Historically over the past 10 years, luxury companies have had strong performances, collectively outperforming the European, Euro Stoxx 50 and global MSCI World indices.

The chart below, reflects the comparison of the Euro Stoxx 50 (EXQ1), MSCI World (IWDA) vs LVMH Moet Hennessy Louis Vuitton (MC), Hermes International (RMS) and Kering (KER):

Source: IBKR TWS. Past performance is not indicative of future results

The reasons have been varied:

- Rising global wealth: Economic growth has led to new wealth creation; the global affluent class has expanded and the desire for status symbols and experiences have increased among consumers. These trends have been especially strong in Asia.

- Lower interest rates have played a significant role in boosting consumer spending and asset values, which in turn benefit luxury companies.

- Valuations premiums: Consistent high margins, built investor confidence in a company in ability to generate suitable profits, leading to higher stock valuations (higher Price to Earnings Ratios (P/E).

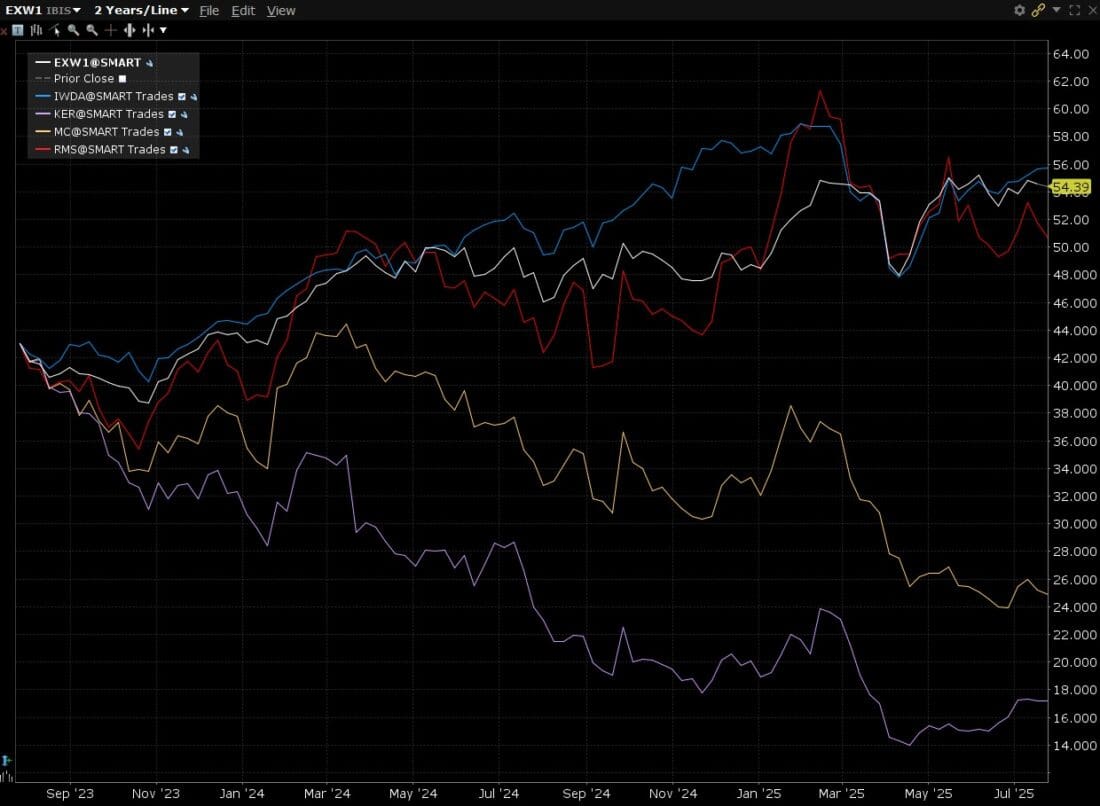

However, when comparing more recent performances there has been a shift, where these companies have had weaker performances when compared to the European, Euro Stoxx 50 and global MSCI World indices, as can be seen in the chart below:

Source: IBKR TWS. Past performance is not indicative of future results

As with the rise in price, there are several reasons that explain the change in trend:

- Deceleration of demand and economic uncertainty. Rising inflation in recent years has eroded consumer purchasing power, and the concern about a potential economic downturn has made consumers more cautious about discretionary spending.

- The market conditions have halted the continuous margin expansions these companies enjoyed. It may have led investors to think that, after a prolonged period of impressive performance, the industry has become overvalued, leading to a correction.

- Lastly, the recent trade war and the market turmoil has increased the fall, they have fallen more sharply than the rest of the market because of this, they would be directly affected by tariffs.

These brands have built a reputation for exceptional quality and artisanry over decades or even centuries. They have a limited production, controlled distribution, and high price points reinforce the perception of exclusivity, making these brands highly desirable. This gives them a competitive advantage.

These are some of their ratios:

| LVMH (MC) | Hermes (RMS) | Kering (KER) | |

| ROE (TTM) | 19.53% | 28.3% | 7.52% |

| Operating Margin (TTM) | 22.33% | 40.54% | 13.45% |

| Total Debt/Total Assets | 27.3% | 9.42% | 44.84% |

| Revenue Growth Rate 3Y (TTM) | 9.66% | 19.09% | -0.86% |

| Price/ Earnings (TTM) | 18.07 | 53.88 | 18.7 |

| Dividend yield (TTM) | 2.75% | 0.68% | 3.04% |

These ratios offer some insight into the companies:

- Hermes exhibits a stronger financial structure with lower debt, higher return on equity (ROE), revenue growth, and operating margin. This superior performance translates to a higher valuation, reflected in a higher price-to-earnings (P/E) ratio and consequently lower dividend yield.

- LVMH occupies a middle ground between Hermes and Kering in terms of financial strength.

- Kering presents a weaker financial profile with higher debt, lower ROE, revenue growth, and operating margin. As a result, its valuation is lower, and the dividend yield is higher.

Upon analysing these figures, it becomes visible that Hermes possesses exceptional fundamentals, yet this strength is offset by a high P/E ratio, which may deter investors in the current economic climate.

While LVMH’s fundamentals are not as robust as Hermes’, they still demonstrate an elevated level of quality, although it has been deteriorating. The market is assigning lower valuation multiples to LVMH compared to Hermes, it is also lower than the EURO Stoxx 50 (24.2) and the MSCI World (28.82).

Kering’s fundamentals are inferior to its competitors. Despite this, the company benefits from lower valuation multiples (Price to Book, Proce to Sales, for example) and a higher dividend yield.

These companies have experienced deficient performance recently, primarily due to economic circumstances and their direct impact on the luxury industry. The recent declines can be seen as a shift in the industry landscape.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account