Originally Posted October 6 2025 – Research Team Q&A: Finding opportunity in uncertainty

In this Q&A, Portfolio Manager and Research Analyst Josh Cummings shares his perspective on volatility, tariffs, artificial intelligence (AI), and U.S. consumer strength.

Key takeaways:

- The U.S. economy remains solid, but the macro tide is no longer lifting all boats. Instead, we’re in a more selective environment increasingly driven by company-specific fundamentals rather than macro bets or thematic processes.

- Tariffs present uncertainty, but so far companies are managing the pressure through supply chain adjustments and strategic pricing. The key question remains how consumers will respond to higher prices, though demand destruction hasn’t materialized yet.

- With AI, we believe it will permeate the economy much like the internet did. It’s important to think broadly across sectors because the biggest investment opportunities may not be the obvious tech players.

Q: It’s been an eventful year, with big swings in market performance. How do you view volatility, and what’s changed in the investment landscape?

A: We like when markets become emotional. That might sound counterintuitive, but in our view, volatility can often present opportunity. There’s a critical distinction that many investors miss: If you’re a long-term investor committed to owning a business for five, 10, or 20 years, short-term volatility can create attractive entry points into high-quality businesses.

That said, the market craves certainty and the noise around politics and policy have created concerns. What we’ve seen this year is that when uncertainty picks up, decision-making slows down across the market. Companies struggle with long-term fixed capital decisions, and even retail giants find themselves flying a little blind.

In terms of the overall investment landscape, the big shift we’ve observed year-to-date is that while the U.S. economy is doing fine, the macro tide is no longer lifting all boats. We’re in a more selective environment now. While AI-related companies remain supported by continued increases in estimates of future data center capital spending, it’s not all about the Mag 7 anymore; top contributors to the S&P 500® Index’s year-to-date performance also include names in financials and aerospace.

As the market broadens out, it’s creating more opportunities for investors who focus on individual company fundamentals rather than macro bets or thematic processes. This environment lends itself to active investing because one of the keys to picking winners is to identify value in places others might overlook.

Q: How are tariffs affecting companies, and how are you evaluating this risk?

A: A lot of our recent conversations with companies have focused on their tariff mitigation strategies. What we’re seeing is a mix of approaches – some substitution, some supply chain movement away from China where and when possible, and pricing increases. But retailers have to be very careful about how they adjust prices.

Many companies are focused on less noticeable items for price increases. For example, if you only buy a coffee maker once every three years, you’re much less sensitive to that price increase than you are to the dozen eggs you buy every week. So, the strategy for what to increase and by how much is important. The critical question for the remainder of the year is around the price elasticity of demand. That is, how much will unit demand contract as prices rise?

The busy holiday season for retailers is still ahead. There are tariffed goods coming in, some un-tariffed goods still on the shelves, and we know prices are going to go up. So far there have been no major calamities, but a lot remains to be seen, and investors need to stay alert as the tariff situation unfolds.

Q: How are you thinking about artificial intelligence (AI) and its investment implications?

A: Any discussion about growth investing must take AI into account, but as a research team, we’re perhaps talking about it a bit differently than most. We can appreciate why investors can myopically focused on a very small group of stocks – those selling into data center growth as a current example.

When we consider a generational theme such as AI, it’s important to think broadly across sectors and to have an investment process built to share insights. Within each of our sector teams, we’re constantly debating how AI will shift the competitive sands by creating victims and beneficiaries of disruption.

What’s happening today reminds some of us of the Internet in 1998 and 1999. Investors became obsessed with a relatively small number of darlings, but only a few of the stocks of the day turned out to be good investments. Yet the Internet ended up being orders of magnitude more impactful than anyone foresaw then. We think AI is going to follow a similar path as it simply permeates the fabric of the global economy.

The companies that may benefit the most aren’t necessarily the obvious AI players; rather, they’re the companies that can effectively integrate AI to improve their business models, reduce costs, enhance customer experiences, or create entirely new revenue streams.

