Originally Posted12 December 2025 – What’s Hot: Implications of China’s trillion dollar trade surplus

Key Takeaways

- China’s surplus reveals growth imbalances

- The Politburo’s 2026 priority list acknowledged that domestic demand, services and innovation must play a larger role from here

- SOE-heavy sectors may stay policy burdened and volatile

- The Politburo’s new emphasis on consumption supports a shift toward privately led EM exposure

- Related Products WisdomTree Emerging Markets ex-State-Owned Enterprises UCITS ETF – Acc Find out more

China crossed a symbolic threshold. Its annual trade surplus has pushed past US$1trn, the largest in modern economic history1. In November alone, the monthly surplus hit about US$112bn as exports grew nearly 6%yoy while imports barely moved1. Despite punitive US tariffs on many Chinese goods, exports have proved remarkably resilient. In November, shipments to the US were down almost 30%yoy, while Europe, Australia and Southeast Asia drove exports higher by 15%, 36% and 8% respectively1.

Essentially, China has responded to US pressure by –

- Re-routing trade through third countries in Asia

- Deepening ties with Europe and the Global South

- Building production bases abroad to skirt tariffs

At first glance, this looks like unambiguous strength. Chinese factories are busy, ports congested, and the country acting as the world’s chief supplier of everything from electric vehicles to solar panels and rare earths. But in Beijing, the mood is less triumphant and more cautious.

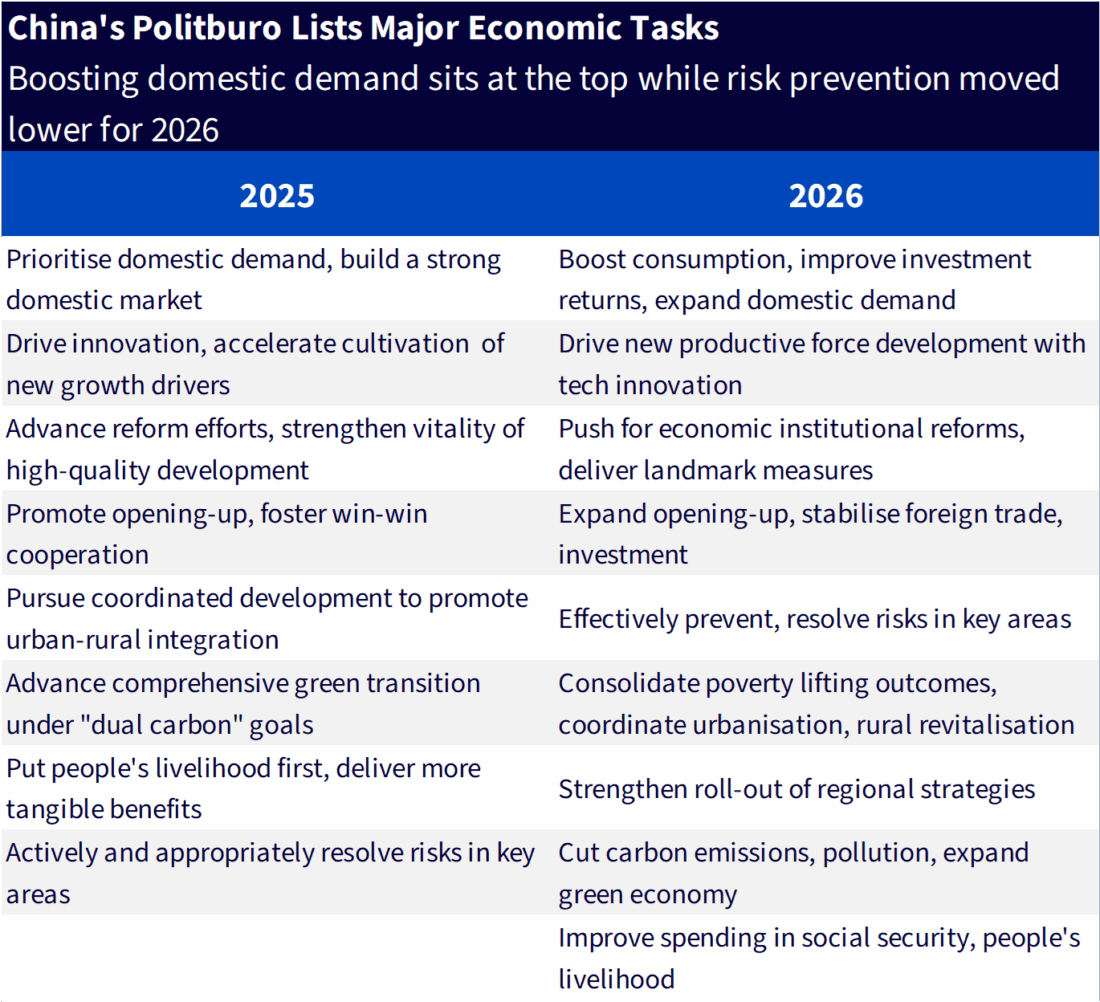

Politburo’s 2026 message: strengthen at home before the world turns harsher

In its December meeting, the Politburo made boosting domestic demand the top economic task for 2026, pledging to adhere to domestic demand as the main driver and build a strong domestic market”. Risk control in areas such as local government debt and the property sector was pushed down the priority list, and policymakers signalled a mildly more pro-growth stance with “proactive” fiscal policy and “moderately loose” monetary settings.

