Stocks are rebounding for the second consecutive session on strengthening confidence that the Iran war could end sooner rather than later even as Secretary Hegseth warned of the most intense day of strikes so far on this Tuesday. The risks of an oil shortage, furthermore, were tempered by the G7 gearing up to possibly release barrels from their strategic inventories and by President Trump saying yesterday that the conflict is near its end. Economic data were also supportive of a broad advance across equities and non-energy commodities, as strong performances on ADP’s weekly jobs numbers and a beat on existing home sales offset a lackluster small business optimism print, reassuring investors that the cycle remains on healthy ground. But Treasuries and the greenback are around their flatlines, as investors await tomorrow’s CPI results and further developments from the Middle East to gauge cost forces and inflation expectations.

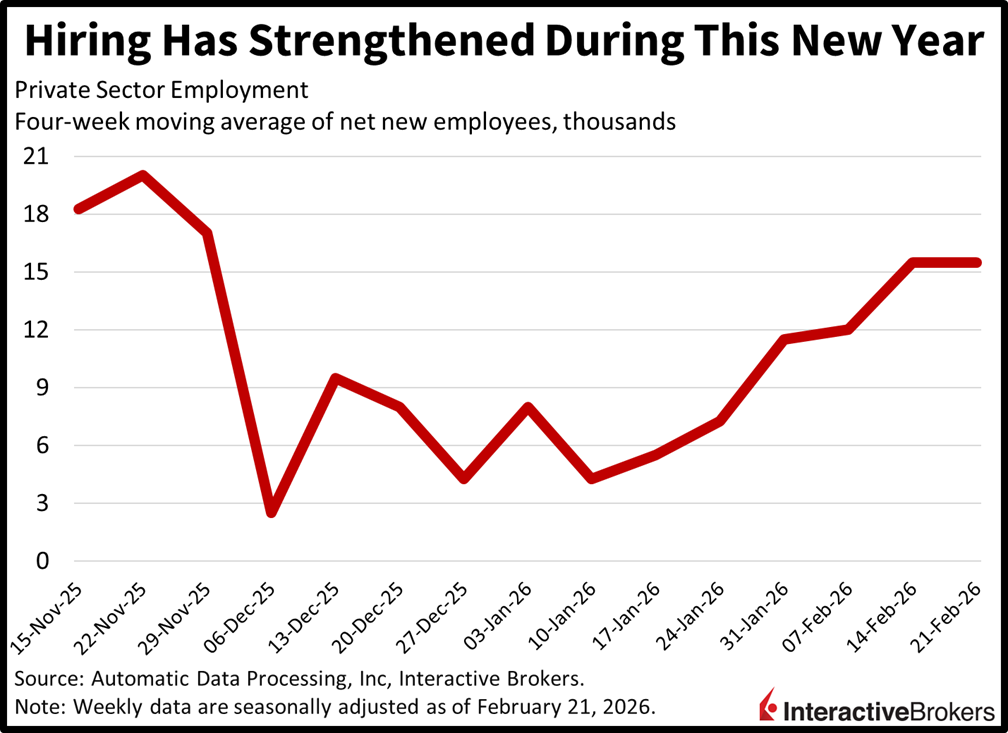

ADP Data Reflect Different Reality Than BLS

Private sector payrolls increased by an average of 15.5k workers in each of the four weeks during the period ended Feb. 21, maintaining the same pace as the prior interval, according to ADP. These numbers are the strongest of the year and are essentially at odds with the BLS print from last week that depicted heavy job losses. The situation illustrates why it’s important to have a buffet approach with economic publications, and the general message across the wide array of reports signals stable labor conditions.

Past performance is not indicative of future results.

