In UK politics, fiscal policy often begins not with a budget speech but with a whisper behind a closed door — or a text message sent to a reporter.

Politicians frequently hint at difficult policy choices or leak proposals to the media, from tax hikes and pension reforms to spending cuts. If the backlash is too strong, the proposals are quietly shelved. This ritual of “leak, test, retreat” has become a hallmark of the annual UK budget theatre, a way to gauge public and market reaction without committing to anything.

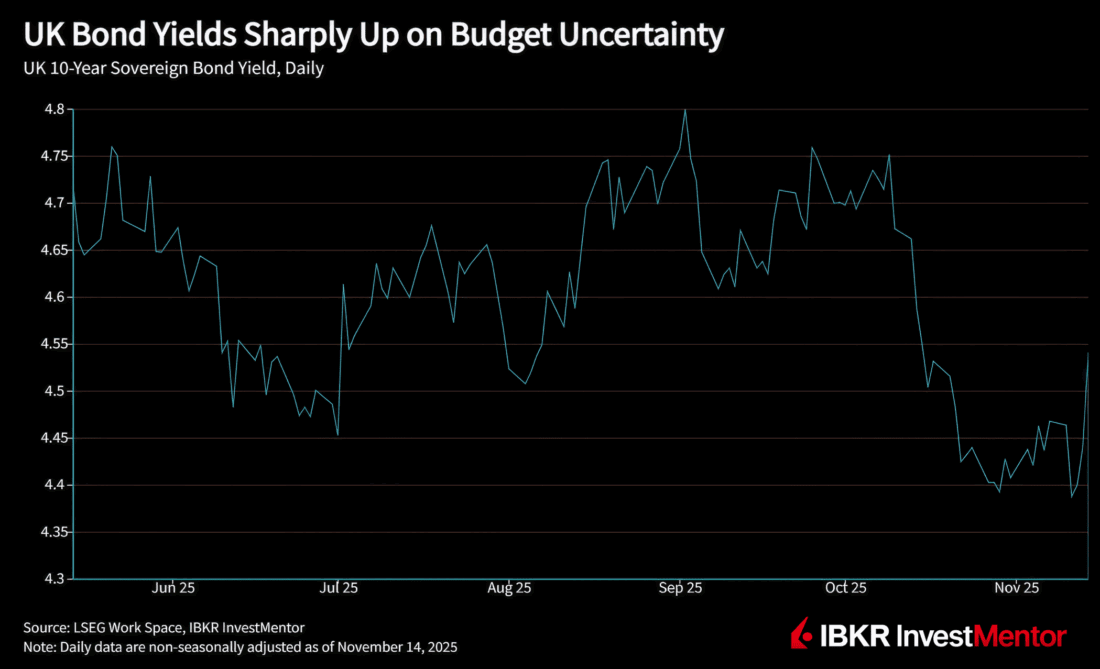

Markets Rattled by a Tax U-Turn

That dance was on full display on Friday, when reports suggested Chancellor — the UK finance minister — Rachel Reeves would abandon plans to raise the basic rate of income tax in the November 26 budget. No official decision has been announced, but the signal alone jolted markets.

- Gilts sold off: yields on longer maturities jumped as much as 14 basis points

- Sterling slipped: down 0.5%, touching its lowest level against the euro in two and a half years

- Stocks fell: FTSE 100 was down nearly 2% at one point, led by banks

Markets had assumed Reeves was preparing to raise rates after warning “we must all contribute.” The sudden wobble left traders questioning fiscal credibility, especially as she is expected to need tens of billions of pounds to stay on track with her fiscal targets.

Government sources briefed the media that better-than-expected forecasts meant tax hikes were unnecessary, but investors weren’t convinced.

Past performance is not indicative of future results.

Breaking a 50-Year Political Taboo

Raising the basic rate of income tax has been avoided for half a century. Politicians see it as a shortcut to an electoral disaster. Reeves’ signals had been widely read as preparing to break that taboo, before stepping back.

Economists, including the well-respected Institute for Fiscal Studies, have argued for higher income tax as one of the few effective and clean ways to plug the fiscal gap. Labour, however, pledged not to raise taxes on “working people”, leaving Reeves caught between economic prudency and political risk.

Lessons from 2022 Mini-Budget

Gilts — British government bonds — are a litmus test of fiscal credibility. When gilt prices fall, yields rise, making it costlier for the government to borrow. Higher borrowing costs often ripple into the wider economy, from mortgage rates to public spending.

The stakes are underscored by the memory of the September 2022 “minibudget”. Then-Prime Minister Liz Truss and Chancellor Kwasi Kwarteng promised the biggest tax cuts since the 1970s, funded by borrowing.

Markets revolted: borrowing costs surged, sterling hit all-time lows against the dollar, and 2-year mortgage rates spiked above 6%. The budget was reversed, the Prime Minister forced out of office in record time, and most of the extreme market moves unwound. But borrowing costs stayed elevated long after. Since then, British politicians have been keen to keep investors onside.

The Real Currency: Credibility

With income tax hikes apparently off the table, the Labour government must now look elsewhere.

- Threshold freezes could raise billions but would hit lower earners hardest

- Business taxes are another option, though politically fraught

- Spending cuts — particularly in capital investment — may be needed to stay within fiscal rules

- Smaller levies could be patched together, but they risk knock-on effects for businesses and households

The lesson is clear: in the UK, fiscal credibility is the real currency. “Leak, test, retreat” may be a political ritual, but markets are less forgiving. Investors want clarity on how the government will raise the revenue it needs. Without it, UK markets will continue to wobble

To learn more about how fiscal policy can move markets, download IBKR InvestMentor.

Learn more about InvestMentor

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account