With the S&P 500 (SPX) leaping about 1% on today’s open thanks to a data point that typically goes unnoticed, I have an important question for the buyers: are you the same people who were clamoring for an emergency 50 basis point rate cut on Monday?

I usually prefer to start writing these daily pieces after the market opens because it gives me a clearer picture of the market’s direction, but I’m starting this piece a bit earlier than usual because I can barely contain myself. Yes, this relatively significant rally is the direct result of weekly jobless claims coming in with a net decline of 6,000 after revisions. Ask yourself when you last paid much attention to this data point, let alone launched a huge rally or decline in its wake. I can’t remember this big of a reaction to this pedestrian report.

But then again, these are not normal times. Yesterday’s 2.5% high/low trading range in SPX is Exhibit A. We’re still working through the aftereffects of the huge carry trade unwind that has rocked global markets since the Bank of Japan raised rates last week. According to published reports, JPMorgan (JPM) analysts estimate that the carry trade is now 75% unwound. I’m not sure how they arrived at that figure, since currencies trade over-the-counter and it is extraordinarily difficult to know exactly what is collateralizing debt (the most extreme examples of this are Long Term Capital Management and Archegos). As a result, even analysts at a bank with much more transparency into these mechanisms acknowledge that their data is not perfectly reliable.

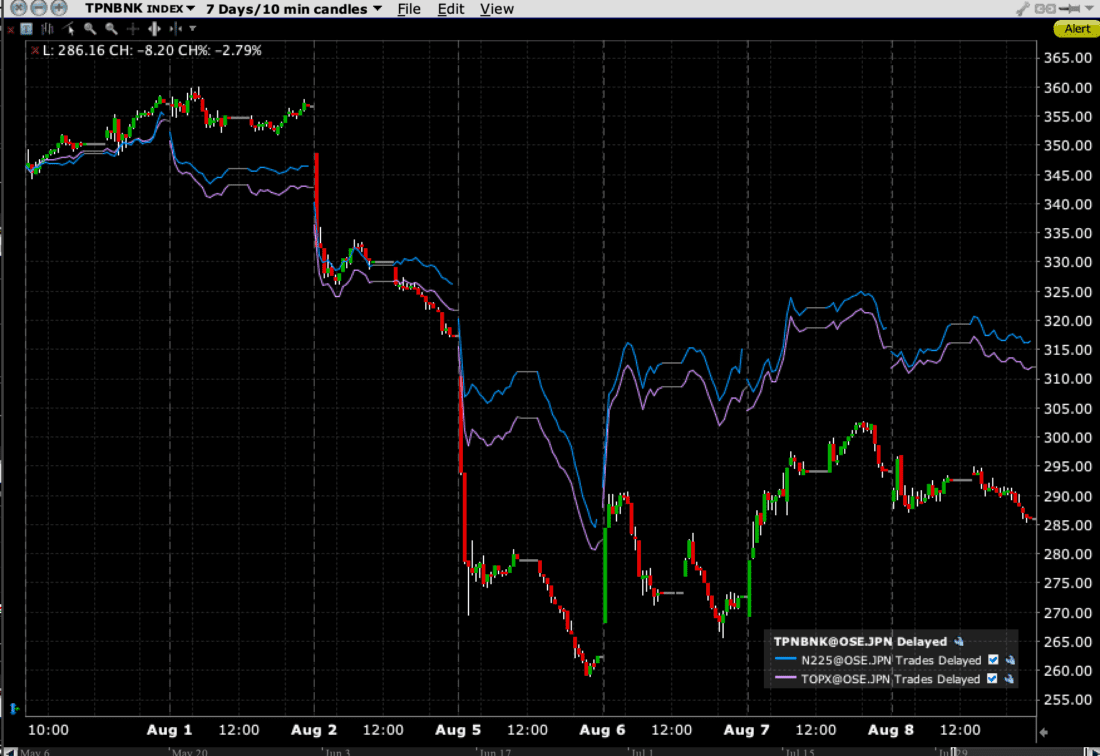

One way that I have been tracking the stresses that may be resulting from the carry trades is the Tokyo Exchange TOPIX Bank Index (TPNBNK). It has drastically underperformed the other key Japanese indices, the Nikkei 225 (N225) and TOPIX (TOPX). Since July 31st, the day that the BOJ raised rates 25 bp when the market had priced in roughly a 50% chance of a 10bp hike, triggering the carry trade unwind, the broader benchmarks are both down about -10% while the bank index is down about -20%. Japanese bank investors are not ready to declare an “all clear” yet.

Since August 1st, 2024: TPNBNK (red/green 10-minute candles), TOPIX (purple line), N225 (blue line)

Past performance is not indicative of future results.

Now consider this morning’s rally in light of the panicky commentary from a wide range of market pundits earlier this week. I was particularly dismayed on Monday morning to see my former professor, Jeremy Siegel, clamoring for an immediate 75 bp cut and another 75bp in September. His assertion is that the neutral rate is somewhere in the 3.5-4% range, and that the Fed needs to get us there ASAP. I defer to his superior skills as an economist about the proper level for the neutral rate, but as a long-time, full-time market practitioner, those moves would have completely spooked the market. Abandoning the path that the FOMC has painstakingly laid out would have been interpreted as panic. “What do they know that we don’t?!?!”

If Chair Powell knows something that we don’t or believes that a faster pace of rate cuts is warranted, he has more than ample opportunity to tell us why when he gives his annual Jackson Hole address in two weeks.

I firmly believe that US-centric investors were too quick to blame Monday’s declines in both stocks and bond yields on recessionary fears. Stock traders have been quick to pounce on any rally since then, even if they have shown a tendency to fade, and the subsequent jump in bond yields show that the recent plunges were more about flight to safety and carry trade closeouts. Neither point to major concerns about a looming recession.

I’ll leave economic punditry to economists but since the Fed has forced us all to become data dependent – if they are, so must we be – my read of the data is that it’s mixed, not dire. In a podcast taped earlier this week, my colleague Jose Torres noted that the ISM Services report contrasted with last week’s downbeat ISM Manufacturing report. The Atlanta Fed’s GDPNow currently projects a 2.9% rise in GDP. It does appear that the conflicting data could certainly indicate that the economy is at an inflection point. I will by no means rule out the possibility or even likelihood of a recession. But it is premature, if not flat out wrong, to say that those fears are an overarching concern.

And now that SPX is up another ¾% since I started typing, can we say that today’s number has quelled the looming recession fears? Absolutely not. Can we say that stock traders remain fixated on buying dips and chasing rallies? Absolutely yes. Does the latter indicate that we desperately need rate cuts to keep markets afloat? C’mon, quit your whining.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account