The sharpest US job losses in 32 months heightened rate cut optimism, reignited investor enthusiasm and extended the recovery in stocks, Treasuries and bitcoin on Wednesday. In glass-half full fashion, no one appears worried about the softening state of the labor market, as bulls piled into reacceleration trades and bears became increasingly motivated to cover shorts. Additionally, strengthening confidence that National Economic Council Director Kevin Hassett, a Trump confidant, will be the next Fed Chair bolstered cyclically oriented areas in the equity space that benefit disproportionately from monetary policy accommodation. Indeed, the Russell 2000 and the Dow Jones Industrial benchmarks led the Wednesday advances amongst the indices, yields dropped relatively evenly across the curve as fixed-income watchers raised the probability of augmented easing in 2026, and the commodity complex was bullish on expectations that looser financial conditions will increase the demand for raw materials and propel activity. The greenback retreated, however, in light of narrowing central bank differentials, while volatility protection instruments experienced declining premiums due to risk-on energies on Wall Street. Traders gravitated to forecast contracts as well to express their views on critical economic, market and climate developments, with a particular emphasis on shorter-dated expirations.

Small Businesses Scale Back Workforce

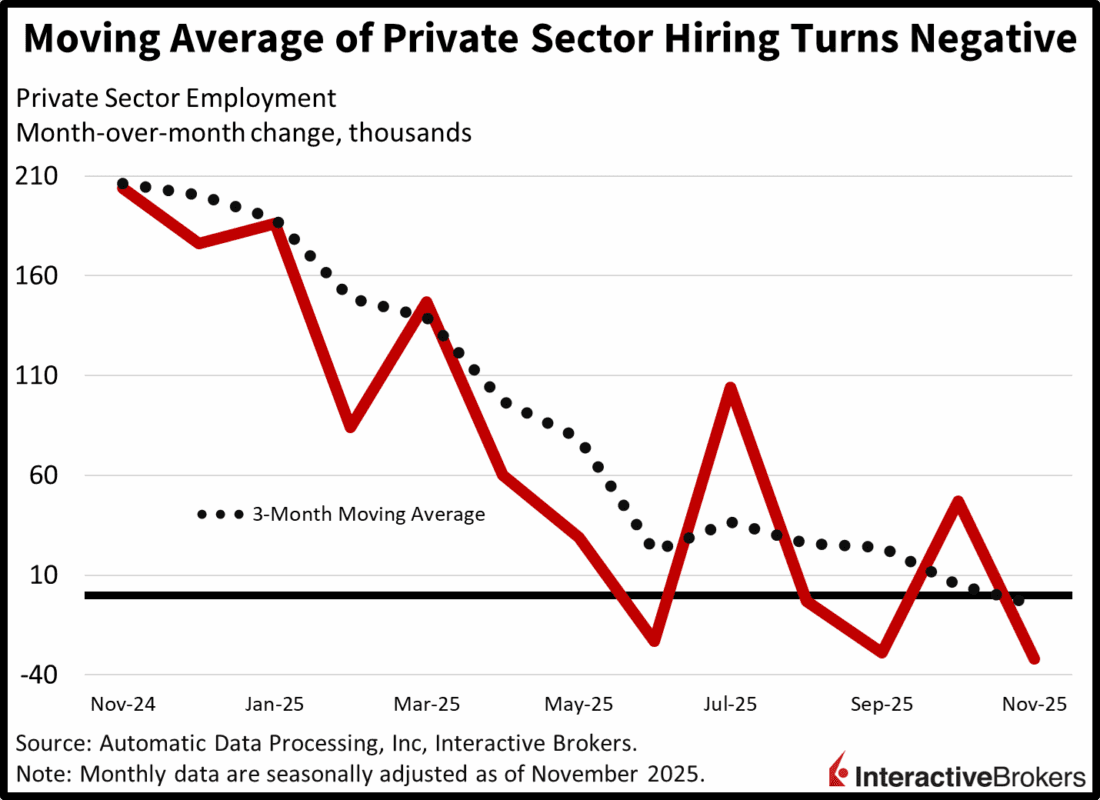

Pain at small US businesses drove sharp losses in November’s private sector payrolls, with 6 out of 10 industries reporting staff reductions. ADP’s jobs report, released Wednesday morning, depicted an overall decrease of 32k workers, well beneath projections of 10k and the October’s gain of 42k. It’s the fourth month of the last six with a negative number, dropping the three-month moving average of hiring below zero for the first time since the pandemic. Establishments with less than 50 employees led the weakness, with a roster reduction of 120k, although the contractions were partially offset by medium-sized firms with 50-499 staffers and large companies; they added 51k and 39k, respectively. Sectors that reduced employment and the extent of the changes were as follows:

- Professional/business services, 26k

- Information, 20k

- Manufacturing, 18k

- Construction, 9k

- Finance, 9k

- Other services, 4k

The impact of those sectors was partially offset by the stated employment gains in the following categories.

