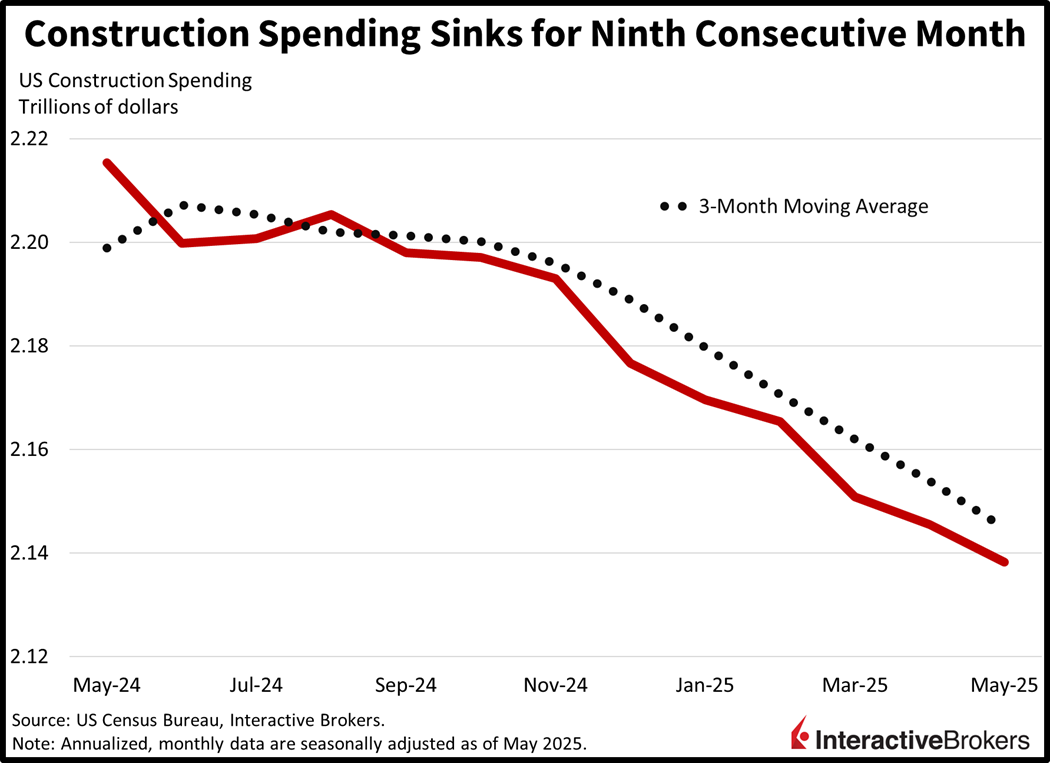

Construction Continued to Languish in May

Construction spending fell for a ninth-consecutive month in May as a lack of new-single family residence developments hampered performance. The 0.3% month-over-month (m/m) decline was slightly worse than the -0.2% expected, which would’ve been unchanged from April. Despite a flat result for fresh builds of multi-family units, the 1.8% m/m drop in singles led to a 0.5% slip in the overall residential category. Pricey properties and heavy borrowing charges continue to weigh on real estate affordability, as inventories have grown meaningfully but have been unable to counter valuation and financing challenges. Additionally, the religious, lodging, commercial, water supply, road and power segments also weighed on results. Conversely, projects focusing on public safety, amusement/recreation, conservation/development and health care served to offset some of the weakness.

Taxation, Trade Progress, Would Outweigh Econ Data

Traders and economists will be focusing on developments from Washington at all hours of the day and night, but economic data scheduled for tomorrow morning include the ADP jobs report. Interestingly, the Street expects ADP to reflect an acceleration in hiring while projecting the government’s print, released the next day, to signal a deceleration. But because rates have sunk significantly since the beginning of the year, strong showings on both fronts are likely to add further fuel to the stock market rally despite heavier yields, as it’ll provide evidence that the expansion is ongoing and will serve to bolster medium-term earnings expectations. Numbers that are too soft may lead to selling pressure in equities, as investors would begin to dial up slowdown fears. A sweet-spot result that is in-line with forecasts can also be well interpreted by participants. In conclusion, however, progress on taxation and trade, shall it occur, would outweigh this week’s activity updates from the calendar.

International Roundup

China’s Manufacturing Enters Expansion: Caixin

China’s goods production moved into expansion in June with the Caixin Manufacturing Purchasing Managers’ Index increasing from 48.3 to 50.4, which exceeded the economist consensus estimate of 49.2. A reading of 50 is the border between contraction and expansion and June’s result depicts the eighth month out of the past nine in which conditions advanced. For the most recent result, the PMI climbed due to more plentiful new orders that supported a jump in production. The increase in demand was only marginal as exports declined for the third consecutive month, albeit at a slower pace than in May. Ramping up promotions helped drive the favorable change in orders. Also last month, business confidence weakened and companies were cautious when hiring workers. The government version of the PMI, released yesterday, depicted the manufacturing sector in contraction.

Japan’s Manufacturing Picks Up

Japan’s large manufacturers experienced improved conditions during the second quarter of this year with the Bank of Japan’s Tankan Survey of business sentiment climbing from 12 to 13 and surpassing the consensus forecast of 12 from economists. The outlook for the business landscape was unchanged at 12 but substantially above the estimate for 9. Large companies also increased capital expenditures. Small companies didn’t follow suit, with the category’s Tankan Index descending from 2 to 1. In the non-manufacturing segments, the large company score dropped from 35 5o 34, consistent with the forecast while the small company gauge was unchanged at 9.

South Korea Trade Surplus Expands

South Korea’s trade balance climbed from $6.9 billion in May to $9 billion last month, according to preliminary estimates. The result, which exceeded the estimate of $8 billion, was driven by a 4.3% y/y jump in exports, which while strengthening from the 1.3% decline in May was below the forecast for a 4.7% expansion. Imports increased 3.3% y/y, less than half the forecast for 6.9% but much higher than May’s 5.3% drop.

Europe Inflation Strengthens Marginally

Prices in the euro area climbed 0.3% m/m and 2% y/y in June, accelerating from the flat m/m result and 1.9% print for May, according to the flash Consumer Price Index from Eurostat. For the y/y metric, June’s performance matched the economist consensus prediction. The Core gauge, which excludes various items with volatile prices, climbed 0.4% m/m after a goose egg in May and 2.3% y/y, which was unchanged and consistent with the forecast. The services sector, with an estimated rate of 0.7% m/m, experienced the strongest price pressure while the non-energy industrial goods category sank 0.2%.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account