Source: Xinhua News Agency, Bloomberg as of 8 December 2025.

Put differently, China knows a trillion-dollar surplus is not a sign of a healthy balance, but of an economy that is still too dependent on external demand. For investors, this combination of external surplus and internal rebalancing has two big implications. First it raises the odds of more global trade frictions. Second it argues for titling toward China’s private, domestically oriented companies rather than State-Owned Enterprises (SOEs).

Global implications: more protectionism, more fragmentation

A surplus of this size is already having consequences. Premier Li Qiang has publicly warned that tariffs are damaging the global economy, even as he celebrates China’s export resilience. The European Central Bank (ECB) noted the surge in Chinese exports to Europe that began before Trump’s latest tariffs. Europe and the US are considering more anti-subsidy and anti-dumping measures, particularly in EVs, renewables and industrial equipment. The more China leans on external demand, the more likely it is to face pushback in the form of tariffs, quotas and local content rules. That introduces a layer of uncertainty for investors exposed to State-Linked exporters and heavy industry.

At the same time, the near-term political backdrop is more constructive than it has been for years. US-China relations have stabilised, and in 2026 Presidents Trump and Xi are expected to meet two to four times, marking an unprecedented level of direct engagement. This tentative thaw reduces immediate tail risks of a sharp escalation, even as strategic rivalry remains. Periods when the bilateral relationship is not actively deteriorating and when the policy focus shifts from sanctions to innovation, have historically been more favourable for China’s privately run growth oriented companies than for SOEs whose role is to absorb policy shocks.

Why this backdrop favours China’s private sector over State-Owned Enterprises (SOE)

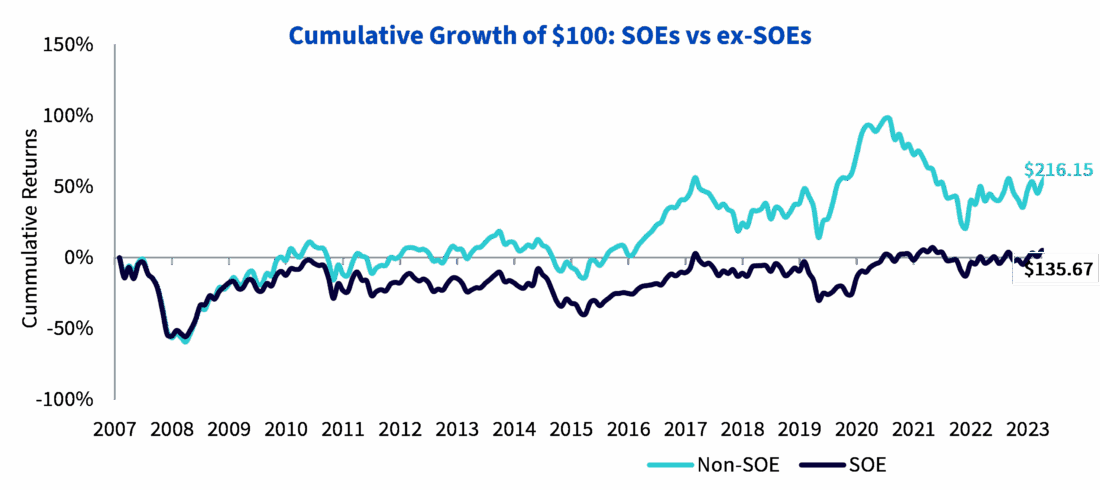

State Owned Enterprises (SOEs) tend to be concentrated in old economy sectors such as financials, energy, materials, utilities and industrials. They often serve as policy tools, offering cheap credit, absorbing labour and supporting politically important sectors, even at the cost of profitability. WisdomTree’s research on ex-SOE strategies shows that removing SOEs from the emerging markets universe tilts exposure away from these old-economy sectors and towards new economy sectors such as technology, consumer discretionary and communication services.

Figure 2: Historical performance of SOEs vs ex-SOEs

Source: WisdomTree, FactSet, Bloomberg from 31 December 2007 to 30 September 2025. Please note: Companies with 20% ownership by government body are defined as SOE. Universe of securities is the MSCI Emerging Markets Index. Returns are calculated in US dollars. Past performance is not indicative of future results. You cannot invest directly in an Index.

