Stocks are jumping to another record today after well-received corporate earnings reports coincided with economic data pointing to reaccelerating conditions. Indeed, the lightest number of layoffs in six weeks came on the heels of the strongest services PMI in seven months and together signaled a powerful labor market that is motivating consumers to spend relentlessly. Robust domestic demand drove activity in the services sectors, signaling confidence amongst workers that is needed for persistent spending in discretionary categories and is essential for the health of the current cycle. But the rate sensitive sectors went the other way unfortunately, with the manufacturing PMI and New Home Sales missing expectations as heavy financing charges hamper orders and closings. And that problem is exacerbating this morning, with yields climbing in bear flattening fashion as fixed-income watchers pare back Fed Fund trim projections in light of stable hiring and subdued firing. Sector breadth is positive in equities meanwhile, with just three major segments retreating out of 11, and those heavier borrowing costs are generating strong bids for the greenback. Similarly, bitcoins, energy commodities, lumber and forecast contracts are also seeing interest. Conversely though, the gold, copper and silver metals are facing selling pressure while investors unwind hedges illustrated by lower prices for volatility protection instruments.

PMI Depicts Accelerating US Growth

Third-quarter US economic growth has accelerated ferociously, according to this morning’s flash Purchasing Managers’ Index (PMI) data from S&P Global. The boom was uneven, however, as a momentous services sector grew at the fastest pace in seven months, with the segment’s score arriving at 55.2 on robust domestic demand. It exceeded the median estimate of 53 and June’s 52.9. Conversely, manufacturing sank and missed the contraction-expansion border of 50 with a print of only 49.5, a seven-month low. It arrived beneath the consensus projection of 52.6 and the previous month’s 52. Goods activities lost speed in light of a waning effect from tariff front running. Price pressures were strong in both segments, partially due to tariffs but additionally because of labor shortages that drove up wage bills. Confidence was subdued, meanwhile, as survey respondents were concerned of drops in federal spending.

New Home Sales Miss Estimates

The pace of new home sales barely recovered last month despite homebuilders offering concessions and lighter prices. The rate of transactions fell 0.6% month over month to 627,000 seasonally adjusted annualized units (SAAU), below the expected 650,000 but slightly above May’s 623,000. Closings were down in the Northeast and West by 27.6% and 8.4% m/m but expanded by 6.3% and 5.1% in the Midwest and South. Both the median and average sales prices dropped from $422,700 and $511,500 to $401,800 and $501,000 and were also lower than valuations from a year ago by 2.9% and 2%. The monthly supply inventory ratio rose to 9.8, the most elevated since September 2022, almost three years ago.

