The nomination of Kevin Warsh as governor and chair of the Federal Reserve was approved by Senate Banking Committee on Wednesday. A full Senate vote can now be scheduled for his appointment to the term as governor ending January 31, 2040. His term as chair of the Fed will be for four years beginning when he is sworn in. Warsh is expected to be confirmed soon.

Jerome Powell has said he will step down as chair as soon as Warsh is ready to step up. However, he plans to retain his seat on the board for the time being. Powell’s term as governor runs through January 31, 2028. His intention is to remain on the board until he is confident that political attacks on the Fed’s independence by the Trump administration are at an end. In the present climate, it would suggest that Powell is on the board for the duration.

Powell has extended a gracious welcome to Warsh when the time arrives for him to take his place on the Board of Governors. Powell has also emphasized that he will not serve as a “shadow chair” but only within his remit as a governor.

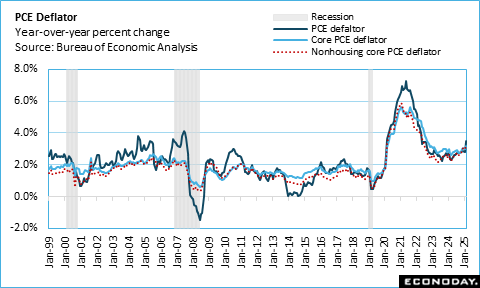

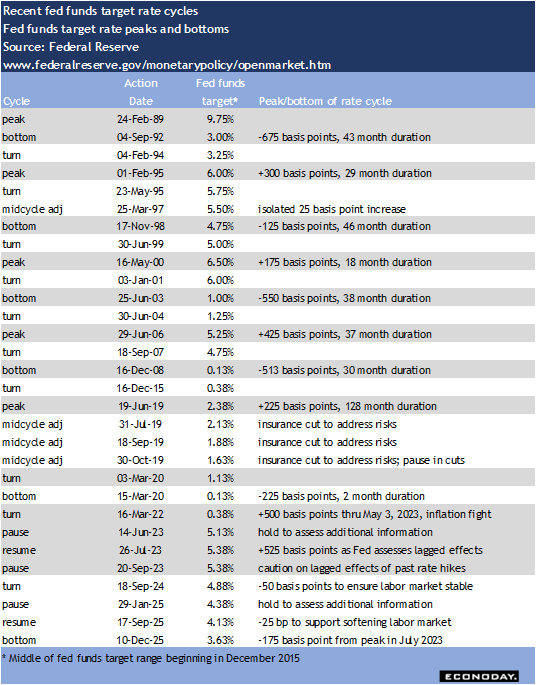

The changeover in leadership comes at a pivotal time for monetary policy. The FOMC has been working to bring down inflation through interest rate policy since the peaks in 2021. Initially it was prices pressures in services holding back disinflation progress, but that had started to improve by early 2025. Then there was the price shock from the imposition of punitive tariffs starting in April 2024 which led to higher prices in commodities that are only now finally passing through the inflation data. However, the oil shock brought on by the start of the war on Iran on February 28 has delayed progress in disinflation again. How long that impact will take to move through the US economy is uncertain.

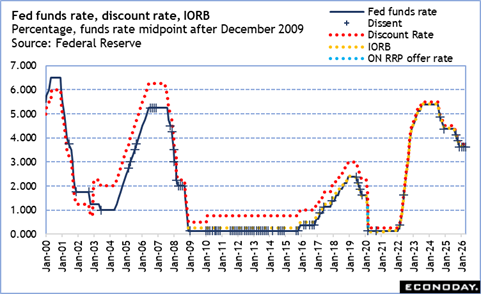

The FOMC decision on April 29 to leave the fed funds target rate range at 3.50 to 3.75 percent was as expected. The accompanying statement was not much different from recent ones except in two aspects.

First, the statement did not include the “somewhat” characterization of “elevated” inflation. This indicates that the committee saw the risks to price stability as more pronounced at present, while the risks to maximum employment were not much changed.

Second, while the vote on maintaining the current fed funds target rate range was 11-1 with a dissent from Stephen Miran as anticipated, it was not the only dissent. Three of the district bank presidents “supported maintaining the target range for the federal funds rate but did not support inclusion of an easing bias in the statement at this time”. This suggests that a growing minority of Fed policymakers may be thinking at a rate increase should be more central to future policy discussion.

The question is if a rate hike could be done as the sort of insurance move to keep inflation from becoming entrenched. The use of a mid-cycle adjustment is not unknown and could be used as a signal by the Fed that it will continue to maintain its credibility as an inflation fighter and also communicate that it is paying attention to the data and the impact on household budgets.

—Past performance is not indicative of future returns.

Originally Posted May 1, 2026 – Last Week in Review: Weighing Iran War Effects on Wholesale Prices

Disclosure: Econoday Inc.

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account