The WisdomTree Emerging Markets (EM) ex-State-Owned Enterprises UCITS ETF provides investors exposure to broad EM universe, investing in companies where government ownership is less than 20% of outstanding shares, making it the only fund of its kind. From an allocation perspective, that implies a higher exposure to information technology, consumer platforms, financials and industrial niches across China, Taiwan, India and Korea and a lighter exposure to energy, materials, real estate and utilities.

Year to Date, the WisdomTree EM ex-SOE UCITS ETF (Ticker: XSOE) posted 25.91%, maintaining competitiveness across the EM competitor funds in November 2025 as highlighted below.

Figure 3: Historical Performance vs EM Competitive landscape

Source: WisdomTree, Bloomberg, FactSet as of 18 August 2014 to 28 November 2025. Please note – WisdomTree is represented by WisdomTree Emerging Markets ex-State-Owned Enterprises ESG Screened Index TR. Vanguard is represented by the FTSE Emerging Net Tax Index TR. Fidelity is represented by the Fidelity Emerging Markets Quality Income Index NTR. UBS is represented by the MSCI Emerging Net Total Return USD Index. HSBC is represented by the FTSE Emerging ESG Low Carbon Select Net Tax Index. Calculations are based on returns in USD and include backtested/backcast data. Standard deviation estimates based on daily returns. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

What XSOE’s top EM holdings are telling us about the earnings landscape

As of the latest rebalance, the top 10 holdings account for roughly 30% of the XSOE portfolio, so their results provide a useful read through on how the broader EM ex-SOE universe is positioned heading into 2026.

Taiwan Semiconductor Manufacturing Co Ltd: reported Q3 2025 revenue of US$33.1Bn, marking a 10% sequential rise, with EPS up nearly 40%yoy. Management raised its 2025 sales outlook to mid30% growth, citing very strong demand for AI-related chips, even as overseas fabs dilute margins.

Alibaba Group Holding Ltd’s: Q3 2025 results earlier in the year showed 8% revenue growth, with EPS slightly below consensus but revenue marginally ahead. Markets interpreted it as a sign that the core commerce business is stabilising, and cloud remains a structural growth driver.

Samsung Electronics Co Ltd: delivered a 15% revenue increase and a sharp rebound in operating profit in Q3 2025, driven by its memory business and AI-oriented products. Management highlighted strong demand for high value added memory and continued investment in advanced technologies.

SK Hynix Inc: posted record quarterly earnings in Q3 2025 as demand for AI memory soared. The company has reportedly sold out its AI-chip memory production for 2026, with its chairman describing AI as not a bubble, even if stock prices may correct.

HDFC Bank Limited: Q2 FY26 results showed 11%yoy net profit growth, with net interest income up 5% and other income up 25%. Asset quality is improving, though net interest margins have seen modest compression after front-loaded rate cuts. Management expects NIMs to recover over the next 4–5 quarters.

Reliance Industries Ltd: posted Q2 FY26 consolidated EBITDA up 14.6%yoy and net profit up 14.3%. Its telecom arm Jio passed 500 million subscribers, while retail EBITDA grew 16.5%yoy. Reliance is also moving into AI infrastructure, planning a 1-gigawatt AI data centre in Andhra Pradesh.

Al Rajhi Bank: the world’s largest Islamic bank, reported a 30% jump in net profit for the first nine months of 2025 and maintains a return on equity above 23%. Loan growth is robust, including a 36% rise in SME lending, with strong capital and liquidity ratios.

Bharti Airtel Ltd: has continued to deliver solid double-digit revenue growth, supported by rising data usage, 5G roll-out and tariff normalisation. Management is prioritising deleveraging and network investment, positioning the company to benefit from ongoing growth in India’s mobile and broadband markets.

PDD Holding Inc: (Pinduoduo + Temu) reported Q3 2025 revenues of RMB108.3 bn, up 9%yoy, with management highlighting strong results from agricultural initiatives and a ramp-up in higher-quality Stock Keeping Units (SKUs).

MercadoLibre Inc: In Latin America continues to be a standout: Q3 2025 net revenue grew 39%yoy to US$7.4bn, marking the 27th consecutive quarter of 30% growth. Its fintech arm, MercadoPago, saw total payment volume grow 32%yoy to US$47.7 bn, with the credit portfolio up 83% as digital banking deepens across the region.

Conclusion

China’s record trade surplus is less a victory lap and more a warning sign. It reflects an economy where external demand is doing too much of the heavy lifting, domestic demand is still fragile, and industrial policy remains skewed towards capacity build-out in manufacturing. The Politburo’s new focus on domestic demand and “new productive forces” acknowledges that this model has limits. For investors, this argues against undifferentiated exposure to China and, more broadly, to emerging markets dominated by SOEs. Instead, it supports a more selective approach that favours private sector leaders in technology, consumer platforms and communication services – the companies benefitting from structural themes such as AI, digitalisation and rising EM consumption.

1 Reuters as of 8 December 2025

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account