Originally posted, 18 Feb 2025 – Three reasons why it may be a mid-cap sweet spot

Authored by: Sergio Marcheli, Portfolio Manager, Equities | Greg Holland, Senior Client Portfolio Manager, Invesco Growth Equities

Key takeaways

Leadership rotation

In recent, months, with little fanfare, mid-cap stocks have taken over market leadership from large caps.

Earnings growth

Mid-cap earnings growth is currently inflecting with 2025 estimates exceeding earnings growth for large caps.1

Better diversification

There’s industry diversification and opportunities to deliver alpha through stock selection within mid cap, in our view.

After an extended period of large-cap leadership, a rotation back to mid-cap leadership already appears in motion with an increasingly attractive setup for 2025. Mid caps outperformed in January as the market has started to broaden.2 We believe it may be a positive setup for the under-invested mid-cap “sweet spot.” Here are three reasons why.

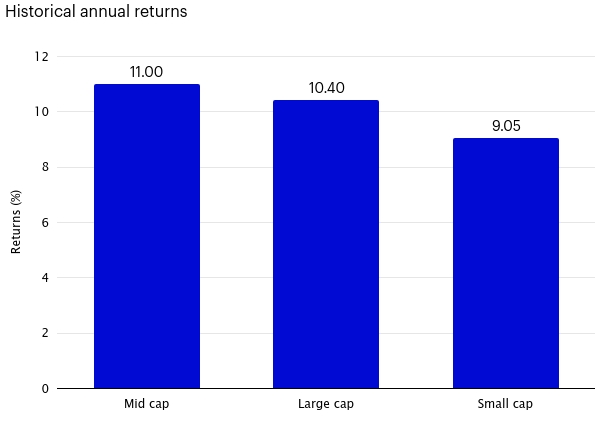

No. 1: Historical and recent outperformance

With an 11.0% annualized return, mid caps have outperformed small caps (9.05% annualized return) and large caps (10.4% annualized return) since the inception of the Russell Midcap Index in 1991.3 And they’ve done this often. Mid caps outperformed large caps 56% of the time and small caps 92% of the time for monthly five-year rolling periods.3

Mid caps have a history of outperformance

Source: Morningstar, 12/31/24. Mid caps are represented by the Russell Midcap Index, small caps are represented by the Russell 2000 Index, and large caps are represented by Russell 1000 Index. An investment cannot be made in an index. Past performance does not guarantee a profit or eliminate risk of loss.

No. 2: Better earnings growth and valuation with potential policy benefits

Mid-cap earnings growth is currently inflecting to the upside, with 2025 estimates exceeding large-caps and at lower valuations.1 Also, while the number and pace of interest rate cuts in 2025 are open questions, the Federal Reserve’s (Fed’s) normalization around current levels has already removed a financing headwind for many mid caps. Our research shows small caps still face significant refinancing risk over the next two to three years. To avoid a negative impact, they would need more cuts than are currently expected.

While the Trump administration’s government policy is still uncertain, potential tariffs and negotiations aimed at stimulating US production would likely be advantageous for mid-cap companies, which tend to be domestic businesses. The potential for lower corporate tax rates in 2025 could benefit all US stocks. If there are additional tax breaks for US production, it could further benefit mid caps. Many of these potential policies should benefit small caps, too; however, we see lower-quality earnings and some offsets that make us less optimistic about them versus mid caps.

Higher growth at a lower price

Sources: FactSet Research Systems, Inc., Jefferies Research, 12/28/24. Mid caps are represented by the Russell Midcap Index and large caps by the Russell 1000 Index. There is no guarantee that future estimates will come to pass. An investment cannot be made directly into an index.

No. 3: Less concentration = better diversification and opportunity

Much has been made about the concentration of the S&P 500 Index in a select group of mega-cap “Magnificent Seven” stocks — Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia, and Tesla.4 Technology-related businesses now dominate growth-style large cap. There’s more industry diversification and opportunities to deliver alpha through stock selection within mid cap, in our view. Some of the best-performing companies in our mid-cap portfolios are a handful of companies behind NVIDIA’s success or that are benefitting from their ecosystem, not just in tech but across sectors, including industrials and utilities.

What hasn’t been discussed as much is how the best small caps have evolved into attractive mid caps and that the number of investable companies in the small-cap universe has been shrinking. It’s not the size of the companies that’s shrinking. Many of the premier small-cap companies we invest in have more than doubled in size, and many of the best-managed companies have graduated into mid-cap companies because of their success. That’s why we’re seeing higher-quality and better-managed mid-cap companies, while the quality of the small-cap universe hasn’t been refreshed.

A contributing dynamic during the last few years is that new initial public offerings (IPOs) haven’t been added to the small-cap opportunity set. Abundant private equity capital, significant regulatory requirements, and the high costs of going public have led many companies to remain private. In fact, some of the best IPO companies during the last two years were delayed and then came to market as mid caps. While we expect IPOs to improve in 2025, we also expect mergers and acquisitions (M&A) to improve dramatically and keep this dynamic in place.

Optimistic outlook

The economy has shown healthy resilience, and the Fed is patiently normalizing policy with what appears to be a beneficial downward bias. Also, the Intrinsic Value and Discovery Growth teams at Invesco have a unique point of view and competitive advantage in the marketplace. They’re deep and experienced teams with long track records of identifying early-stage small-cap opportunities, which can then compound over time, and they graduate what they believe are the best of them into mid-cap funds.

Learn more about mid-cap at Invesco, including Invesco Discovery Mid Cap Growth Fund and Invesco Value Opportunities Fund.

Footnotes

- 1 Sources: FactSet Research Systems, Inc., and Jefferies Research, 12/28/24. Mid caps are represented by the Russell Midcap Index and large caps by the Russell 1000 Index. There’s no guarantee that future estimates will come to pass.

- 2 Source: Data is based on the performance of Russell Midcap Index 4.25% versus the Russell 2000 Index 2.63% and the Russell 1000 Index (3.18%).

- 3 Source: Morningstar, 12/31/24. Mid caps are represented by the Russell Midcap Index, small caps are represented by the Russell 2000 Index, and large caps are represented by Russell 1000 Index. An investment cannot be made in an index. Past performance does not guarantee a profit or eliminate risk of loss.

- 4 Source: The Invesco Value Opportunities and the Invesco Discovery Mid Cap Growth portfolios don’t hold any of the S&P 500 Magnificent Seven stocks.

Disclosure: Invesco US

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account