Originally Posted 20 January 2026 – Looking back at equity factors in Q4 2025 with WisdomTree

Key Takeaways

- Europe and emerging markets led 2025 equity performance, beating US returns as dollar weakness and controlled valuations supported ex-US rerating.

- Value was the clear factor winner, especially in Europe and emerging markets, driven by banks, cyclicals, defence, industrials and dividend-rich stocks.

- In Q4, Value stayed on top while Quality showed signs of life, suggesting leadership has broadened beyond pure artificial intelligence (AI) growth.

Looking back to 2025, equities proved tougher than the headlines. After an early-year tariff shock and a sharp April drawdown, a powerful ‘everything rally’ took hold as central banks eased and the US dollar weakened. Artificial Intelligence (AI) remained the defining growth engine, but leadership broadened beyond the mega-caps. Emerging markets and Europe ultimately outshone the US, even though US equities delivered strong double-digit gains. In Q4, markets wobbled: November’s risk rally slowed as AI spending and US Federal Reserve easing narratives were stress-tested, yet equities recovered into December with rate-cut expectations firming.

From a factor perspective, Value stocks maintained their leadership, particularly within the European and Emerging Markets. Quality stocks also showed some renewed strength in Q4.

This instalment of the WisdomTree Quarterly Equity Factor Review examines how equity factors behaved during the fourth quarter and the potential impact on investors’ portfolios.

Performance in focus: Value keeps the lead

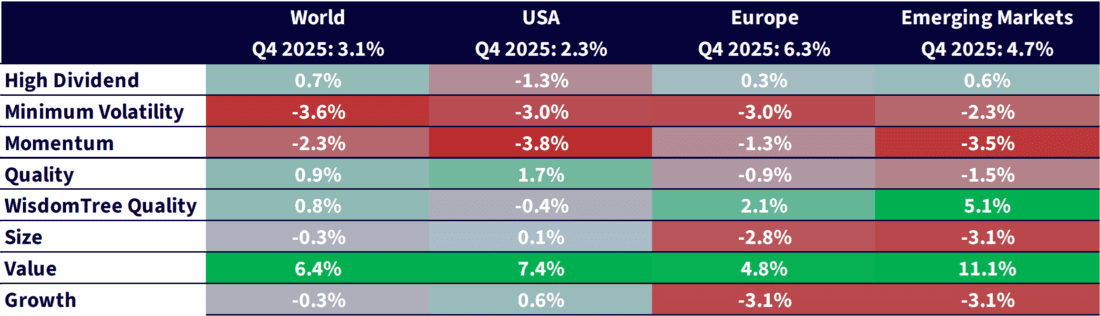

Equity markets rebounded at the end of Q4 after a very sluggish start. The MSCI World outperformed US Equities (+3.1% versus +2.3%), thanks to strong performance in Europe (+6.3%) and Emerging Markets (+4.7%). This Q4 split echoed the broader 2025 rotation: developed ex-US markets did the heavy lifting, with Europe extending a multi-quarter run of outperformance. Emerging markets also advanced, supported by a weaker dollar and improving global growth.

Value continued to dominate in Q4:

- Value posted the strongest returns in all regions (US, Developed World, Europe and Emerging Markets).

- Minimum Volatility and Momentum suffered across all regions this quarter.

- After a difficult first three quarters of the year, Quality is showing some strength in the US and Developed Markets. High-quality, dividend-growing stocks did particularly well in Europe and Emerging Markets.

- Growth underperformed across regions except the US, where it managed to outperform.

Figure 1: Equity factor outperformance in Q4 2025 across regions

Source: WisdomTree, Bloomberg, MSCI. 30 September 2025 to 31 December 2025. Calculated in US Dollars for all regions except Europe, where calculations are in EUR. Historical performance is not an indication of future performance and any investments may go down in value.

2025 in review: a Value-led year beyond the US

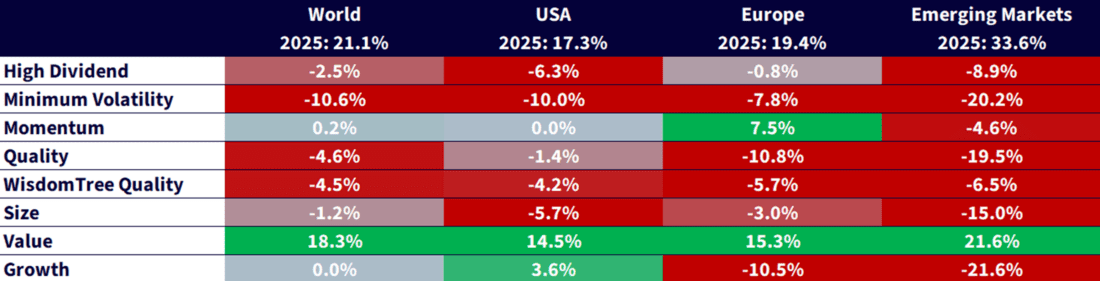

2025 ultimately delivered for equity investors. The MSCI World gained 21.1% in advance of US Equities (+17.3%). For the first time in some years, European and emerging market equities outperformed the US over the full year. That outperformance was largely driven by foreign exchange and valuation effects. A weaker US dollar and still-stretched US valuations meant ex-US equities had greater scope for multiple expansion as rates eased.