Past performance is not indicative of future results

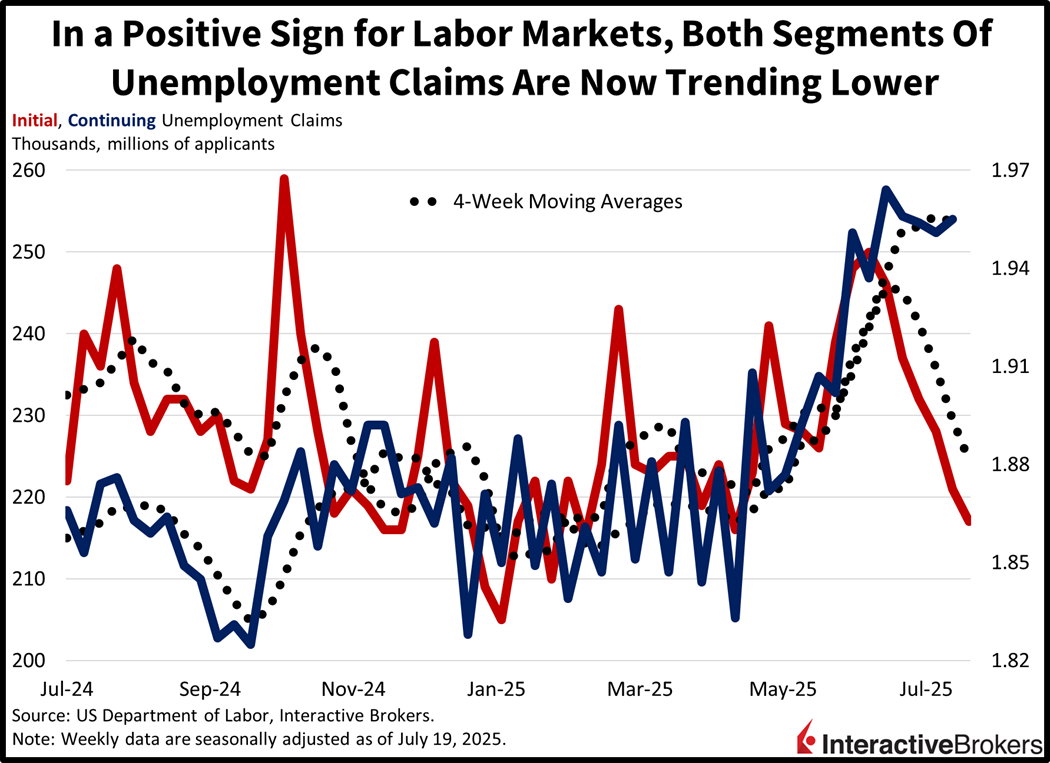

Initial and Continuing Claims Trend Lower

Initial unemployment claims marked a 14-week low, dropping for the sixth-consecutive print to their lowest level since early April. Continuing filings, meanwhile, remained elevated but also missed expectations despite rising modestly. First-time applications fell to 217,000 for the seven-day period ended July 19, beneath the projected 227,000 and the prior report’s 221,000. Continuing visits increased to 1.955 million for the week ended July 12, below the 1.960 million median estimate but slightly above the previous publication’s 1.951 million. In an encouraging sign of labor market strength though folks, the four-week moving averages for both segments ticked lower to 224,500 and 1.954 million from 229,500 and 1.956 million.

Past performance is not indicative of future results

Path to Economic Acceleration Widens

The US economy is likely to accelerate in the months to come as a rise in relative certainty bolsters confidence amongst corporate executives and consumers alike. Supply-side tailwinds are being driven by lighter taxation, milder regulations, onshoring incentives and heavy oil production, which are coinciding with robust demand conditions and widening the path for S&P 500 earnings expansion. Consumer spending has hung in there and so has hiring, but the back half is likely to deliver even better results, although immigration restrictions will contain progress. Meanwhile, softer borrowing costs are also going to support bullish conditions, as market watchers price in 2 rate cuts by the end of the year. And duration is poised to cooperate too as fixed-income analysts notice inflation stabilizing in the mid 2s. Moreover, strong activity and tariff revenues can soften extended term premiums and quell sovereign debt and fiscal imbalance concerns. Lower costs of capital are critical to this constructive outlook, as they would push the rate-sensitive manufacturing and real estate sectors of the economy into growth territories and broaden progress.

International Roundup

Eurozone Services Grow but Manufacturing Decline Continues

The flash Eurozone Services PMI climbed further into expansion this month, but its manufacturing counterpart remained in contraction despite hitting a 36-month high.

The manufacturing gauge climbed from 49.5 in June to 49.8, slightly higher than the economist consensus estimate. It was a 36-month high but still below the contraction-expansion threshold of 50. Output increased marginally with Germany offsetting weakness in France.

The Eurozone Services PMI also climbed, reaching 51.2, a six-month high and up from 50.5 in June. It also exceeded the economist economic consensus estimate of 50.6.

Regarding overall activities in both manufacturing and services sectors, a 13-month contraction of new orders stabilized, but new export orders continued to fall. The strengthening trend in new orders resulted in employers adding workers for the fifth consecutive month. While staffing declined in manufacturing, it increased in services, with overall additions being only marginal. Despite the marginal increase in staffing, business sentiment sank in both goods producing and services sectors after hitting an 11-month high in June.

Canada Retailing Turns Positive

Retail sales in Canada climbed 1.6% m/m in June after falling 1.1% in the preceding month, according to preliminary data for Statistics Canada. In a similar manner, manufacturing sales turned positive, posting a 0.4% increase after sinking 0.9% in May.

South Korea’s GDP Turns Positive

After a negative first-quarter print, South Korea’s gross domestic product (GDP) turned positive during the period running from April through June, according to Statistics Korea. For the recent period, GDP was up 0.6% quarter over quarter, exceeding the economist consensus expectation of 0.5% and reversing from the 0.2% decline in the first quarter. The year-over-year result of 0.5%, meanwhile, accelerated from the goose egg recorded for the first quarter and surpassed the consensus estimate of 0.4%.

Activity expanded 2.7% in manufacturing and 0.6% in services, but declined by the stated amounts in the following categories:

- Construction, 4.4%

- Electricity, gas and water supply, 3.2%

- Agriculture, forestry and fishing, 1.4%.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account