Markets are indecisive today as participants await a catalyst that could potentially send stocks above all-time highs. President Trump’s declaration that the Iran-Israel conflict is over has turned Wall Street’s focus to the taxation and cross-border fronts. Meaningful progress on any of the two matters can bolster equities to fresh records. Today’s economic calendar was quiet, but New Home Sales plunged to their lowest level since October despite a long list of builder concession and discount programs. Affordability constraints driven by near 7-handle mortgages and costly residences continued to weigh on transactions and push up inventories. On the data front, this Friday’s PCE could be a significant influencer for asset prices, because if the Fed’s preferred inflation gauge reflects a lack of sticker pressures, then traders on the floor may very well start chanting “rate cut, rate cut.” In today’s trading, equity breadth is narrow with investors only reflecting interest in technology and communication services shares. But they are scooping up Treasuries with a short-end bias, bitcoins, commodity futures ex nat gas and lumber and forecast contracts. Elsewhere, the greenback is flat, yields from the belly of the curve out to the 30-year maturity are rising slightly ahead of a $70 billion offering of 5-year notes, and folks are gently unwinding volatility protection instruments.

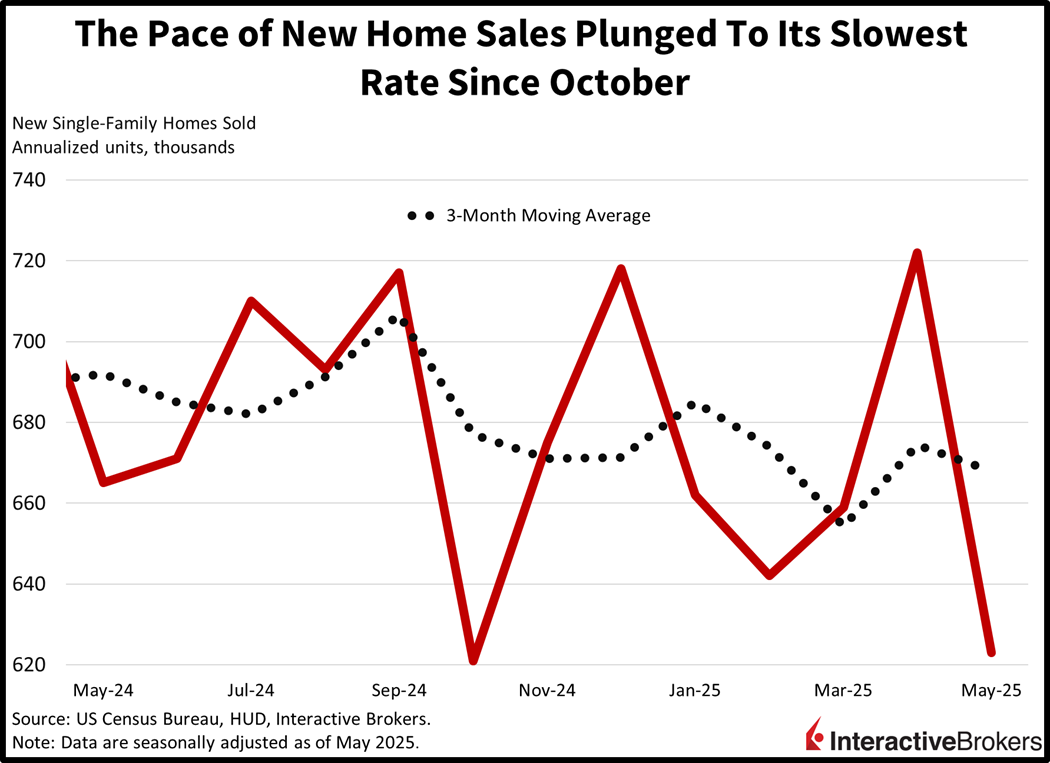

New Home Sales Sink to October Level

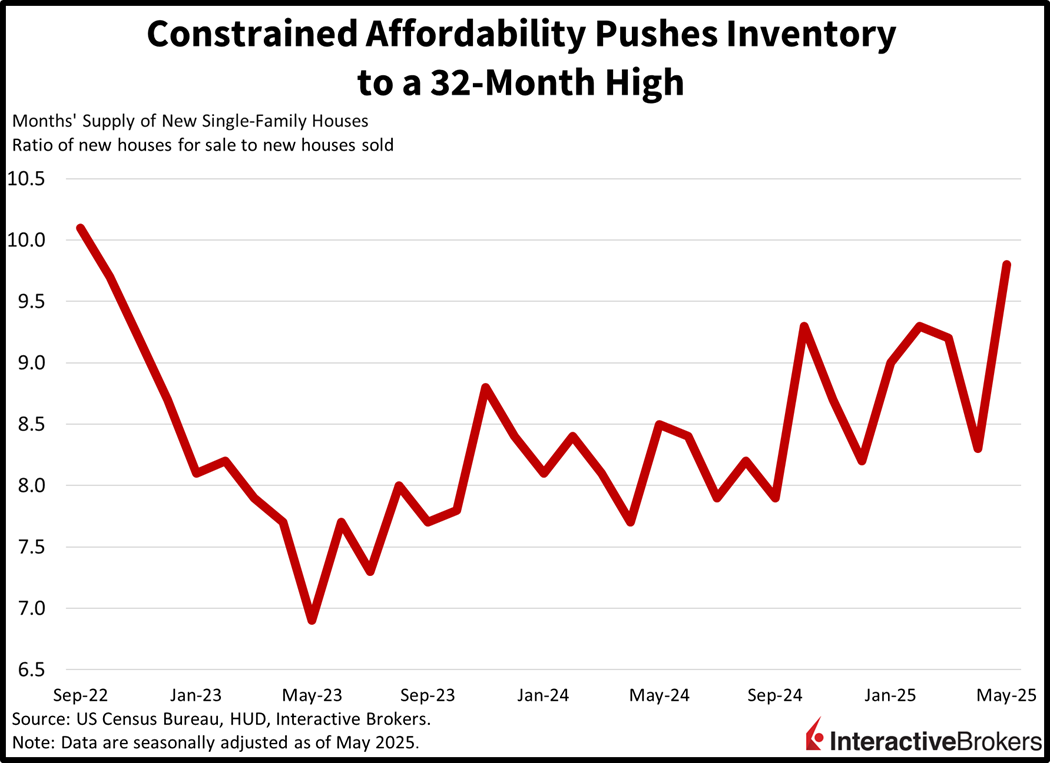

In another sign that the real estate market is struggling under the weight of elevated mortgage rates and lofty prices, new home sales plunged to its slowest pace since October. The 623,000 seasonally adjusted annualized units sold last month marked a 13.7% month-over-month (m/m) decline, badly missing estimates for 690,000. April’s result was 722,000. Declines in the larger regions from a residential construction perspective of 21% m/m in the South, 7.1% in the Midwest and 5.4% in the West failed to be offset by a 32.1% m/m gain in the Northeast. The lack of buying activity drove the inventory ratio north to the tallest level since September of 2022, almost three years ago. Indeed, the number of months of sales based on the current transaction rate increase from 8.3 to 9.8 m/m. But despite the lack of demand, the median and average closing price rose from $411,400 and $511,200 to $426,600 and $522,200, which is emblematic of the margin pressure that builders face against the backdrop of costly labor, materials, land, insurance, financing, etc.

Past performance is not indicative of future results

Investors Await Further Clues Before Diving In