Factor-wise, Value definitely won in 2025:

- Value outperformed by double digits in all four regions in 2025, with +15.3% in Europe and +21.6% in Emerging Markets.

- Minimum Volatility, Size and Quality stood out from the other end of the spectrum in 2025 with underperformance across all regions despite a Quality revival in Q4.

- Growth’s performance was very mixed, with outperformance in the US but double-digit underperformance in Europe and Emerging Markets.

- In Europe, Momentum performed strongly, posting the second-best returns after Value.

Figure 2: Equity factor outperformance in 2025 across regions

Source: WisdomTree, Bloomberg, MSCI. 31 December 2024 to 31 December 2025. Calculated in US Dollars for all regions except Europe, where calculations are in EUR. Historical performance is not an indication of future performance and any investments may go down in value.

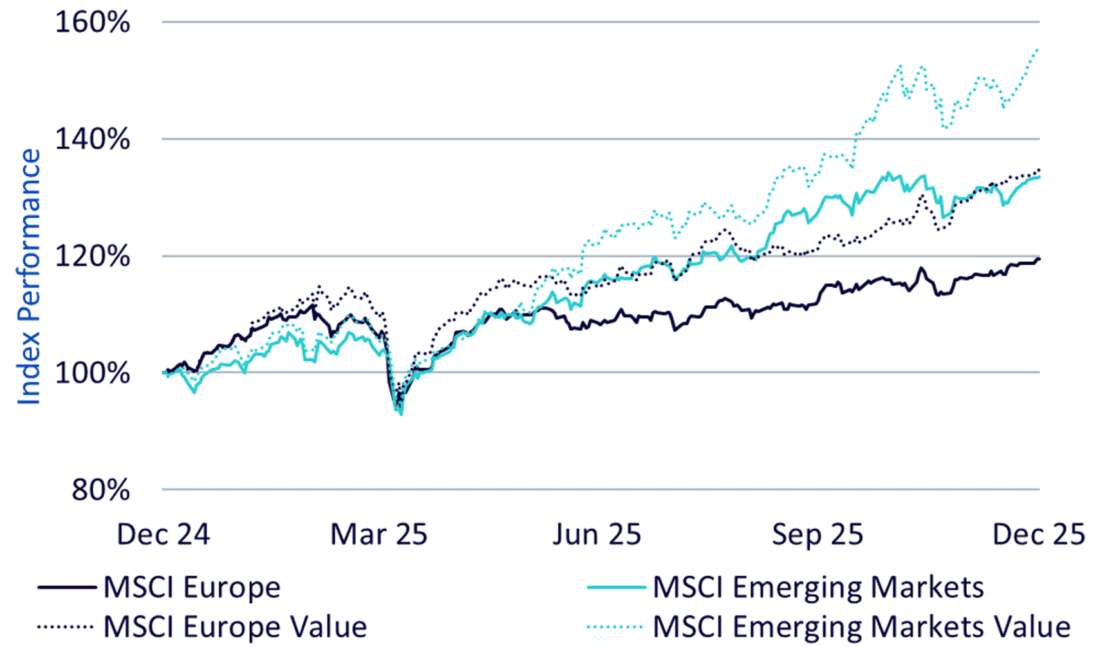

Europe and Emerging Markets powered a Value-led year

In Europe, Value’s leadership in 2025 was driven by a classic mix of policy support, earnings resilience and compelling valuations. Investors’ attention turned to cash-generative names and away from the narrow US AI trade. Banks were notable winners, benefiting from a re-steepening yield curve. Defence and industrial stocks benefited from higher order books tied to re-armament and upgrades buoyed by Germany’s multi-year infrastructure and defence push. 2025 was a year that rewarded balance-sheet strength, dividend durability and operational leverage, attributes that are concentrated in Europe’s value cohort.

Emerging markets also benefited from the weaker US dollar and cheaper starting valuations. The rally was quite broad-based, but value-heavy pockets did best where currency tailwinds and policy support were strongest.

Figure 3: Value outperformed in Europe and Emerging Markets in 2025

Source: WisdomTree, Bloomberg, MSCI. 31 December 2024 to 31 December 2025. Calculated in US Dollars for all regions except Europe, where calculations are in EUR. You can not invest in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Looking forward to 2026

Looking to 2026, existing trends remain in place:

- The US is benefiting from the rate easing cycle, fiscal tax cuts and an improved growth outlook, but still suffering from high valuation and ultra-high concentration around the AI narrative. Investors may benefit from a more resilient allocation to US equities by investing in high-quality, dividend-growth stocks.

- Strong stability of rates and continued government stimulus around Defence and Infrastructure in Europe that should continue to push European Value names.

- Earning improvements, a weak US dollar and improved domestic demand is leading to a positive environment for emerging market equities.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account