With rising uncertainty on their radar, investors seek to make their portfolios more resilient. They see active investment management as key to the solution.

As investors around the world acknowledge significant risks in 2025 and beyond, a large majority (75%) also believe actively managed strategies offer value in current markets. An even bigger proportion – four out of five – say they will increase ther investment in active strategies over the coming 12 months

Schroders Global Investor Insights Survey, which polled the attitudes of almost 1,000 professional investors from around the world, captured the shift in market sentiment which occurred in the first half of 2025 triggered in large part by US trade policy announcements.

Read the full results of Schroders Global Investor Insights Survey 2025

The survey was undertaken from mid-April, a fortnight after President’s Trump’s so-called “Liberation Day”, on which initial US tariff policies were declared. Markets fell sharply in response.

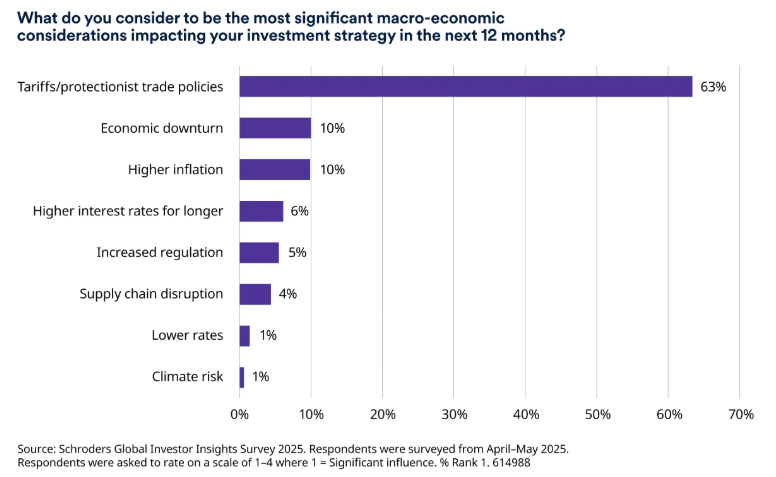

Global trade policy ranks as investors’ primary concern, but economic growth and interest rates are also on the radar

Investors were asked to rate their greatest concerns on a scale of one to four. The vast majority (63%) cited US trade and tariff policy as their chief worry.

However, economic performance, inflation and higher interest rates also featured. After tariffs, the next three areas of concern – economic downturn, higher inflation and higher interest rates – were broadly equal in ranking.

This ties in with another major source of financial market volatility during the first half of 2025: questions over the sustainability of national debt for major global economies including the US, Japan and other G7 countries.

Higher interest rates are pushing up the debt-servicing costs of the world’s biggest economies. Weaker economic growth would likely worsen this position. Bond markets have experienced volatility as a result, and the survey findings suggest investors anticipate more related uncertainty ahead.

When asked to rank their assessment of volatility today against previous market shocks, one in four respondents said they expect greater volatility in the coming 12 months compared to both the COVID-19 epidemic and the global financial crisis of 2008.

Past performance is not indicative of future results

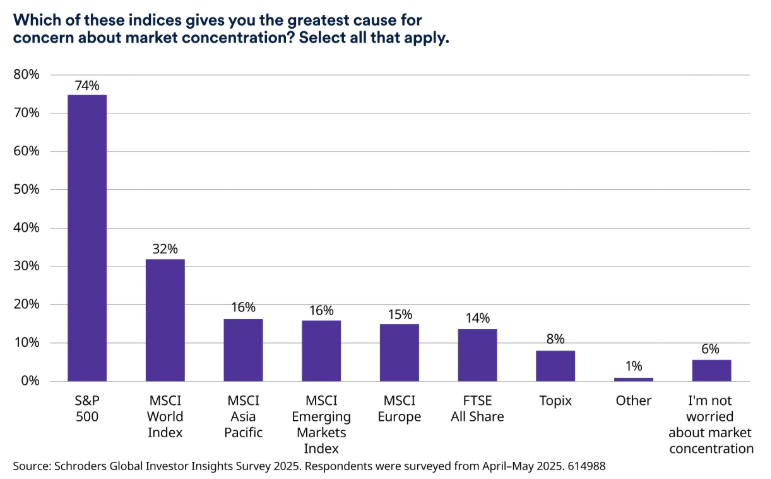

Volatility has brought home the danger of market concentration

In public equities, the volatility sparked by US tariff announcements in April was an unwelcome reminder that markets had become increasingly concentrated around US equities, and around giant US tech companies especially. By the start of this year global indices, such as the MSCI World, comprised over 70% US stocks.

