- Wall Street megamergers have not hit the tape as the second quarter comes to a close

- Animal spirits have been kept at bay, but there are indications that the M&A tide could turn soon

- Many small deals have done through, including ones from overseas, and an active calendar of corporate shareholder meetings could offer fresh insights into capital plans

Another pair of IPO gangbusters played out last week. On the heels of the outright fervor that came with CoreWeave (CRWV) and Circle (CRCL) earlier in Q2, shares of Voyager Technologies (VOYG) soared by 82% on their first day of trading. The space- and defense-technology company saw its stock rise by triple digits (percent) intraday last Wednesday—investors were clearly excited about the firm’s niche.

Voyager partners with firms like Airbus, Mitsubishi, and Palantir (PLTR) in low-orbit endeavors, and with Aerospace & Defense being among this year’s top-performing industry groups, it’s easy to see why shares lit up screens early on.1

A Spate of Successful Equity Launches

While the total IPO count is still low, the window seems cracked open. Following Voyager’s stock taking flight mid-week, Chime Financial (CHYM) made its much-anticipated debut, raising $864 million after pricing above its initial estimated range.2 CHYM was music to the bulls’ ears, surging 39% on Thursday.

Brokerage platform eToro (ETOR)3 and virtual physical-therapy company Hinge Health (HNGE)4 are other notable go-public stories in 2025, raising $310 million and $864 million, respectively, both of which priced above their anticipated ranges.

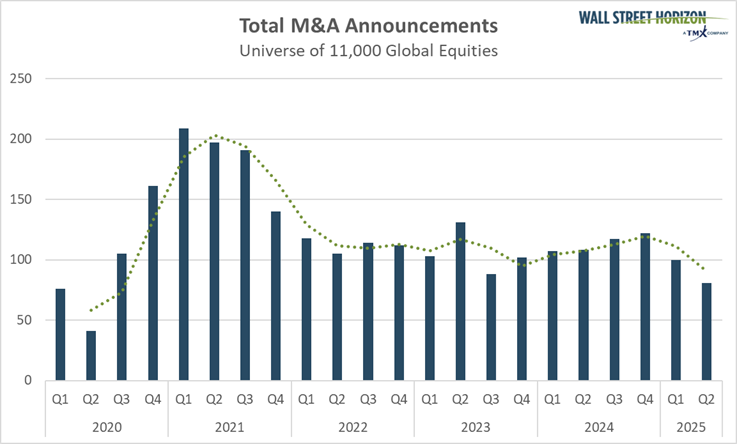

So, animal spirits are alive and well, right? Not so fast. According to Wall Street Horizon’s data, dealmaking numbers remain depressed. Total M&A announcements are merely flat on a year-on-year basis, continuing a trend that began some three years ago, after the capital markets boom of late 2020 and throughout 2021.

Still-Sluggish M&A Trends Heading into 2H 2025

Source: Wall Street Horizon

The hope was that a more favorable administration in the White House and a business-friendly Congress would get the ball rolling with looser regulations, fueling corporate decision-makers to shake hands and ink agreements.

That bullish backdrop has not panned out. Instead, tariffs make the macro environment uncertain, and CEOs and CFOs are apparently unwilling to strike deals. Still, with massive rallies in some recent IPO stocks, bankers’ hopes may just be rekindled.

The Deals Are There, Just on the Small Side

It’s not a total M&A malaise, though. 2025 has brought about a rash of smaller buyouts valued at under a few billion dollars. In the first quarter, PepsiCo (PEP) agreed to buy prebiotic soda brand Poppi for $1.6 billion. In the mortgage space, Rocket Cos. (RKT) purchased Redfin (RDFN) for $1.75 billion.

Then, just last month, retailer Dick’s Sporting Goods (DKS) scooped up Foot Locker (FL) in a $2.4 billion cash and debt transaction. The shoe space is indeed kicking up activity—recall in early May that private equity firm 3G Capital agreed to buy Skechers (SKX) for $9.4 billion. In the tech space and during the throes of earnings season, Salesforce (CRM) struck an $8 billion deal to purchase Informatica (INFA), bolstering its AI capabilities.

