Before prices hit your shopping cart or gas tank, they move through the production pipeline, and that’s where the Producer Price Index (PPI) comes in. PPI tracks what businesses pay each other for goods and services at the wholesale level, essentially measuring “factory-gate prices” before costs reach consumers. Think of it as inflation’s early warning system: when producer costs rise, those pressures often work their way downstream to consumer prices, making PPI an essential gauge for anyone following inflation trends and Fed policy.

Understanding Headline vs. Core

A critical distinction in PPI data is between headline and core measures:

- Headline PPI includes everything: food, energy, and trade services — components that can swing dramatically month to month based on global commodity markets, weather, or supply disruptions.

- Core PPI strips out those volatile elements (foods, energy, and trade margins) to reveal the underlying trend in producer prices across the broader economy.

This distinction matters significantly for Fed watchers: persistent core inflation would signal entrenched pricing power across industries, while volatile headline moves driven by energy are typically more transient.

September’s Story: Energy-Driven Pressures, Contained Core

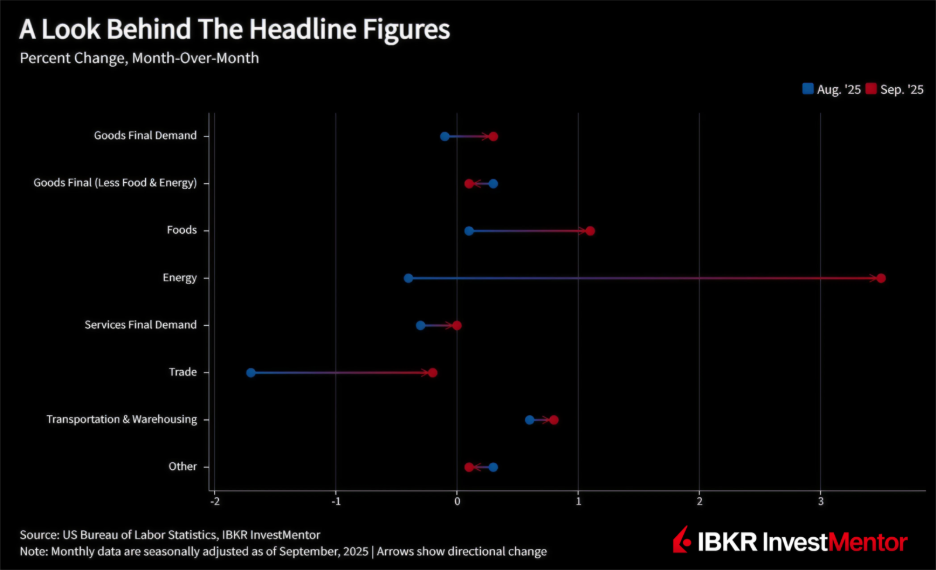

September’s PPI for final demand rose 0.3% from August and is up 2.7% over the past year, reversing a small decline the prior month. Data collection wrapped up before the recent federal funding lapse, so the shutdown didn’t affect these figures. Beneath the headline, the story is concentrated in specific sectors rather than broad-based:

Price increases:

- Final demand goods: +0.9% (largest gain since February)

- Energy: +3.5% overall; gasoline jumped 11.8%

- Food: +1.1%

- Goods excluding food and energy: +0.2% (modest)

Offsetting factors:

- Final demand services: unchanged overall

- Trade margins declined (wholesalers and retailers earned less on sales)

- Transportation and warehousing: +0.8% (airline passenger services +4.0%)

What stands out to me is how much of the monthly move came from energy, particularly gasoline. That 11.8% spike ripples through transportation costs, manufacturing inputs, and distribution networks. Food also pushed higher, but outside those categories, price pressures remained muted.

In September, core PPI rose just 0.1% monthly and 2.6% year-over-year. The fact that core is running cooler than headline tells me the recent pressure isn’t systemic, it’s concentrated in fuel and certain food categories rather than reflecting broad inflation across the entire production pipeline.

Upstream Signals: What’s Happening Further Back in the Supply Chain

Beyond final demand, intermediate goods and services, the inputs businesses buy to produce other products, deserve close attention. These upstream prices can foreshadow future cost pressures:

- Processed goods for intermediate demand: +0.4% in September, +3.8% year-over-year (helped by gasoline and energy products)

- Unprocessed goods for intermediate demand: +0.1% (corn prices rose, but natural gas fell sharply, creating a mixed picture)

- Services for intermediate demand: +0.1% (led by higher margins in food wholesaling)

These movements matter because they represent costs that manufacturers and service providers will eventually need to absorb or pass along. When intermediate prices climb steadily, it often signals that finished goods prices will follow, though the transmission isn’t immediate or guaranteed.

The Takeaway

September’s PPI report points to moderate, energy-led inflation, not a broad price surge. The headline index is up 2.7% over the past year, heavily influenced by that 11.8% jump in gasoline and higher food costs. Core PPI, however, looks calmer: up just 0.1% monthly and 2.6% annually, suggesting underlying price pressures remain relatively contained across most sectors.

For Fed watchers, PPI is an early signal. If producer costs, especially core, keep rising and spread beyond energy and a few categories, those pressures can eventually show up in consumer prices and influence how the Fed approaches future rate cuts as it balances employment support against inflation control.

The key question in my view: is this mostly temporary energy volatility, or the first sign of more persistent cost pressures building in the production pipeline? The answer will become clearer as we see whether September’s move proves to be a one-off spike or the start of a broader trend.

To learn more about how PPI impacts prices download IBKR InvestMentor.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account