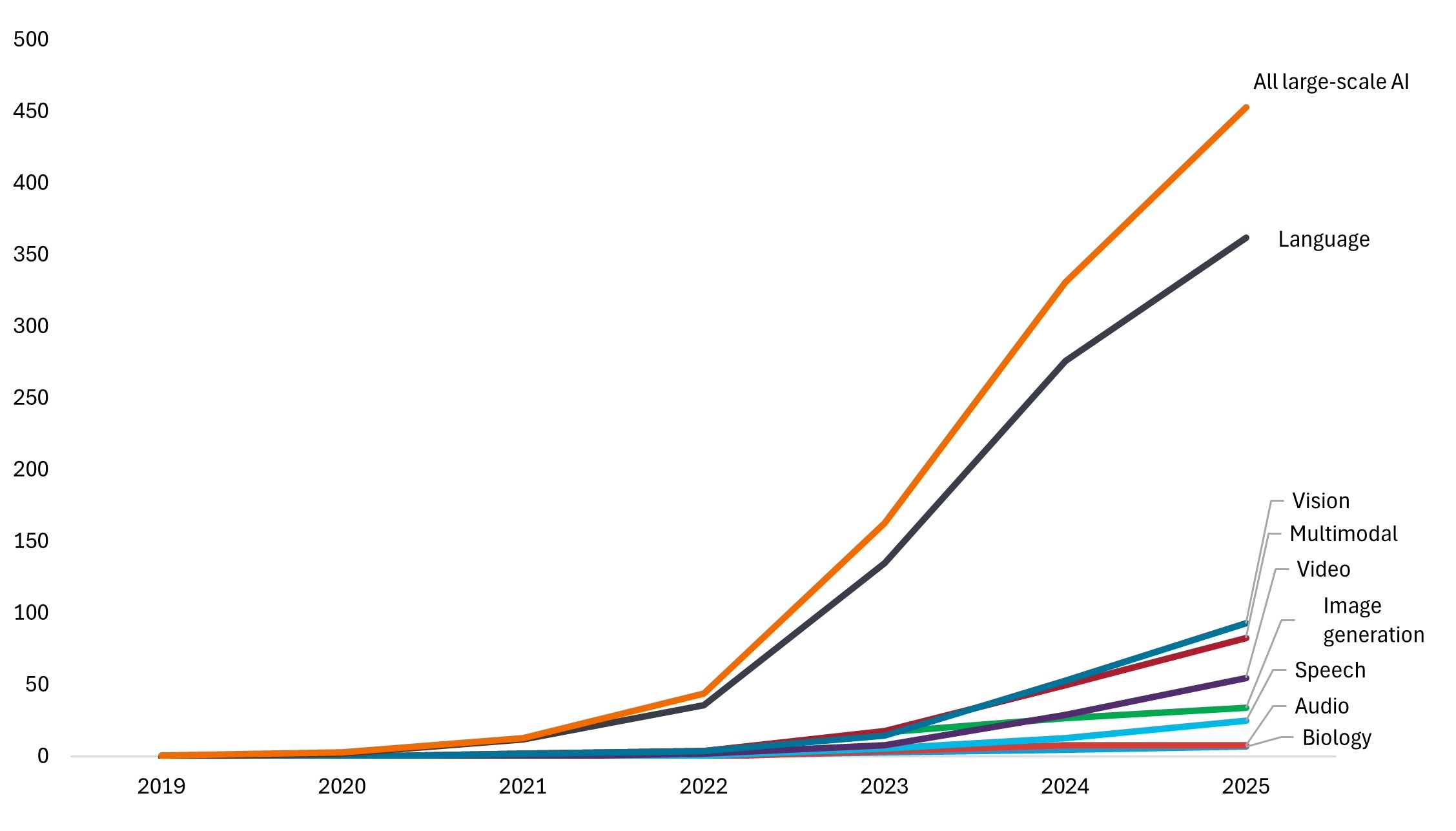

Several years ago, we talked about “big data” and the promise of machine learning, algorithms that could learn relatively simple, repetitive tasks. Large language models (LLMs) and AI are perhaps the ultimate realization of that process. The world is currently generating approximately 30 terabytes of new data every second,1 and roughly 90% of the world’s information has been created within the last two years.2 Additionally, there has been a sharp acceleration in the release of large-scale models since 2022 (Exhibit 1).

Exhibit 1: Cumulative number of large-scale AI models by domain since 2017 Source: Epoch (2025), Our World in Data, as at 12 March 2025.

Source: Epoch (2025), Our World in Data, as at 12 March 2025.

Past performance is not indicative of future results.

What’s your outlook on the U.S. consumer in the current market environment?

The consumer has shown remarkable resilience. While we’re seeing some normalization in spending patterns, the underlying health appears solid. Here’s a key data point that doesn’t get enough attention: Household debt-to-asset ratios are at 50-year lows, which means U.S. households are in a stronger financial position than many investors appreciate (figure 2).

Figure 2: Debt-to-asset ratio for U.S. households

Source: Federal Reserve. As of 30 June 2025.

Source: Federal Reserve. As of 30 June 2025.

Past performance is not indicative of future results

Even in recent months, what we’re hearing from companies almost universally is that business is still pretty good. Consumer sector earnings broadly exceeded expectations in the second quarter.

Tariffs remain a wild card as we discussed. We’re watching carefully how consumer behavior responds to price increases. So far, we haven’t seen major demand destruction, but it’s still early.

Disclosure: Janus Henderson

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account