Investors are trimming equities in favor of fixed-income during low-volume trading today as the year comes to a close. Similar to last week’s holiday-shortened days, market participants are considering the risks associated with 2025’s political shift. Folks are looking ahead to the incoming Trump administration, which may bring significant governmental reforms, trade conflicts and adversarial posturing that may not be supportive of extended equity valuations. Against this backdrop, the stateside economic calendar featured a continued recovery in the residential real estate sector but a deeper contraction in Midwestern manufacturing. Meanwhile, a tragic South Korea plane crash weighed on Boeing shares while the Asian nation’s industrial production data underwhelmed.

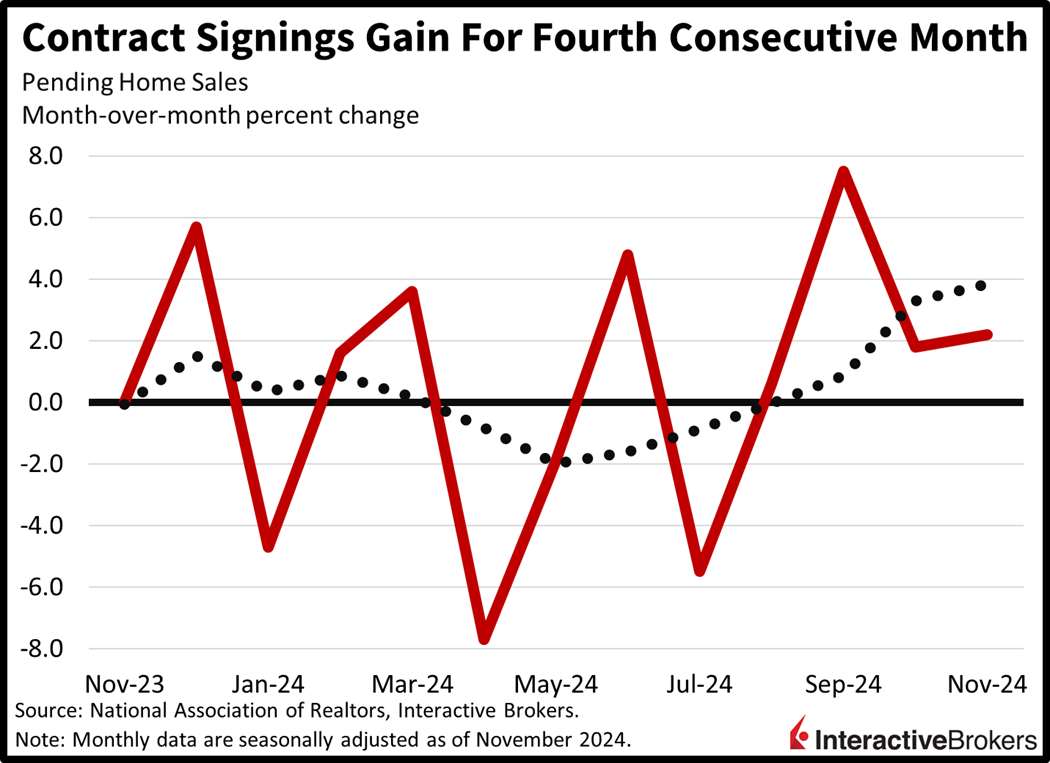

Contract Signings Maintain Streak

A psychological acceptance of higher-for-longer mortgage rates is slowly shifting the residential real estate market in favor of buyers, with contract signings rising to the greatest level since early 2023. Sellers, meanwhile, are incrementally acquiescing to monthly payment constraints in order to close transactions, with November pending home sales rising for the fourth month in a row. Contract signings rose 2.2% month over month (m/m), exceeding the 0.8% consensus estimate as well as October’s 1.8%. The South, West and Midwest led with increases of 5.2%, 0.5% and 0.4%, while the Northeast experienced a 1.3% decline. The report is a leading indicator to home closings, as agreements are acknowledged roughly 30 days before keys are turned over.

Past performance is not indicative of future results.

Midwest Manufacturing Sinks Further

The state of Midwestern manufacturing worsened this month at a deeper degree than in November, according to the Chicago Purchasing Managers Index (PMI). December’s score of 36.9 was worse than the 42.5 anticipated and the 40.2 from the preceding month. A score below 50 indicates contraction. Weak new orders weighed on production activity and pricing power, but the sluggishness was modestly countered by gains in employment, supplier deliveries and backlogs.