- Education/health services, 33k

- Leisure/hospitality, 13k

- Natural resources/mining, 8k

- Trade/transportation/utilities, 1k

In another sign of softening, compensation trends decelerated as the median year-over-year (y/y) change in annual pay slowed from 6.7% and 4.5% for job changers and stayers, respectively, to 6.3% and 4.4%.

Path for Russell 2000 Widens The small-cap, cyclically oriented Russell 2000 has the potential to deliver the strongest gains across the major domestic indices in the coming year. Today’s outperformance is driven by beliefs that the economy remains on a robust trajectory despite constant reminders of labor

market stress and enthusiasm that the Fed will cut next week as well as two or three times by the end of 2026. It’s precisely the mix of a strong cycle alongside looser financial conditions that can lead to a significant rally in smaller companies that are heavily vulnerable to shifts in activity and restrictive monetary policy. Indeed, an extended expansion helps the index’s constituents bolster top lines, while lighter borrowing yields drive lower debt service costs for an area of the equity space that carries increasingly fragile balance sheets relative to blue-chip counterparts. Furthermore, an economic reacceleration and Fed reductions can swing many of the firms in the gauge that lose money into profit territory. The trade may interest folks that would like to be in stocks but are worried about valuations amongst the magnificent 7, are concerned of the risk-reward dynamics of AI and/or want to position for a broadening of the equity rally in the near future while growing diversification throughout sectors.

International Roundup

Services Sector Growth in China Slows

China’s services industry continued to expand in November, but the growth was the slowest in five months, according to the RatingDog China General Services Purchasing Managers Index (PMI) from S&P Global. The gauge slipped from 52.6 to 52.1, staying above the contraction-expansion threshold of 50. New orders increased at the slowest pace in five months, but exports reversed from previous declines with reduced uncertainty about global trade shoring up demand from abroad. However, unfinished work orders grew, a result of declines in employment staffing. In other areas, elevated costs of fuel, raw materials and office supplies caused input expenses to climb. The higher costs were only partially passed on to customers in the form of higher prices. On a positive note, confidence among services companies continued to strengthen. The government issued Services PMI that was released this past weekend also declined, falling six points to 49.5.

Hong Kong Economic Activity Expands with Exports Growing

Hong Kong experienced its first increase in export sales in 13 months during November, which contributed to the S&P Global Hong Kong SAR PMI climbing from 51.2 to 52.9. It was the fourth consecutive month of increasing results from the index. Overall new orders and output both grew at accelerated paces relative to October. Additionally, input costs climbed at the second-fastest rate in nearly two years. Those costs were partially recouped by businesses with output prices climbing at the fastest pace since September 2024. Also last month, pessimism regarding business conditions eased but sentiment was still downbeat, preventing companies from hiring workers.

Singapore Business Activity Also Climbs

Singapore business activity grew last month at its fastest pace in more than three years, but higher input costs, lower selling prices and issues with transportation and labor caused the S&P Global Singapore PMI to fall two points to 55.4. A sharp rise in new orders fueled by successful marketing and new projects caused businesses to increase their purchasing and hiring, which contributed to the overall increase in activity. Conversely, supply delays, declining selling prices, higher input costs, growing lead times and a labor shortage pushed the headline result down. In a similar manner, sentiment eased to a three-month low but stayed positive with firms remaining hopeful that market conditions and internal growth plans can support future sales.

Europe Gate Prices Fall Y/Y

The Producer Price Index in Europe slipped 0.5% y/y in October, a worse decline than the 0.4% drop expected by a consensus of economists and an acceleration from the 0.2% descent in September. On a m/m basis, prices were up only 0.1%, matching the economist consensus after September’s 0.1% decline.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account