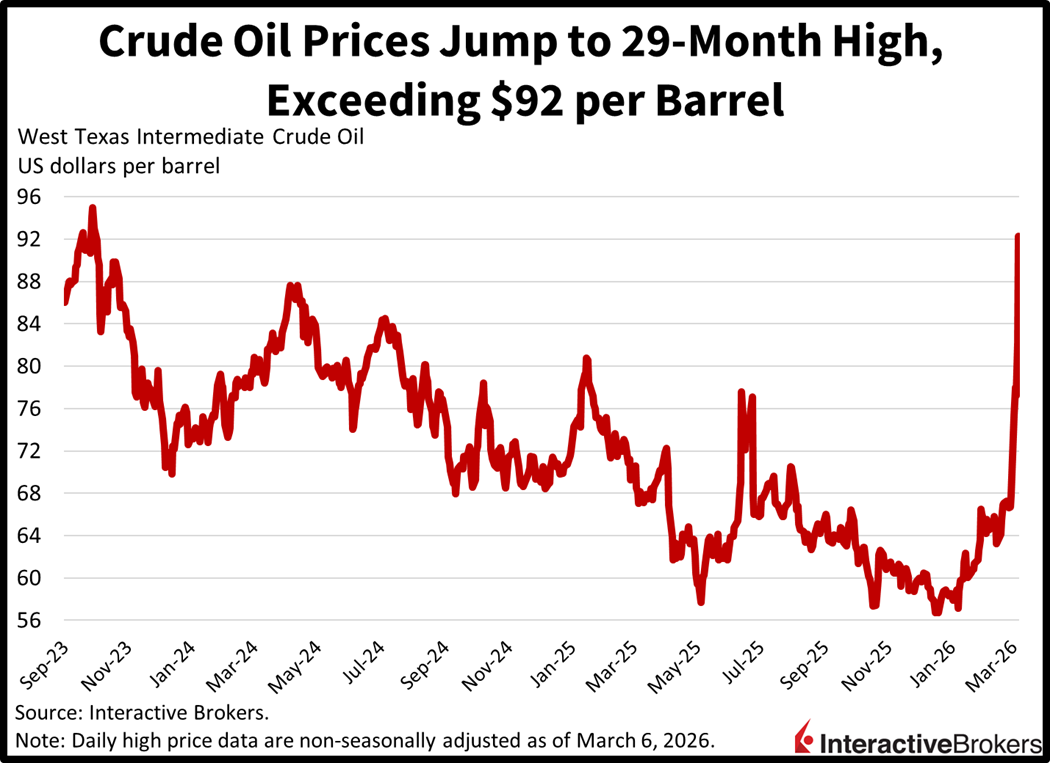

Rising pessimism concerning peace in the Middle East combined with an awful nonfarm payrolls report sent stagflationary winds throughout markets on Jobs Friday. A 29-month high in crude prices coinciding with a colossal employment loss of 92k sparked worries among investors that inflationary risks may keep the Fed from cutting even as labor conditions deteriorate. And in a week that featured terrific economic data up until the last day, retail sales posted a decline, generating doubts about the ability for consumers to weather this spike in gasoline costs without derailing expenditures on other staples and discretionary activities. But the traditional Treasury rally you’d expect from weak activity figures isn’t manifesting due to the war in Iran, with participants on Friday instead meaningfully raising exposure to commodities, especially gold, silver, oil and natural gas. Stocks got creamed across sectors and benchmarks with energy the sole gainer out of the 11 major categories as traders clamored for volatility protection instruments, effectively lifting put option premiums. Elsewhere, risk-off moods punished crypto, the greenback was nearly flat and forecast contracts caught bids.

Past performance is not indicative of future results.

US Economy Lost 92k Jobs in February

The US economy lost 92k jobs last month with broad-based reductions across sectors. The enormous disappointment came in well below the consensus expectation for a 50K expansion and downwardly revised 126k additions for January. A strike in the health care industry, a sector that has been a consistent driver of employment gains in the past few years, dented about 31k from the headline. Meanwhile, 9 of the 14 categories saw rosters shrink with the number of losses as follows:

- Private education/health services, 34k

- Leisure/hospitality, 27k

- Manufacturing, 12k

- Transportation/warehousing, 11k

- Construction, 11k

- Information, 11k

Government, professional/business services and mining experienced headcount drops of 6k, 5k and 2k. Conversely, financial activities, other services, wholesale trade, retail trade and utilities each added 10k or less.