Japan Factories Just Shy of Expansion

Manufacturing conditions appear to be stabilizing in Japan, however, with December’s final PMI reading improving from its flash reading released earlier this month and approaching the contraction-expansion threshold of 50. The PMI was revised up to 49.6 from 49, compared to a reading of 49 in November. The weakness in new orders was less severe than initially reported, while employment and confidence contributed positively. But cost pressures jumped to a four-month high on the back of loftier materials expenses as well as a weaker yen.

Canada Business Sentiment Weakens

The Canadian Federation of Independent Business gauge of expectations for the next 12 months dropped from a more than two-year high of 59.8 in November to 56.4 this month. The retail and hospitality groups’ results of 52 and 51.7, respectively, were a drag on the headline number while the information, arts and creation sector and the financial services category strength continued, posting scores of 67.7 and 66.3, respectively.

South Korea’s Retail Sales Climb

South Korea’s retail sales swung from a decline to a 0.4% m/m increase last month, but industrial production faltered. The retail result was up significantly from the 0.8% and 0.3% contractions in October and September. The November gain, however, was attributed primarily to semidurable items with all other categories sinking. While duty-free stores recorded a 6.5% increase, sales at supermarkets fell 0.1%. On a year-over-year (y/y) basis, overall retail sales plunged 4.7%. Meanwhile, November industrial production dipped 0.7% m/m compared to the 0.4% decline anticipated by analysts and the preceding month’s flat result. The y/y growth rate of 0.1% also fell short of analysts’ outlook of 0.4% and October’s 6.3% gain.

Hong Kong’s Trade Deficit Grows

Hong Kong experienced a H$43.4 billion trade deficit in November, compared to the H$31 billion shortfall in the preceding month. On a y/y basis, exports climbed 2.1%, growing at a slower pace than the 3.5% rate in October. Imports jumped 5.7%, a faster pace than October’s 4.5% increase.

Investors Seize Profits

Stocks are selling off as investors book profits and lock in the yields of the day while the greenback strengthens as a result. All major, domestic, equity benchmarks are trading much lower with the Nasdaq 100, Russell 2000, S&P 500 and Dow Jones Industrial indices losing 1.4%, 1.2%, 1.2% and 1.1%. Sectoral breadth is deeply negative with all segments taking losses. Consumer discretionary, materials and technology are leading the way down; they’re sinking 1.6%, 1.4% and 1.4%. But Treasurys are catching a bid with the 2- and 10-year Treasury maturities changing hands at 4.26% and 4.56%, 7 basis points (bps) lighter on the session across both fronts. The greenback’s gauge is higher by 31 bps as a result, with the US dollar appreciating against the euro, pound sterling, franc, yuan and Aussie dollar. The US currency is depreciating relative to the Canadian tender and yen, however. Commodities are tilted bearishly with silver, lumber, copper and gold down 1.8%, 1.3%, 1% and 0.9%, but crude oil is bucking the trend, it’s up 1.2%.

Uncertainty Sustains Trump Bump

President Trump’s pro-business policies will support corporate fundamentals overall, but market participants don’t like uncertainty. The arrival of the GOP’s majority in Washington brings a much different dynamic than what we’re used to with the Biden administration, which didn’t offer much bumpiness. Indeed, the Democrats operated under a predictable framework, but the Republicans most definitely have a distinct mindset. Furthermore, stretched equity valuations alongside political turbulence pave the way for Trump bumps, despite the economy and earnings expected to continue growing. Finally, recession is on no one’s mind, considering Trump’s stimulative agenda, which includes lighter taxation, milder regulations and a push to incrementally propel the nation’s share of global manufacturing.

Jimmy Carter’s Legacy

We acknowledge the life of Jimmy Carter, who passed away yesterday. He was 100. During his presidency from 1977 to 1981, Carter appointed inflation hawk Paul Volcker as head of the Federal Reserve, pushed through deregulation, supported civil rights, forged the Camp David Accord with warring Middle East countries, and signed an agreement with the Soviet Union to limit nuclear weapons. However, he was also criticized for a failed attempt to rescue hostages from Iran, runaway inflation and a massive energy crisis involving a shortage of gasoline. After his presidency, the decorated former submarine officer won the Nobel Peace Prize for his work to promote and expand human rights. He is also well-known for being a key figure in Habitat for Humanity.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account