Wall Street is waiting for progress on taxation or trade to justify current valuations and push equities higher, but the economic calendar may serve a pleasant surprise. Key releases in the next few days include unemployment claims and the Fed’s preferred inflation gauge, which could quell slowdown worries and price pressure angst. We’ll also examine durable goods tomorrow, which will offer information concerning the momentum of capital expenditures, a significant element of the Trump administration’s onshoring ambitions. Finally, Treasury auctions have generally performed well lately and bullish at the long end alongside a rate cut could fuel corporate earnings growth and economic performance from here.

International Roundup

Japan Policymakers Express Divergent Views

Policymakers during the Bank of Japan June 16-17 meeting were split over the need to raise the key interest rate, according to a summary of opinions released yesterday. The bank decided to keep the rate stable at 0.5%. Certain members pushed for maintaining the existing level, arguing that the impacts of U.S. tariffs are highly uncertain. Conversely, some members maintained that price pressures are higher than expected, so a loftier benchmark level is warranted. Another member opined that the adverse results of tariffs have yet to materialize, and that trade uncertainty is likely to hurt business sentiment. The BOJ kicked off 2025 by raising its interest rate to 0.5% in January. Meanwhile, inflation has surpassed the organization’s 2% goal, largely due to companies passing the costs of higher raw materials onto customers.

In a presentation this morning, board member Naoki Tamura warned that inflation could accelerate and argued in favor of the bank raising the short-term financing rate.

Corporate Price Pressure Higher than Expected

Japan’s Corporate Services Price Index was up 3.3% year over year (y/y) for May, exceeding the economist estimate of 3.1% but easing from 3.4% in April. The gauge measures prices that corporations charge each other.

A Bad Read for Vices in Australia

Australia’s Consumer Price Index (CPI) climbed 2.1% during the 12-months to May, a slower pace than the 2.4% y/y rate for April, according to the Australian Bureau of Statistics. Economists anticipated a 2.3% northward change. Consumers who enjoy alcohol and tobacco faced a 5.9% hike, making it the category the largest contributor to the headline’s increase. Tobacco fuel the jump, rising 11.5%. The health segment and the food and non-alcoholic beverage category followed with increases of 4.4% and 2.9%

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account