While Unemployment Rate Ticks Higher

The unemployment rate reported on Friday was also worse than expectations, with the 4.4% figure arriving ahead of the projection calling for an unchanged 4.3%. Part of the uptick in joblessness could be explained by a 50-month low in the labor force participation rate, which dropped to 62% and remains well off its pre-pandemic peak of 63.3%. But on the bright side, wages grew much faster than inflation, with average hourly earnings expanding 0.4% month over month (m/m) and 3.8% year over year (y/y), above forecasts by one tenth of a percent and similar to February’s 0.4% and 3.7% statistics.

And Consumer Spending Contracts

Consumers pared back their shopping enthusiasm to start the year, as the January retail sales report posted a contraction. The print was delayed due to the longest government shutdown in history but slightly beat expectations of -0.3%, coming in at -0.2%. The control group, which excludes gas, autos, building materials and food services and is a critical input to the government’s gross domestic product (GDP) calculation, also came in ahead of projections, growing 0.3% versus the 0.2% forecast while recovering from 0 in December.

Pre-owned Car Prices Climb

Used car prices rose last month, according to the Manheim Index. February costs ascended 0.8% m/m and 4% y/y compared to January’s figures of 2.4% m/m and 2.4% y/y. Traditional engines continued to outperform their electric counterparts, rising 0.9% m/m and 3.7% y/y relative to the latter’s 0.8% and 1.8%.

Stocks Have Not Closed Near Daily Lows This Week

Despite the meaningful market volatility this week, stocks have not closed near their daily lows as of Friday afternoon because traders have used price declines as buying opportunities. Today’s intraday rebound is significant, as it’s occurring while crude oil is making new highs north of $92. Both developments transpiring simultaneously is quite shocking, as the former is telling us that economic fundamentals are weakening due to short-term expectations of an increasingly extended war in Iran, while the latter is potentially signaling that equity investors believe that the conflict may be over faster than commodity watchers think. Meanwhile, there’s no doubt of a heavy dose of uncertainty related to the cycle, and if employers didn’t hire much in February, before the Middle East battle started, then they’ll probably do even less recruiting this month. Overall, activity figures will begin to materially weaken if West Texas Intermediate remains in the vicinity of $100 for a few weeks, and that bodes poorly for the reacceleration trade, rate cuts and ongoing expansions in both corporate earnings and GDP.

International Roundup

South Korea Inflation Cooler Than Expected

Prices in South Korea climbed 0.3% m/m and 2% y/y last month, according to the Consumer Price Index. Both metrics depict slower inflation than the economist consensus estimates for increases of 0.4% and 2.1% relative to January and the year-ago period.

On a m/m basis, consumers paid 1.4% more for recreation and culture. In other areas, the restaurants and hotels classification, the transport segment and the housing, water, electricity, gas and other fuels group each experienced 0.4% hikes while foods and non-alcoholic beverages experienced a 0.3% gain. Other categories either demonstrated weaker price pressures or no changes except for health and the furnishings, household equipment and routine maintenance categories. They became 0.2% and 0.1% less expensive.

And Equities Recover From Freefall

After a handful of volatile trading days for South Korea equities, the country’s KOSPI Index closed the week flat as dip buyers stepped up to the plate after the benchmark fell 20%. Exchange traded funds that seek to generate twice the return of the market intensified the selloff that was triggered by fears about the Middle East war causing oil prices to climb. The country is heavily dependent on imports of the commodity and is one of the world’s largest purchasers of energy products that are shipped through the troubled Strait of Hormuz.

UK Home Price Gains Continue

Prices for dwellings in the UK were up 0.3% m/m and 1.3% y/y in February after ascending 0.8% and 1.1% in January, according to the Halifax House Price Index. The m/m metric matched the economist consensus estimate while the y/y statistic was considerably stronger than the expected 0.9% result. The gains brought the average price to £301,151, an all-time high and the y/y print was the strongest in four months. Halifax believes the housing market is gaining momentum after a sluggish end of 2025 despite supply constraints and low affordability. At the same time, real wages have been strengthening, and mortgage rates are easing, helping to improve buyer confidence. Geopolitical uncertainties, however, are likely to cause a slower decline in interest rates than previously anticipated.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account