To close out Q2, other deals have caught investors’ attention, with the most notable being Brown & Brown’s (BRO) $9.8 billion acquisition of Accession Risk Management. In the Health Care sector, BioNTech (BNTX) expanded its portfolio with the acquisition of CureVac (CVAC), a $1.25 billion equity deal, marking the end of a decades-long rivalry. Overseas, luxury goods maker Kering recently acquired Lenti, an Italian eyewear manufacturer.5

Macro Jitters Lingering, Keeping Purse Strings Tight

Are these the blockbuster megamergers everyone longed for a year ago? Certainly not, but it does prove that the environment can be conducive to risk-taking under the right circumstances. Moreover, with peak tariff fear hopefully in the rearview mirror, at least according to the Economic Policy Uncertainty Index, the back half of 2025 might just feature an M&A rebirth.6

Along with cooling trade-war concerns, a more upbeat outlook on the economy would likely spur deals. We’ve seen strategists reduce their recession forecasts, and online prediction markets suggest a less than one-in-three chance of a two-quarter US economic contraction this year.7

More confidence at the macro level could help boost the appeal of buyouts and partnerships. And with central banks cutting interest rates at a fast clip (the US Federal Reserve notwithstanding), an easing of global monetary policy may make borrowing cheaper, enabling more leveraged deals and refinancing. Citi’s head of banking expects more private-public “get-togethers,” which may offer a twist on the longed-for M&A upcycle.8

End-of-Season Shareholder Meetings Could be the Tell on M&A

The second quarter’s final few trading days might actually present fresh breadcrumbs on the M&A pipelines heading into Q3. Ahead of Independence Day in the US, there’s an active slate of shareholder meetings scheduled.

Such events bring together stakeholders, and management teams present their strategic initiatives, which may include hints at key investments, such as M&A. Our data reveal that more than 1,800 Annual General Meetings will take place or have already occurred this month.

Shareholder Meeting Volume Remains High Through June

Source: Wall Street Horizon

If you’re looking for clues on overall C-suite vibes, you might want to monitor The Conference Board’s Measure of CEO Confidence, which plunged in the second quarter to its lowest level since Q4 2022—a time when recession fears were extremely high. It was the largest quarter-on-quarter decline in the survey’s history, which dates back to 1976.9 It’s reasonable to expect a recovery in the next quarterly update in August, and if such a rebound comes to pass, then it may signal a greater collective risk appetite.

The Bottom Line

Dealmaking isn’t dead. There has been a steady diet of small to medium-sized mergers and acquisitions, but an outright M&A bonanza has simply not materialized. Global activity is also not all that bad, with significant corporate moves having been inked this quarter in Europe and Asia. But with an emerging IPO wave sweeping Wall Street, macro conditions may be shifting in favor of larger M&A transactions in the second half.

—

Originally Posted on June 18, 2025 – M&A Watch: A String of Hot IPOs Could Spark Second-Half Dealmaking

Footnotes

- Voyager Technologies Rises in Debut, Signaling Improving IPO Market, The Wall Street Journal, Josh Beckerman, June 11, 2025, https://www.wsj.com

- Digital bank Chime debuts advance wage product ahead of anticipated IPO, Reuters, Hannah Lang, May 15, 2024, https://www.reuters.com

- Stock trading app eToro pops 29% in Nasdaq debut after pricing IPO above expected range, CNBC, Samantha Subin, May 14, 2025, https://www.cnbc.com

- Hinge Health prices IPO at $32, the top end of expected range, CNBC, Ashley Capoot, May 21, 2025, https://www.cnbc.com

- Kering Buys Italian Manufacturer Lenti in Eyewear Push, The Wall Street Journal, Andrea Figueras, June 10, 2025, https://www.wsj.com

- Economic Policy Uncertainty Index for United States, Federal Reserve Bank of St. Louis, June 17, 2025, https://fred.stlouisfed.org/series/USEPUINDXD

- Recession this year?, Kalshi, June 17, 2025, https://kalshi.com

- Citi expects banking fees, trading revenue to climb despite US tariff “anxiety”, Reuters, Tatiana Bautzer, Arasu Kannagi Basil, June 10, 2025, https://www.reuters.com

- CEO Confidence Declined Significantly in Q2 2025, The Conference Board, May 29, 2025, https://www.conference-board.org

Copyright © 2025 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon’s prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account