So when asked which indices posed greatest concentration risk, three quarters of investors (74%) cited the US S&P500 index. The global MSCI World index was the next greatest cause for concern, likely due to its extreme US tilt.

Past performance is not indicative of future results

In the face of these risk factors, investors want to make portfolios more resilient

Given the above volatility and the risks perceived by investors, achieving “portfolio resilience” was the goal of the majority of investors (55%), ahead of return generation and income.

“Portfolio resilience” is not to be confused with risk aversion. A majority of investors (62%) are maintaining or increasing their risk appetite in the current environment. This suggests that many see opportunities as well as risk within current volatility.

Portfolio resilience is associated with active investment strategies and a mix of public market and private market assets

Four in five investors say they are more likely to invest more into actively-managed strategies in the coming 12 months. This is linked to other findings where investors see active management as better suited to successfully navigating a more complex period in markets than a passive index-tracking approach.

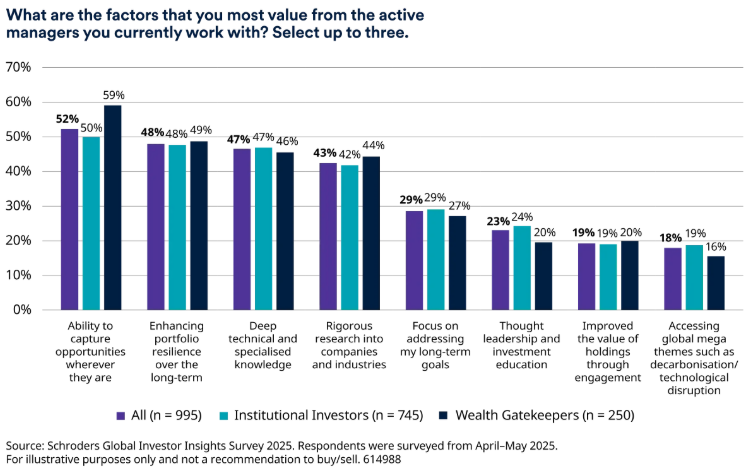

When asked to identify which attributes of active management held the greatest appeal, respondents cited a range of factors, first of which was the ability to capture returns wherever they arise. Achieveing portfolio resilience was the second most valued attribute.

Active management was also seen to bring “deep specialist knowledge”.

Johanna Kyrklund, Schroders’ Group CIO, said: “The wider backdrop is that financial markets are still adjusting back to structurally higher interest rates, made painful in many cases by high levels of debt. This is raising questions about future market trends and the value of passive approaches in a period of greater uncertainty.”

Past performance is not indicative of future results

While the high level of confidence in actively-managed investments was one of the stand-out themes of this year’s survey, so was the high degree of interest in using a mix of both public and private assets.

When asked which two asset classes they would use to access the best return opportunities, 46% cited public equities and 45% cited private equities. Interestingly, the third asset class cited here (by 40%) was another private market category – private debt and credit alternatives (PDCA).

Again, when it came to generating income, PDCA was a priority, with over 40% of both institutional investors and wealth gatekeepers looking to these assets to meet their income needs. High yielding publicly-traded equities and public-traded bonds came a close second and third.

“The ability to access diversifying and flexible income through the wide universe of securitised and asset-backed finance provides a valuable extension of the fixed income toolkit for investors,” said Michelle Russell-Dowe, Schroders Capital’s Co-Head, Private Debt and Credit Alternatives.

Read the full results of Schroders Global Investor Insights Survey 2025

—

Originally Posted on June 11, 2025 – Investors see the value of active management as volatility intensifies

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Research

The availability of research providers may differ depending on your location. Much of the tools, information and services accessible through research tools are prepared and offered by independent third-party providers and not by Interactive Brokers. Information about a third-party provider provided on market research pages is NOT a recommendation of that provider by Interactive Brokers. Interactive Brokers does not make any representations or warranties concerning the services provided by the third-party providers.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account