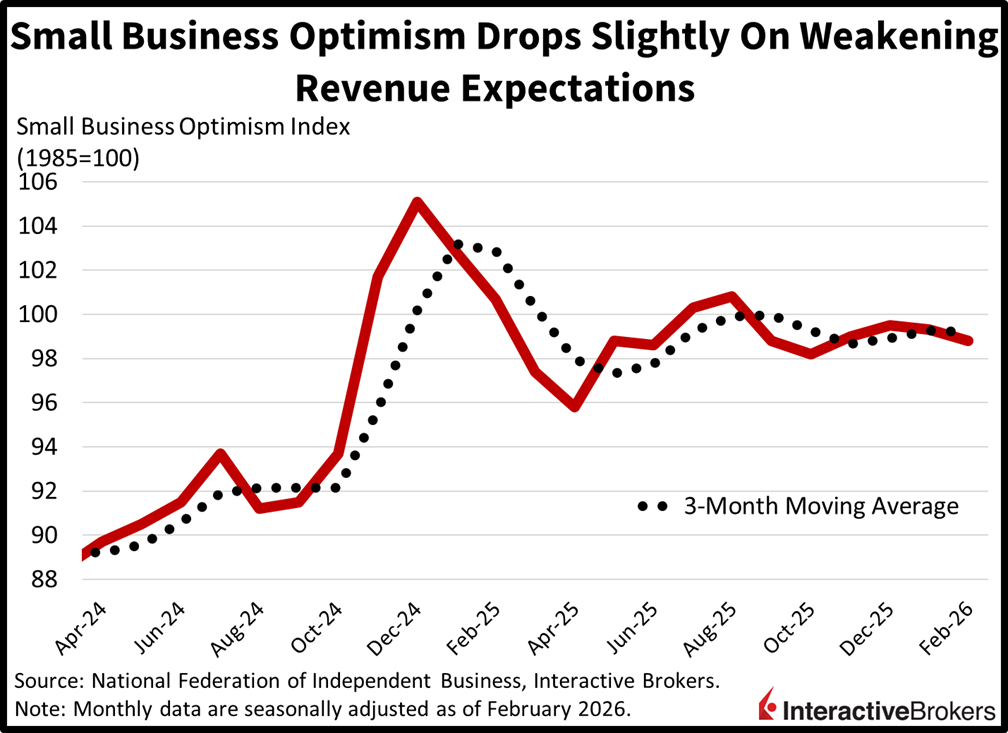

Sales Expectations Weigh on Small Business Sentiment

The National Federation of Independent Business’s gauge for optimism slipped for the second consecutive month, as slower sales expectations weighed on hiring intentions and the economic outlook. The February headline figure of 98.8 arrived beneath the median estimate of 99.7 and the prior period’s 99.3. Job openings and earnings trends improved, partially countering the impact of softening revenue projections. When asked what the single most important problem was, 19% of survey respondents cited taxes, 15% said quality of labor, 12% mentioned inflation and 11% were hurt by a lack of customers.

Past performance is not indicative of future results.

Existing Home Sales Strengthen Modestly

Sales of existing homes climbed 1.7% month over month (m/m) last month to a 4.09 million seasonally adjusted annual rate (SAAR) as improving wages and slightly lower financing costs improved affordability, causing more shoppers to become buyers. The pace exceeded the economist consensus estimate for 3.89 million SAAR and picked up from 4.02 million SAAR in January. Despite the gain, sales were still down 1.4% year over year (y/y). For the m/m results, condominium and co-ops deals climbed 5.3% m/m followed by the 2.5% hike in single-family residences. Among regions, the West led with m/m growth of 8.2% and was followed by the 1.6% gain in the South and the 1.1% increase in the Midwest. Volume in the Northeast, however, sank 6%.

The median sales price for all housing types ascended by 0.3% y/y to $398,000, making February the 32nd month of homes becoming more expensive. Conversely, affordability was enhanced by the average mortgage interest rate falling from 6.10% to 6.05%. Inventory remained at January’s level of 3.8 months of supply with stronger sales helping to offset the impact of the number of available residences increasing 2.4% m/m and 4.9% y/y.

Peace in the Middle East is Bullish

An end to the Iran war and the elimination of an oil supply crunch risk would benefit equities and fixed income tremendously. Indeed, the corporate earnings outlook would become far less cloudy and inflation expectations would take a dive, helping to potentially raise stock valuations while lighter interest rates loosen financial conditions. But messaging from Washington has been mixed, and there’s still a chance of a reescalation in the Middle East conflict, which has sustained elevated volatility levels on the back of a wide range of potential outcomes for asset prices. Similar to last year’s tariff uncertainty and Russia’s invasion of Ukraine in 2022, these significant shifts could materially change fundamentals for shareholders and substantially alter performance across the yield curve, however, recent developments do lift the odds of Wall Street being out of the woods in short order.

International Roundup

China’s Trade Surplus Soars

China’s goods trade surplus during the first two months of 2026 jumped to $213 billion, an all-time high record for the January and February period, according to the General Administration of Customs of China. The organization combined the two months when releasing the data to compensate for the annual differences in the dates of the Lunar New Year holiday. During the period, exports to the US fell 11% y/y in response to import tariffs while overall shipments of goods to foreign markets climbed 21.8%, a much stronger showing than the 7.1% gain expected by a consensus of economists. Africa’s purchases of Chinese products led the growth, expanding by 50%. The following regions and the extent of the growth were also significant:

- ASEAN countries, 29.4%

- The EU by 27.8%

- Latin America, 16.4%

Exports of technology products, electronics and automobiles were particularly strong.

Imports during the period were 19.8% higher than in the January-February period of 2025. China produced an all-time record high surplus of $1.2 trillion last year.

Household Spending Falls in Japan

Household spending in Japan kicked of the year by declining 2.5% m/m and 1% y/y in January. The results were considerably worse than the economist consensus estimate for outlays to increase 0.8% m/m and 2.4% y/y following December’s 2.2% and 2.6% drops. Education and housing costs fell the most with y/y declines of 22.6% and 12.3%. Fuel, light and water charges sank 2.6% and clothing and footwear descended 1.7%. The transportation and communications category also weakened, falling 1%.

Separately, workers’ real income was up 1.3% y/y, a deceleration from 3% in December.

Retail Sales in the UK Disappoint

February retail transactions in the UK were 1.1% higher than in the year-ago period with rainy weather weighing on consumers’ spending appetites, according to the British Retail Consortium. The print trailed the 12-month average of 2.3%. Food sales appeared the strongest, recording a 2.9% jump but falling below the 12-month growth average of 3.8%. Non-food purchases, however, sank by 0.4% compared to the 12-month average growth of 1%. The online non-food sales category, furthermore, dropped 1.3%, underperforming the 12-month average of 1.2%. The BRC notes that Valentine’s Day was an exception with strong sales of jewelry, watches and perfume. Going forward, low consumer sentiment and uncertainty regarding the Middle East war are likely to challenge the sector.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account